International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 13, Issue 1 (January 2026), Pages: 239-246

----------------------------------------------

Original Research Paper

Forecasting central bank policy rates using machine learning and deep learning approaches

Author(s):

Affiliation(s):

1Department of Economics, Mandakh University, Ulan Bator, Mongolia

2Department of Information Technology, Institute of Mathematics and Digital Technology, Ulan Bator, Mongolia

3Interdisciplinary Studies Department, University of Finance and Economics, Ulan Bator, Mongolia

4Department of Management, Management School, Mongolian University of Science and Technology, Ulan Bator, Mongolia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-5379-1630

Corresponding author's ORCID profile: https://orcid.org/0000-0002-5379-1630

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2026.01.025

Abstract

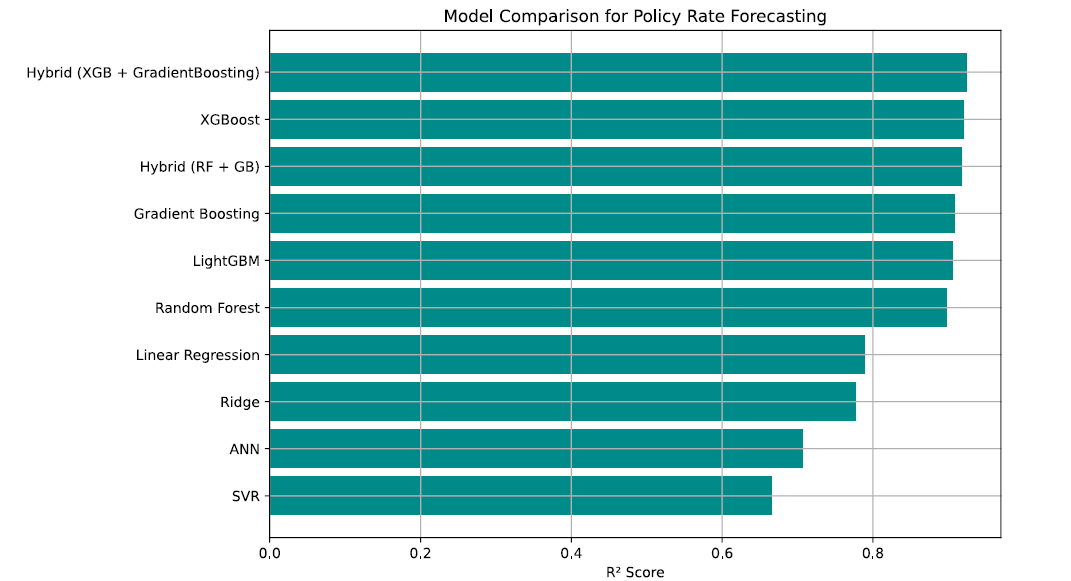

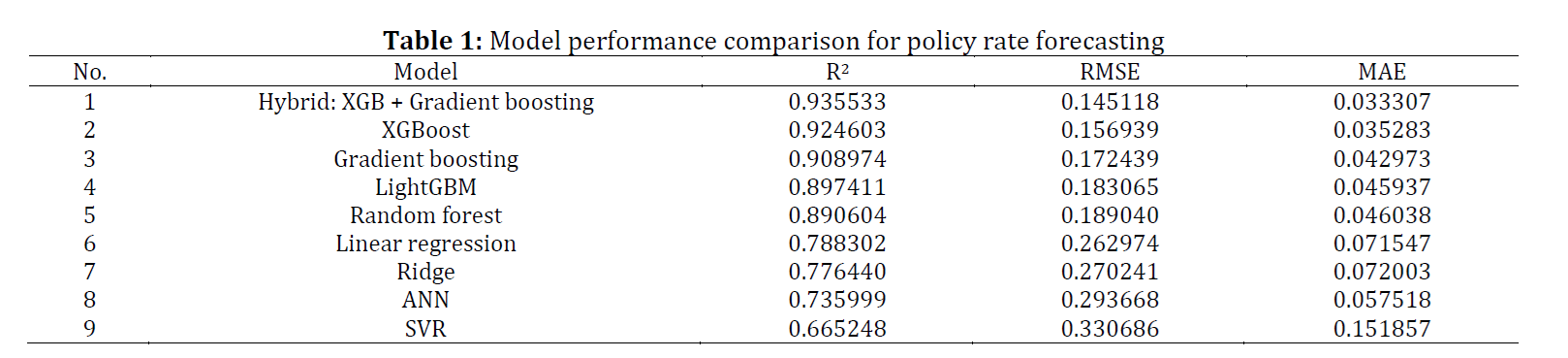

Accurate forecasting of central bank policy rates is essential for effective monetary policy, stable market expectations, and overall macroeconomic stability. In emerging economies such as Mongolia, traditional econometric models, including the Taylor Rule, ARIMA, and SVAR, often fail to adequately capture nonlinear relationships, time dependencies, and structural changes in the economy. To address these limitations, this study develops and evaluates advanced forecasting approaches based on hybrid combinations of machine learning and deep learning models. The analysis uses a monthly dataset consisting of 26 macroeconomic variables from January 2008 to December 2024. Seven forecasting models are constructed and evaluated using RMSE, MAE, and R² performance measures. The results indicate that hybrid models, particularly XGBoost combined with Gradient Boosting and LSTM integrated with XGBoost, achieve the highest forecasting accuracy, with the best model attaining an R² value of 0.9355. Overall, the hybrid approaches outperform both conventional econometric models and individual machine learning or deep learning models in capturing complex macroeconomic dynamics and structural shifts. These findings offer a reliable data-driven framework to support monetary policy decisions in Mongolia and provide a methodology that can be applied to other emerging economies with similar economic conditions.

