International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 13, Issue 2 (February 2026), Pages: 229-239

----------------------------------------------

Original Research Paper

The impact of stock splits and reverse stock splits on stock returns in the Indonesian market

Author(s):

Affiliation(s):

Faculty of Economics and Business, Universitas Pendidikan Nasional, Denpasar, Indonesia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-7064-6304

Corresponding author's ORCID profile: https://orcid.org/0000-0002-7064-6304

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2026.02.024

Abstract

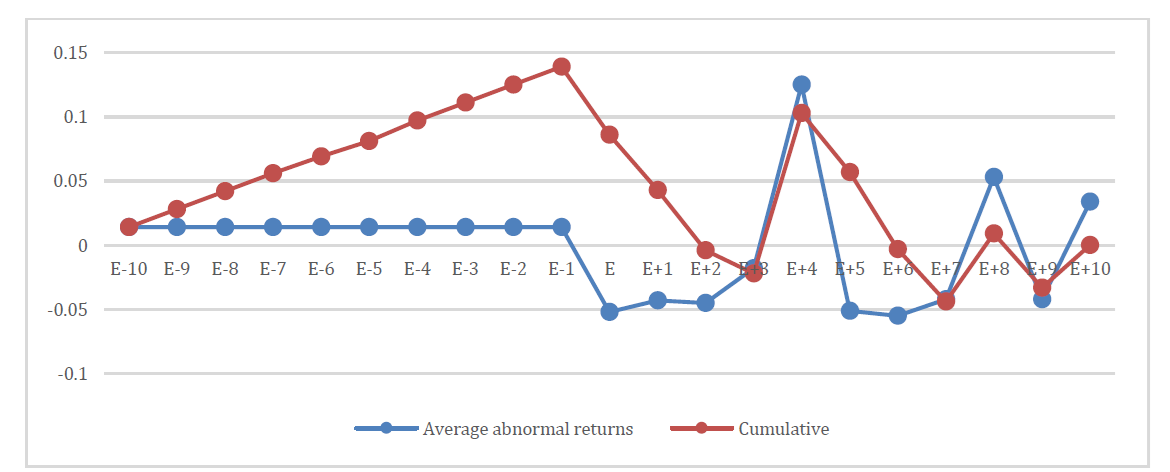

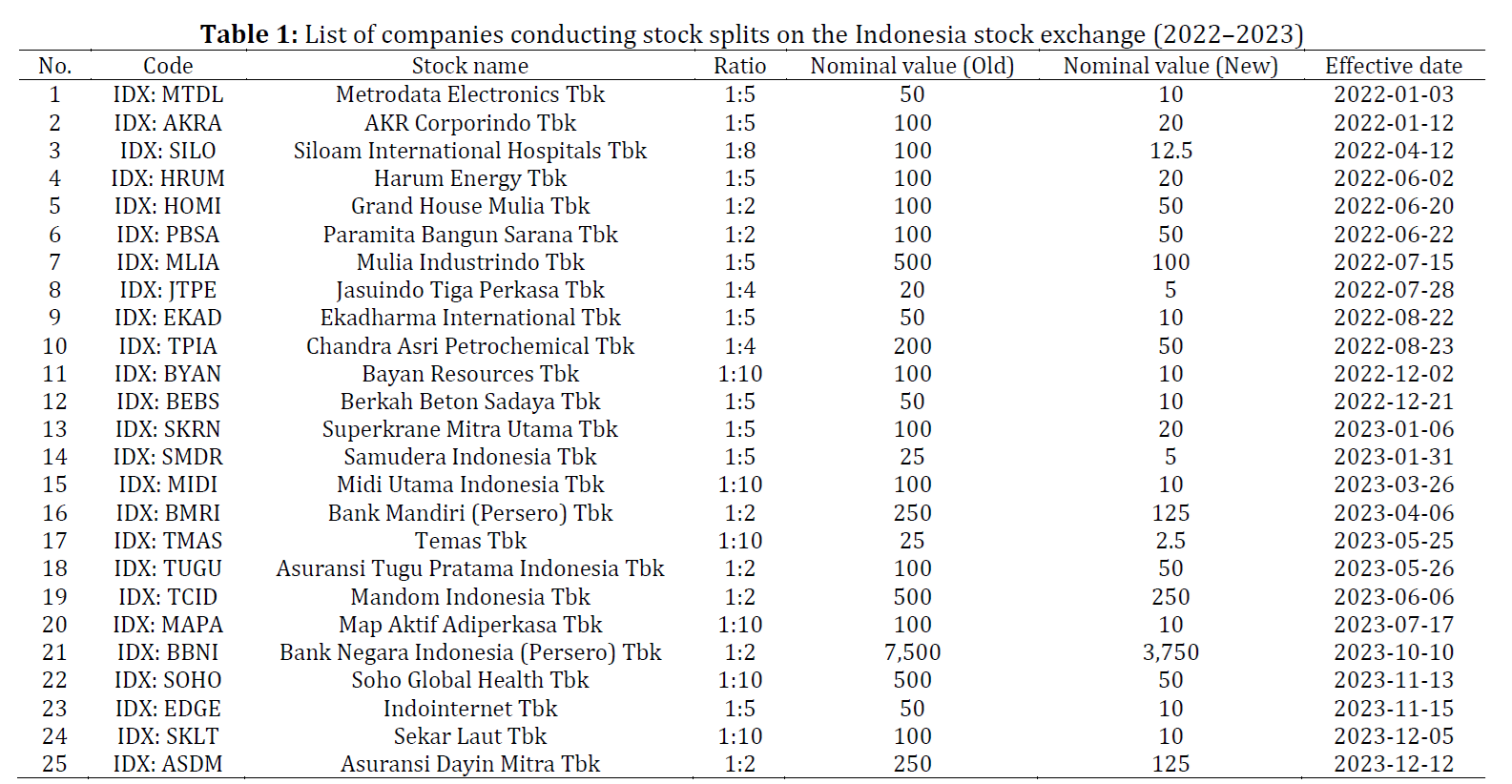

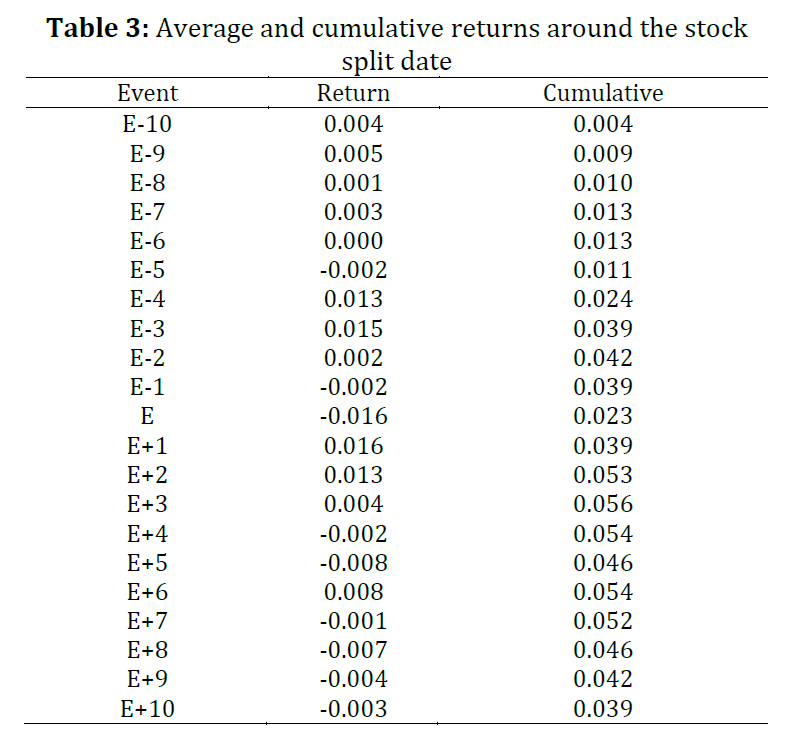

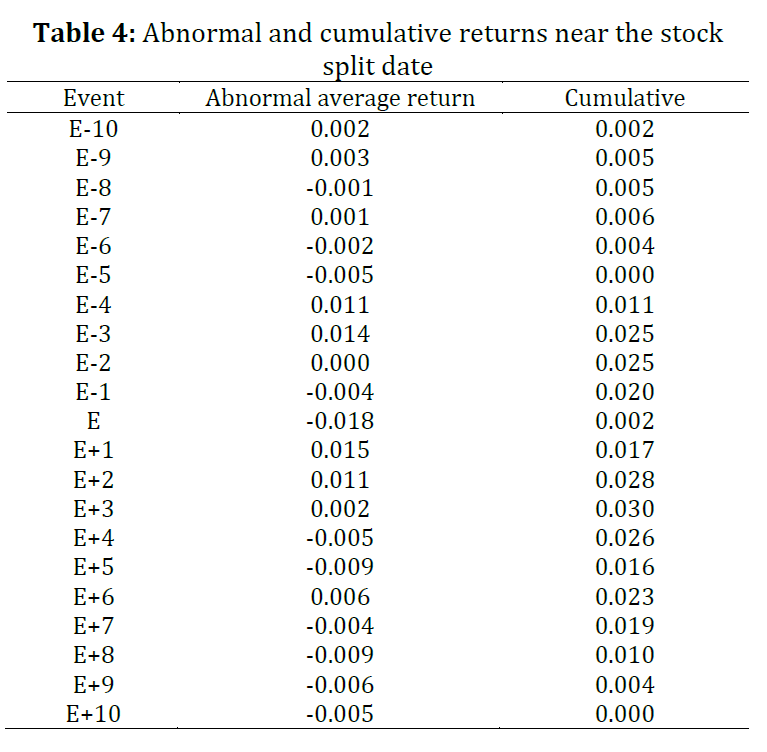

This study examines the impact of stock splits and reverse stock splits on stock returns around their effective dates in the Indonesia Stock Exchange during the 2022–2023 period. The research applies an event study method and uses the cumulative abnormal return (CAR) approach to measure