International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 13, Issue 1 (January 2026), Pages: 101-114

----------------------------------------------

Original Research Paper

Foreign investors as guardians or colluders? The moderating role of IFRS in corporate tax avoidance in Korea

Author(s):

Affiliation(s):

Department of Accounting and Taxation, Hanbat National University, Daejeon, South Korea

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-3344-8648

Corresponding author's ORCID profile: https://orcid.org/0000-0003-3344-8648

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2026.01.011

Abstract

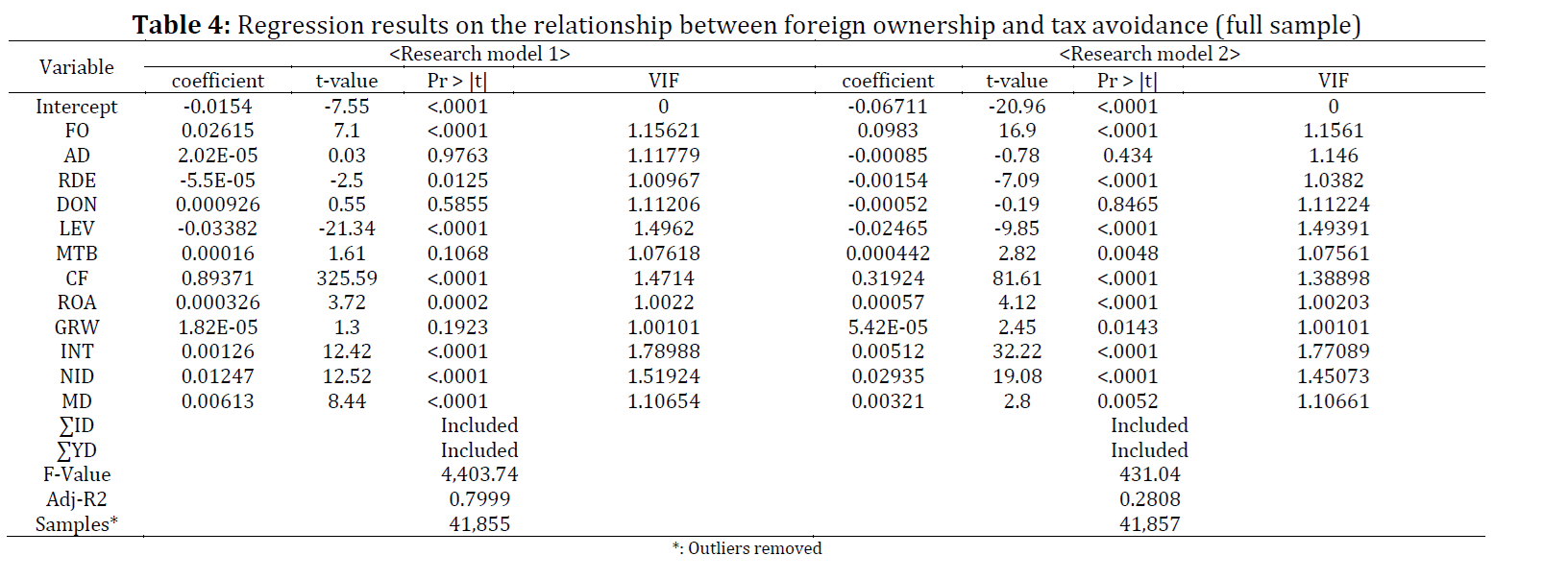

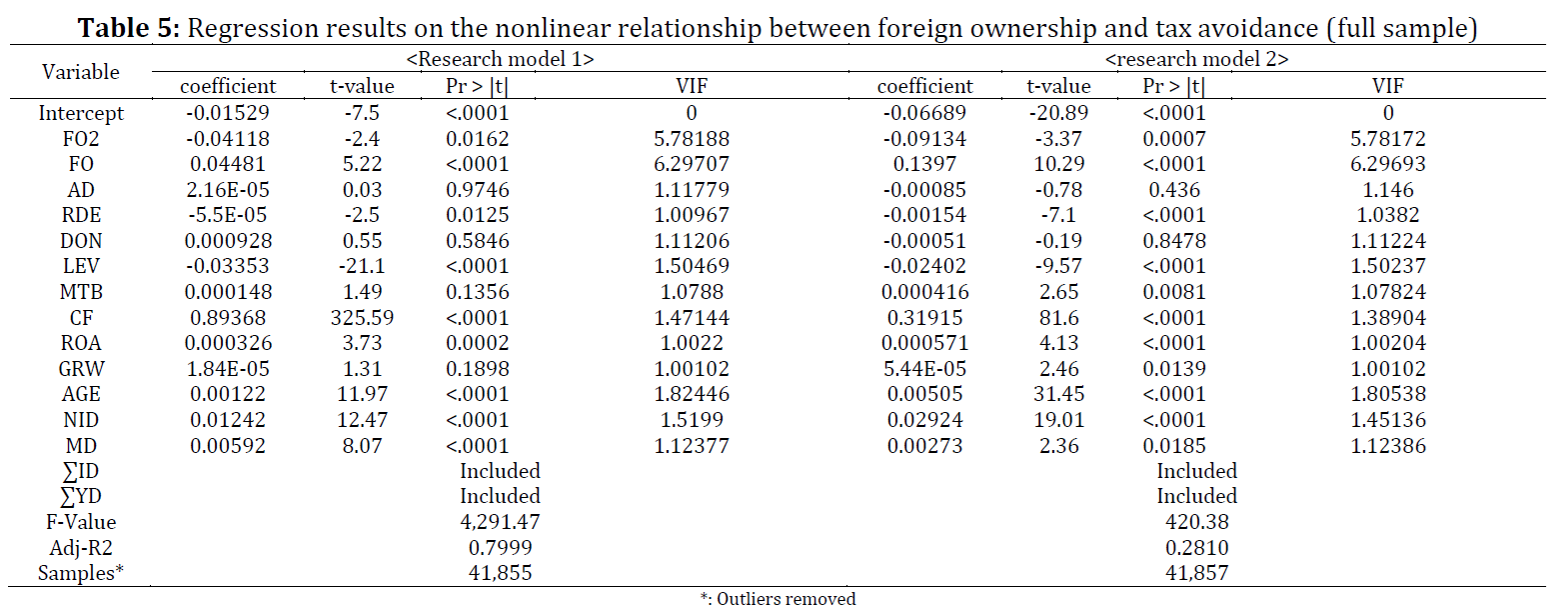

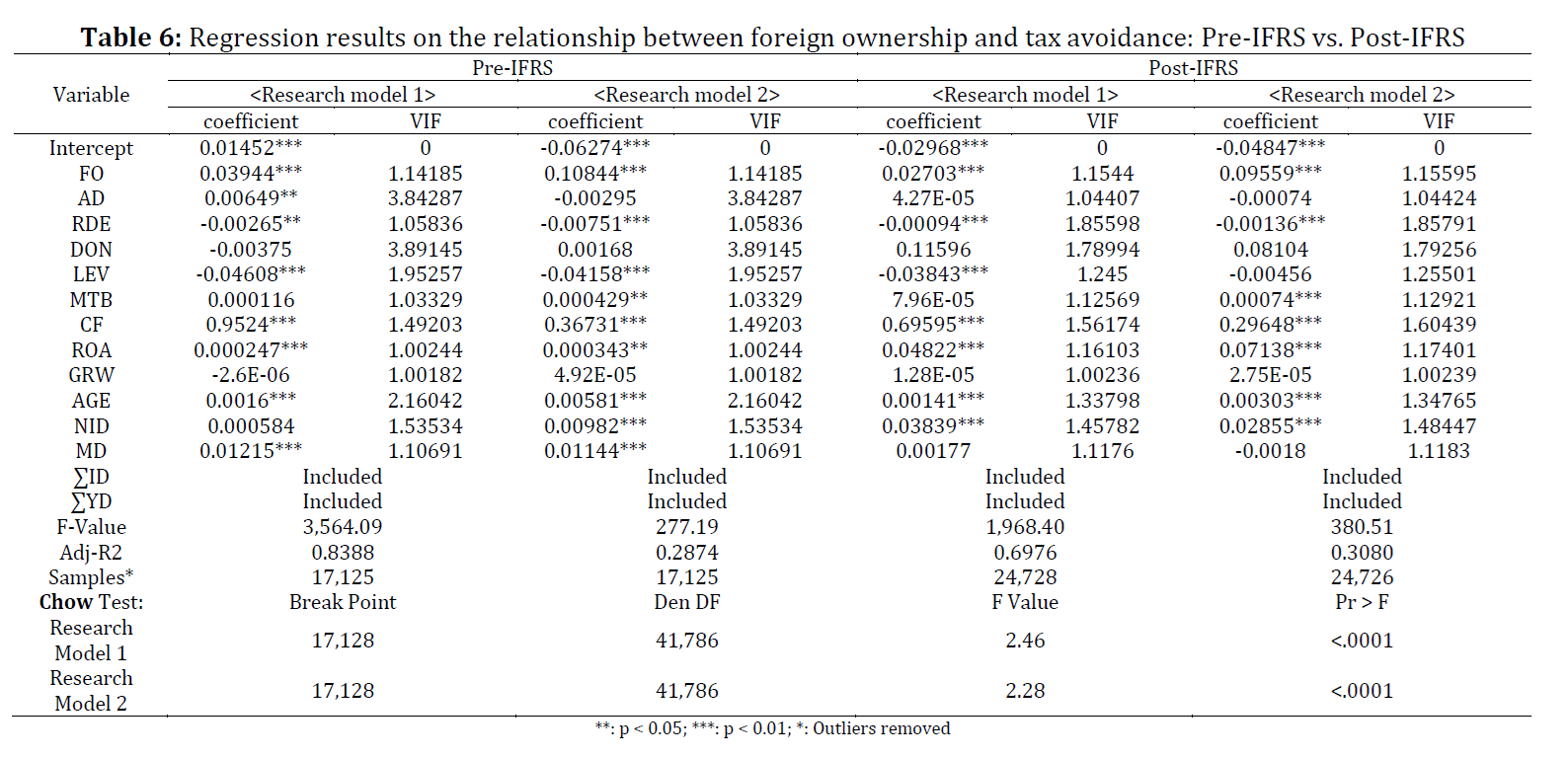

