International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 13, Issue 3 (March 2026), Pages: 130-142

----------------------------------------------

Original Research Paper

Impact of a training program on the professional skepticism of auditing students: The moderating role of trait skepticism

Author(s):

Affiliation(s):

Faculty of Accounting and Business, Thuyloi University, Kim Lien, Hanoi, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0005-0825-2135

Corresponding author's ORCID profile: https://orcid.org/0009-0005-0825-2135

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2026.03.013

Abstract

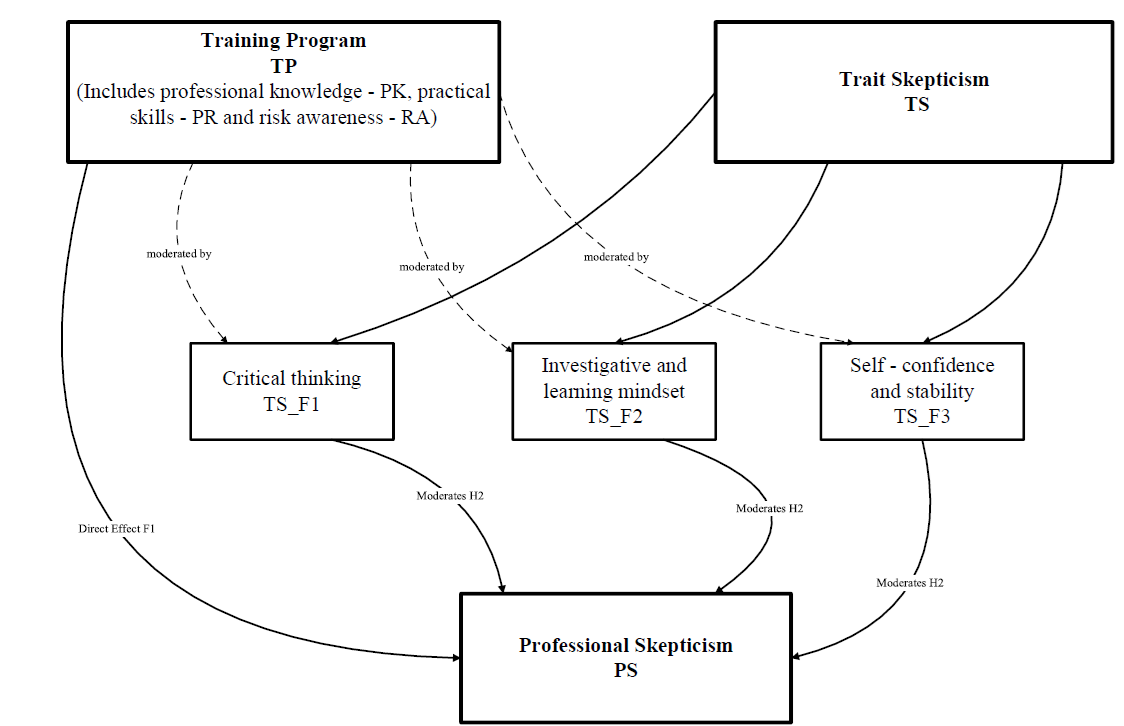

This study examines the effect of a training program on the professional skepticism of auditing students and investigates the moderating role of trait skepticism. A mixed-methods approach was used. In-depth interviews were conducted in two phases to refine the measurement scales and to help interpret the quantitative findings. In addition, a survey was administered to 239 auditing students at a university in Vietnam. The results show that the training program has a positive and significant effect on students’ professional skepticism. The findings also reveal a moderating effect of trait skepticism. For students who already have high levels of critical thinking and inquisitiveness, the training program is still beneficial, but the additional improvement is relatively smaller. In contrast, students with lower initial levels of trait skepticism gain greater marginal benefits from the program. This study was conducted at a single university, which may limit the generalizability of the results. Moreover, the cross-sectional design does not capture changes in skepticism over time. Future research should include multiple universities and use longitudinal designs to examine how skepticism develops during both study and professional practice. Further studies could also explore the role of organizational and cultural factors in shaping skepticism in auditing practice. These findings provide useful implications for the design and improvement of auditing training programs by highlighting the importance of adapting training strategies to the different characteristics of students, thereby supporting the development of high-quality future auditing professionals.

© 2026 The Authors. Published by IASE.

This is an

Keywords

Professional skepticism, Training program, Trait skepticism, Audit, Student

Article history

Received 10 October 2025, Received in revised form 4 March 2026, Accepted 10 March 2026

Acknowledgment

This research was funded by the Science and Technology Budget of Thuyloi University under project code CS2025-17. The authors would like to express their sincere gratitude to Thuyloi University for the financial support provided for this study.

Compliance with ethical standards

Ethical considerations:

This study was conducted in compliance with ethical standards. All participants provided informed consent prior to participation, and their privacy and confidentiality were protected throughout the study.