© 2026 The Authors. Published by IASE.

This is an

Keywords

Policy rate forecasting, Hybrid machine learning, Deep learning models, Monetary policy analysis, Emerging economies

Article history

Received 29 July 2025, Received in revised form 9 January 2026, Accepted 23 January 2026

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Sodnomdavaa T, Badrakh O, Altangerel D, and Sodnomdavaa T (2026). Forecasting central bank policy rates using machine learning and deep learning approaches. International Journal of Advanced and Applied Sciences, 13(1): 239-246

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

----------------------------------------------

References (23)

- Aruoba SB and Drechsel T (2024). Identifying monetary policy shocks: A natural language approach. NBER Working Paper 32417. https://doi.org/10.3386/w32417 [Google Scholar]

- Bates JM and Granger CW (1969). The combination of forecasts. Journal of the Operational Research Society, 20(4): 451-468. https://doi.org/10.1057/jors.1969.103 [Google Scholar]

- Brubakk L, ter Ellen S, and Xu H (2021). Central bank communication through interest rate projections. Journal of Banking & Finance, 124: 106044. https://doi.org/10.1016/j.jbankfin.2021.106044 [Google Scholar]

- Clarida R, Gali J, and Gertler M (1999). The science of monetary policy: A new Keynesian perspective. Journal of Economic Literature, 37(4): 1661-1707. https://doi.org/10.1257/jel.37.4.1661 [Google Scholar]

- Clemen RT (1989). Combining forecasts: A review and annotated bibliography. International Journal of Forecasting, 5(4): 559-583. https://doi.org/10.1016/0169-2070(89)90012-5 [Google Scholar]

- Cogley T and Sargent TJ (2005). Drifts and volatilities: Monetary policies and outcomes in the post WWII US. Review of Economic Dynamics, 8(2): 262-302. https://doi.org/10.1016/j.red.2004.10.009 [Google Scholar]

- Diebold FX and Mariano RS (2002). Comparing predictive accuracy. Journal of Business & Economic Statistics, 20(1): 134-144. https://doi.org/10.1198/073500102753410444 [Google Scholar]

- Elliott G, Komunjer I, and Timmermann A (2008). Biases in macroeconomic forecasts: Irrationality or asymmetric loss? Journal of the European Economic Association, 6(1): 122-157. https://doi.org/10.1162/JEEA.2008.6.1.122 [Google Scholar]

- Goodfriend M (1983). Discount window borrowing, monetary policy, and the post-October 6, 1979 Federal Reserve operating procedure. Journal of Monetary Economics, 12(3): 343-356. https://doi.org/10.1016/0304-3932(83)90058-2 [Google Scholar]

- Hinterlang N (2020). Predicting monetary policy using artificial neural networks. Discussion Paper No. 44/2020, Deutsche Bundesbank, Frankfurt am Main, Germany. https://doi.org/10.2139/ssrn.3669522 [Google Scholar]

- Hinterlang N and Hollmayr J (2022). Classification of monetary and fiscal dominance regimes using machine learning techniques. Journal of Macroeconomics, 74: 103469. https://doi.org/10.1016/j.jmacro.2022.103469 [Google Scholar]

- Koop G and Korobilis D (2013). Large time-varying parameter VARs. Journal of Econometrics, 177(2): 185-198. https://doi.org/10.1016/j.jeconom.2013.04.007 [Google Scholar]

- Mullainathan S and Spiess J (2017). Machine learning: An applied econometric approach. Journal of Economic Perspectives, 31(2): 87-106. https://doi.org/10.1257/jep.31.2.87 [Google Scholar]

- Patton AJ and Timmermann A (2007). Testing forecast optimality under unknown loss. Journal of the American Statistical Association, 102(480): 1172-1184. https://doi.org/10.1198/016214506000001176 [Google Scholar]

- Pettenuzzo D and Timmermann A (2017). Forecasting macroeconomic variables under model instability. Journal of Business and Economic Statistics, 35(2): 183-201. https://doi.org/10.1080/07350015.2015.1051183 [Google Scholar]

- Primiceri GE (2005). Time varying structural vector autoregressions and monetary policy. The Review of Economic Studies, 72(3): 821-852. https://doi.org/10.1111/j.1467-937X.2005.00353.x [Google Scholar]

- Sodnomdavaa T, Sodnomdavaa T, and Amgalanbat N (2025). Possibility of predicting inflation: Using machine learning model. International Journal of Social Science and Humanities Research, 5(2): 49–64. [Google Scholar]

- Stock JH and Watson MW (1999). Forecasting inflation. Journal of Monetary Economics, 44(2): 293-335. https://doi.org/10.3386/w7023 [Google Scholar]

- Stock JH and Watson MW (2004). Combination forecasts of output growth in a seven‐country data set. Journal of Forecasting, 23(6): 405-430. https://doi.org/10.1002/for.928 [Google Scholar]

- Svensson LE (1997). Inflation forecast targeting: Implementing and monitoring inflation targets. European Economic Review, 41(6): 1111-1146. https://doi.org/10.1016/S0014-2921(96)00055-4 [Google Scholar]

- Taylor J (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39(1): 195-214. https://doi.org/10.1016/0167-2231(93)90009-L [Google Scholar]

- Woodford M and Walsh CE (2005). Interest and prices: Foundations of a theory of monetary policy. Macroeconomic Dynamics, 9(3): 462-468. https://doi.org/10.1017/S1365100505040253 [Google Scholar]

- Wright JH (2009). Forecasting US inflation by Bayesian model averaging. Journal of Forecasting, 28(2): 131-144. https://doi.org/10.1002/for.1088 [Google Scholar]