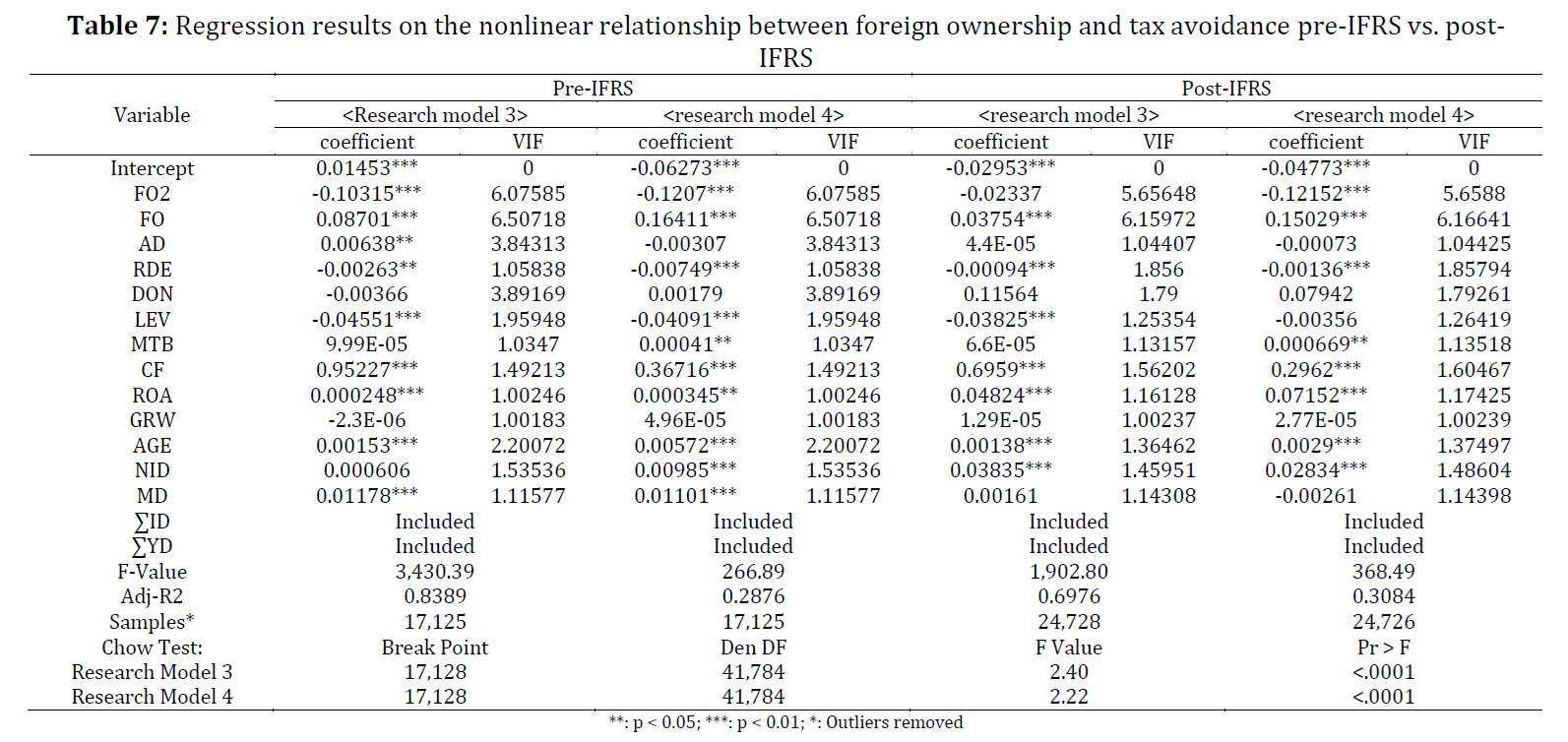

This study examines the effect of foreign ownership on corporate tax avoidance among firms listed on the Korean stock market and investigates whether this relationship is nonlinear and moderated by the adoption of International Financial Reporting Standards (IFRS) in 2011. As foreign investors have become more influential in Korea’s capital market, they play an important role in shaping firms’ tax behavior. While prior studies suggest that foreign ownership can reduce tax avoidance through stronger monitoring, this study also considers whether high levels of foreign ownership may support managerial interests or allow aggressive tax practices. Using panel data from KOSPI- and KOSDAQ-listed firms from 2001 to 2023, tax avoidance is measured by book-tax differences (BTD) and discretionary book-tax differences (DDBTD). The results reveal an inverted U-shaped relationship between foreign ownership and tax avoidance, indicating that tax avoidance increases at low levels of foreign ownership but decreases after reaching a certain threshold due to enhanced monitoring. This relationship remains after IFRS adoption, although the degree of nonlinearity becomes weaker in the post-IFRS period. These findings suggest that the influence of foreign ownership on corporate tax behavior depends on both the level of ownership and changes in the institutional environment, and they provide important implications for understanding the governance role of foreign investors in emerging markets.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Foreign ownership, Tax avoidance, Nonlinear relationship, IFRS adoption, Corporate governance

Article history

Received 8 August 2025, Received in revised form 9 December 2025, Accepted 16 December 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Kwon GJ (2026). Foreign investors as guardians or colluders? The moderating role of IFRS in corporate tax avoidance in Korea. International Journal of Advanced and Applied Sciences, 13(1): 101-114

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (18)

- Athira A and Ramesh VK (2023). COVID-19 and corporate tax avoidance: International evidence. International Business Review, 32(4): 102143. https://doi.org/10.1016/j.ibusrev.2023.102143 [Google Scholar] PMid:37235071 PMCid:PMC10198770