the difference between actual and expected returns within a 10-day window before and after the corporate action. The results show that stock splits generally have a positive effect on stock returns. CAR increases significantly before the effective date, suggesting a favorable reaction from investors. In contrast, reverse stock splits have a negative effect, as CAR declines sharply on and after the effective date. These findings indicate that stock splits are viewed as positive signals about a company’s future performance, while reverse stock splits are often interpreted as signs of potential financial or operational problems. This study contributes to the literature on financial markets in emerging economies and provides practical implications for managers, investors, and regulators. A better understanding of market reactions to share restructuring can support more informed decision-making, especially in dynamic capital markets such as Indonesia.

© 2026 The Authors. Published by IASE.

This is an

Keywords

Stock split, Stock return, Cumulative abnormal return, Event study, Indonesia stock exchange

Article history

Received 17 September 2025, Received in revised form 25 January 2026, Accepted 21 February 2026

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.Citation:

Suidarma IM, Putri NWOP, Dewi PAS, Putra IKKA, Sara IM, and Marsudiana IDN (2026). The impact of stock splits and reverse stock splits on stock returns in the Indonesian market. International Journal of Advanced and Applied Sciences, 13(2): 229-239

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (34)

Adamska A and Dąbrowski TJ (2021). Investor reactions to sustainability index reconstitutions: Analysis in different institutional contexts. Journal of Cleaner Production, 297: 126715. https://doi.org/10.1016/j.jclepro.2021.126715 [Google Scholar]

Adler HM, Nera MM, FoEh JEHJ, and Sinaga J (2024). Dividend policy as a moderating of the effect of dividend announcement on stock price in Indonesian firms. International Journal of Economics and Financial Issues, 14(4): 96-105. https://doi.org/10.32479/ijefi.16465 [Google Scholar]