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.Citation:

Hoang TML, Tran TH, Tran MN, and Le TH (2026). Impact of a training program on the professional skepticism of auditing students: The moderating role of trait skepticism. International Journal of Advanced and Applied Sciences, 13(3): 130-142

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (23)

Ajzen I (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2): 179-211. https://doi.org/10.1016/0749-5978(91)90020-T [Google Scholar]

Bandura A (1997). Self-efficacy: The exercise of control. Macmillan, London, UK. [Google Scholar]

Bonner SE and Walker PL (1994). The effects of instruction and experience on the acquisition of auditing knowledge. The Accounting Review, 69(1): 157–178. https://doi.org/10.2308/TAR-9410256365 [Google Scholar]

Carpenter TD, Durtschi C, and Gaynor LM (2011). The incremental benefits of a forensic accounting course on skepticism and fraud-related judgments. Issues in Accounting Education, 26(1): 1-21. https://doi.org/10.2308/iace.2011.26.1.1 [Google Scholar]

Chang L (1994). A psychometric evaluation of 4-point and 6-point Likert-type scales in relation to reliability and validity. Applied Psychological Measurement, 18(3): 205-215. https://doi.org/10.1177/014662169401800302 [Google Scholar]

Glover SM and Prawitt DF (2014). Enhancing auditor professional skepticism: The professional skepticism continuum. Current Issues in Auditing, 8(2): P1-P10. https://doi.org/10.2308/ciia-50895 [Google Scholar]

Hurtt RK (2010). Development of a scale to measure professional skepticism. AUDITING: A Journal of Practice & Theory, 29(1): 149-171. https://doi.org/10.2308/aud.2010.29.1.149 [Google Scholar]

Hurtt RK, Brown-Liburd H, Earley CE, and Krishnamoorthy G (2013). Research on auditor professional skepticism: Literature synthesis and opportunities for future research. AUDITING: A Journal of Practice & Theory, 32(Supplement 1): 45-97. https://doi.org/10.2308/ajpt-50361 [Google Scholar]

Kolb DA (1984). Experiential learning: Experience as the source of learning and development. Prentice-Hall, Englewood Cliffs, USA. [Google Scholar]

Liu X (2018). Can professional skepticism be learned? Evidence from China. Journal of Education for Business, 93(6): 267-275. https://doi.org/10.1080/08832323.2018.1466773 [Google Scholar]

Messier WF, Glover SM, and Prawitt DF (2019). Auditing & assurance services: A systematic approach. 11th Edition, McGraw-Hill Education, Columbus, USA. [Google Scholar]

Nelson MW (2009). A model and literature review of professional skepticism in auditing. AUDITING: A Journal of Practice & Theory, 28(2): 1-34. https://doi.org/10.2308/aud.2009.28.2.1 [Google Scholar]

Nolder CJ and Kadous K (2018). Grounding the professional skepticism construct in mindset and attitude theory: A way forward. Accounting, Organizations and Society, 67: 1-14. https://doi.org/10.1016/j.aos.2018.03.010 [Google Scholar]

Peecher ME, Solomon I, and Trotman KT (2013). An accountability framework for financial statement auditors and related research questions. Accounting, Organizations and Society, 38(8): 596-620. https://doi.org/10.1016/j.aos.2013.07.002 [Google Scholar]

Popova V (2012). Exploration of skepticism, client‐specific experiences, and audit judgments. Managerial Auditing Journal, 28(2): 140-160. https://doi.org/10.1108/02686901311284540 [Google Scholar]

Quadackers L, Groot T, and Wright A (2014). Auditors’ professional skepticism: Neutrality versus presumptive doubt. Contemporary Accounting Research, 31(3): 639-657. https://doi.org/10.1111/1911-3846.12052 [Google Scholar]

Ramadhany AA, Erlina E, Sadalia I, and Fachrudin KA (2025). Enhancing fraud detection performance: The interplay of red flag awareness, self-efficacy, and professional skepticism. Journal of Risk and Financial Management, 18(6): 301. https://doi.org/10.3390/jrfm18060301 [Google Scholar]

Rasso JT (2015). Construal instructions and professional skepticism in evaluating complex estimates. Accounting, Organizations and Society, 46: 44-55. https://doi.org/10.1016/j.aos.2015.03.003 [Google Scholar]

Robinson SN, Curtis MB, and Robertson JC (2018). Disentangling the trait and state components of professional skepticism: Specifying a process for state scale development. AUDITING: A Journal of Practice & Theory, 37(1): 215-235. https://doi.org/10.2308/ajpt-51738 [Google Scholar]

Rodgers W, Mubako GN, and Hall L (2017). Knowledge management: The effect of knowledge transfer on professional skepticism in audit engagement planning. Computers in Human Behavior, 70: 564-574. https://doi.org/10.1016/j.chb.2016.12.069 [Google Scholar]

Ta TT, Doan TN, Pham DC, and Tran HN (2022). Factors affecting the professional skepticism of independent auditors in Viet Nam. Cogent Business and Management, 9(1): 2059043. https://doi.org/10.1080/23311975.2022.2059043 [Google Scholar]

Trotman KT, Bauer TD, and Humphreys KA (2015). Group judgment and decision making in auditing: Past and future research. Accounting, Organizations and Society, 47: 56-72. https://doi.org/10.1016/j.aos.2015.09.004 [Google Scholar]

- Weijters B, Cabooter E, and Schillewaert N (2010). The effect of rating scale format on response styles: The number of response categories and response category labels. International Journal of Research in Marketing, 27(3): 236-247. https://doi.org/10.1016/j.ijresmar.2010.02.004 [Google Scholar]