- Balakrishnan K, Blouin JL, and Guay WR (2019). Tax aggressiveness and corporate transparency. The Accounting Review, 94(1): 45-69. https://doi.org/10.2308/accr-52130 [Google Scholar]

- Braga RN (2017). Effects of IFRS adoption on tax avoidance. Revista Contabilidade & Finanças, 28(75): 407-424. https://doi.org/10.1590/1808-057x201704680 [Google Scholar]

- Choi J and Park H (2022). Tax avoidance, tax risk, and corporate governance: Evidence from Korea. Sustainability, 14(1): 469. https://doi.org/10.3390/su14010469 [Google Scholar]

- Chow GC (1960). Tests of equality between sets of coefficients in two linear regressions. Econometrica, 28(3): 591-605. https://doi.org/10.2307/1910133 [Google Scholar]

- Desai MA and Dharmapala D (2006). Corporate tax avoidance and high-powered incentives. Journal of Financial Economics, 79(1): 145-179. https://doi.org/10.1016/j.jfineco.2005.02.002 [Google Scholar]

- Desai MA and Dharmapala D (2009). Corporate tax avoidance and firm value. The Review of Economics and Statistics, 91(3): 537-546. https://doi.org/10.1162/rest.91.3.537 [Google Scholar]

- Desai MA, Dyck A, and Zingales L (2007). Theft and taxes. Journal of Financial Economics, 84(3): 591-623. https://doi.org/10.1016/j.jfineco.2006.05.005 [Google Scholar]

- Ebaid IES (2024). Does the implementation of IFRS improve transparency regarding the company's financial conditions? Evidence from an emerging market. PSU Research Review, 8(2): 498-513. https://doi.org/10.1108/PRR-11-2021-0063 [Google Scholar]

- Goh YS and Seo YM (2014). Revisiting the monitoring role of foreign investors-investment horizons of foreign investors and corporate tax avoidance. Journal of Tax Studies, 31(1): 73-104. [Google Scholar]

- Kang J (2012). Impacts of IFRS on corporate tax legislation: With special reference to South Korea's reforms. The Kyoto Economic Review, 81(2): 106-131. [Google Scholar]

- Key KG and Kim JY (2020). IFRS and accounting quality: Additional evidence from Korea. Journal of International Accounting, Auditing and Taxation, 39: 100306. https://doi.org/10.1016/j.intaccaudtax.2020.100306 [Google Scholar]

- Morck R, Shleifer A, and Vishny RW (1988). Management ownership and market valuation: An empirical analysis. Journal of Financial Economics, 20: 293-315. https://doi.org/10.1016/0304-405X(88)90048-7 [Google Scholar]

- Nguyen HTT, Nguyen HTT, and Van Nguyen C (2023). Analysis of factors affecting the adoption of IFRS in an emerging economy. Heliyon, 9(6): e17331. https://doi.org/10.1016/j.heliyon.2023.e17331 [Google Scholar] PMid:37389083 PMCid:PMC10300374

- Okafor ON, Akindayomi A, and Warsame H (2019). Did the adoption of IFRS affect corporate tax avoidance. Canadian Tax Journal, 67(4): 947–979. https://doi.org/10.32721/ctj.2019.67.4.okafor [Google Scholar]

- Park JK and Hong YE (2009). Corporate tax avoidance and foreign ownership. Korean Study on Taxation, 26(1): 105-135. [Google Scholar]

- Plesko GA (2004). Corporate tax avoidance and the properties of corporate earnings. National Tax Journal, 57(3): 729-737. https://doi.org/10.17310/ntj.2004.3.12 [Google Scholar]

- Shi AA, Concepcion FR, Laguinday CM, Ong Hian Huy TA, and Unite AA (2020). An analysis of the effects of foreign ownership on the level of tax avoidance across Philippine publicly listed firms. DLSU Business & Economics Review, 30(1): 3. https://doi.org/10.59588/2243-786X.1115 [Google Scholar]