Almeida DWLSD, Pimenta Júnior T, Gaio LE, and Lima FG (2024). Stock splits and reverse splits in the Brazilian capital market. Journal of Economics, Finance and Administrative Science, 29(58): 277–293. https://doi.org/10.1108/JEFAS-08-2021-0168 [Google Scholar]

Anhar M, Maronrong R, Burda A, and Sumail LO (2024). Dynamics of Indonesian stock market interconnection: Insights from selected ASEAN countries and global players during and after the COVID-19 pandemic. Investment Management and Financial Innovations, 21(2): 180-190. https://doi.org/10.21511/imfi.21(2).2024.14 [Google Scholar]

Blau BM, Cox JS, Griffith TG, and Voges R (2023). Daily short selling around reverse stock splits. Journal of Financial Markets, 65: 100832. https://doi.org/10.1016/j.finmar.2023.100832 [Google Scholar]

Burkart M and Zhong H (2023). Equity issuance methods and dilution. The Review of Corporate Finance Studies, 12(1): 78-130. https://doi.org/10.1093/rcfs/cfac029 [Google Scholar]

Chen J and Ausloos M (2023). A study about who is interested in stock splitting and why: Considering companies, shareholders, or managers. Journal of Risk and Financial Management, 16(2): 68. https://doi.org/10.3390/jrfm16020068 [Google Scholar]

Cowan AR (1993). Tests for cumulative abnormal returns over long periods: Simulation evidence. International Review of Financial Analysis, 2(1): 51-68. https://doi.org/10.1016/1057-5219(93)90006-4 [Google Scholar]

Ding W, Levine R, Lin C, and Xie W (2021). Corporate immunity to the COVID-19 pandemic. Journal of Financial Economics, 141(2): 802-830. https://doi.org/10.1016/j.jfineco.2021.03.005 [Google Scholar] PMid:34580557 PMCid:PMC8457922

Dudycz T and Brycz B (2021). Why the par value of share matters to investors. International Journal of Financial Studies, 9(1): 16. https://doi.org/10.3390/ijfs9010016 [Google Scholar]

Dutta A, Knif J, Kolari JW, and Pynnonen S (2018). A robust and powerful test of abnormal stock returns in long-horizon event studies. Journal of Empirical Finance, 47: 1-24. https://doi.org/10.1016/j.jempfin.2018.02.004 [Google Scholar]

Handayani SR and Rahayu SM (2019). Stock return and financial performance as moderation variable in influence of good corporate governance towards corporate value. Asian Journal of Accounting Research, 4(1): 18-34. https://doi.org/10.1108/AJAR-07-2018-0021 [Google Scholar]

How CC and Tsen WH (2019). The effects of stock split announcements on the stock returns in Bursa Malaysia. Jurnal Ekonomi Malaysia, 53(2): 41-53. https://doi.org/10.17576/JEM-2019-5302-4 [Google Scholar]

Iannino MC, Zhang M, and Zhuk S (2024). Signaling through timing of stock splits. Journal of Corporate Finance, 87: 102610. https://doi.org/10.1016/j.jcorpfin.2024.102610 [Google Scholar]

Liu Y and Haw IM (2022). On price difference of A+H companies. China Accounting and Finance Review, 24(2): 199-225. https://doi.org/10.1108/CAFR-02-2022-0012 [Google Scholar]

Liu Y, Liu X, Zhang Y, and Li S (2022). CEGH: A hybrid model using CEEMD, entropy, GRU, and history attention for intraday stock market forecasting. Entropy, 25(1): 71. https://doi.org/10.3390/e25010071 [Google Scholar] PMid:36673213 PMCid:PMC9857506

Lobanova O and Aidov A (2023). Reverse stock splits and liquidity in ETFs. Journal of Risk and Financial Management, 17(1): 4. https://doi.org/10.3390/jrfm17010004 [Google Scholar]

Marisetty N and Babu MS (2020). An empirical study on expected return models with reference to bonus issues and stock splits in Indian share market. International Journal of Management, 11(5): 1612-1630. https://doi.org/10.2139/ssrn.3731427 [Google Scholar]

Meza N, Báez A, Rodriguez J, and Toledo W (2020). The dividend signaling hypothesis and the corporate life cycle. Managerial Finance, 46(12): 1569-1587. https://doi.org/10.1108/MF-10-2019-0512 [Google Scholar]

Nayyar R, Dhamija S, and Mehta C (2023). Analysing the likelihood of and market reaction to reverse stock splits in India. Global Business Review. https://doi.org/10.1177/09721509231189916 [Google Scholar]

Ohlson JA and Penman SH (1985). Volatility increases subsequent to stock splits: An empirical aberration. Journal of Financial Economics, 14(2): 251-266. https://doi.org/10.1016/0304-405X(85)90017-0 [Google Scholar]

Pandey DK, Kumari V, and Tiwari BK (2022). Impacts of corporate announcements on stock returns during the global pandemic: Evidence from the Indian stock market. Asian Journal of Accounting Research, 7(2): 208-226. https://doi.org/10.1108/AJAR-06-2021-0097 [Google Scholar]

Perez MF, Shkilko A, Tang N, and van Nes P (2025). Stock split signalling: Evidence from short interest. Journal of Banking & Finance, 172: 107394. https://doi.org/10.1016/j.jbankfin.2025.107394 [Google Scholar]

Sia PC, Leong CM, and Puah CH (2023). Asymmetric effects of inflation rate changes on the stock market index: The case of Indonesia. Journal of International Studies, 16(1): 128-141. https://doi.org/10.14254/2071-8330.2023/16-1/9 [Google Scholar]

Song C (2020). Financial illiteracy and pension contributions: A field experiment on compound interest in China. The Review of Financial Studies, 33(2): 916-949. https://doi.org/10.1093/rfs/hhz074 [Google Scholar]

Sunardi S, Noviolla C, Supramono S, and Hermanto YB (2023). Stock market reaction to government policy on determining coal selling price. Heliyon, 9(2): e13454. https://doi.org/10.1016/j.heliyon.2023.e13454 [Google Scholar] PMid:36846662 PMCid:PMC9947261

Tabibian SA, Zhang Z, and Jafarian M (2020). How does split announcement affect stock liquidity? Evidence from Bursa Malaysia. Risks, 8(3): 85. https://doi.org/10.3390/risks8030085 [Google Scholar]

Titman S, Wei C, and Zhao B (2022). Corporate actions and the manipulation of retail investors in China: An analysis of stock splits. Journal of Financial Economics, 145(3): 762-787. https://doi.org/10.1016/j.jfineco.2021.09.018 [Google Scholar]

Tse YK, Dong K, Sun R, and Mason R (2024). Recovering from geopolitical risk: An event study of Huawei's semiconductor supply chain. International Journal of Production Economics, 275: 109347. https://doi.org/10.1016/j.ijpe.2024.109347 [Google Scholar]

West J, Azab C, Ma KC, and Bitter M (2020). Numerosity: Forward and reverse stock splits. Journal of Behavioral Finance, 21(3): 323-335. https://doi.org/10.1080/15427560.2019.1672168 [Google Scholar]

Wiguna IGNH, Dewi NAWT, and Yasa INP (2021). Financial market performance affected by the COVID-19 case: Study on Indonesian composite stock index. Advances in Economics, Business and Management Research, 197: 165-172. https://doi.org/10.2991/aebmr.k.211124.025 [Google Scholar]

Woo KY, Mai C, McAleer M, and Wong WK (2020). Review on efficiency and anomalies in stock markets. Economies, 8(1): 20. https://doi.org/10.3390/economies8010020 [Google Scholar]

Woo M and Kim MA (2021). Option volume and stock returns: Evidence from single stock options on the Korea Exchange. Journal of Derivatives and Quantitative Studies, 29(4): 280-300. https://doi.org/10.1108/JDQS-06-2021-0012 [Google Scholar]

- Zhang P, Xu K, Huang J, and Qi J (2024). Investor sentiment and the holiday effect in the cryptocurrency market: Evidence from China. Financial Innovation, 10: 113. https://doi.org/10.1186/s40854-024-00639-x [Google Scholar]