International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 9 (September 2025), Pages: 220-229

----------------------------------------------

Original Research Paper

The risk-return relationship in Vietnam’s stock market: A weak connection

Author(s):

Affiliation(s):

Faculty of Economics, Ho Chi Minh City University of Technology and Education, Ho Chi Minh City, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-4068-5190

Corresponding author's ORCID profile: https://orcid.org/0000-0003-4068-5190

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.09.022

Abstract

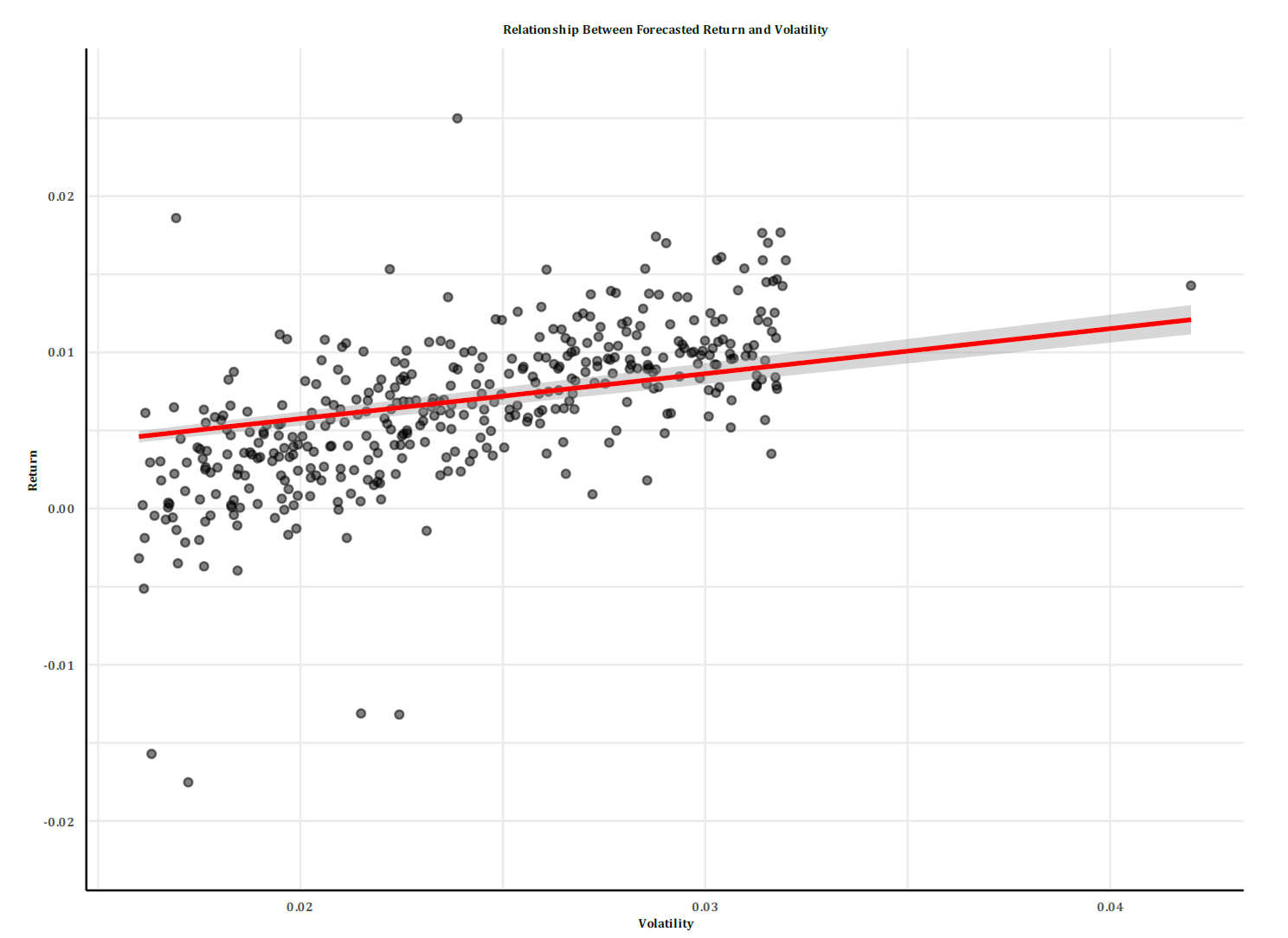

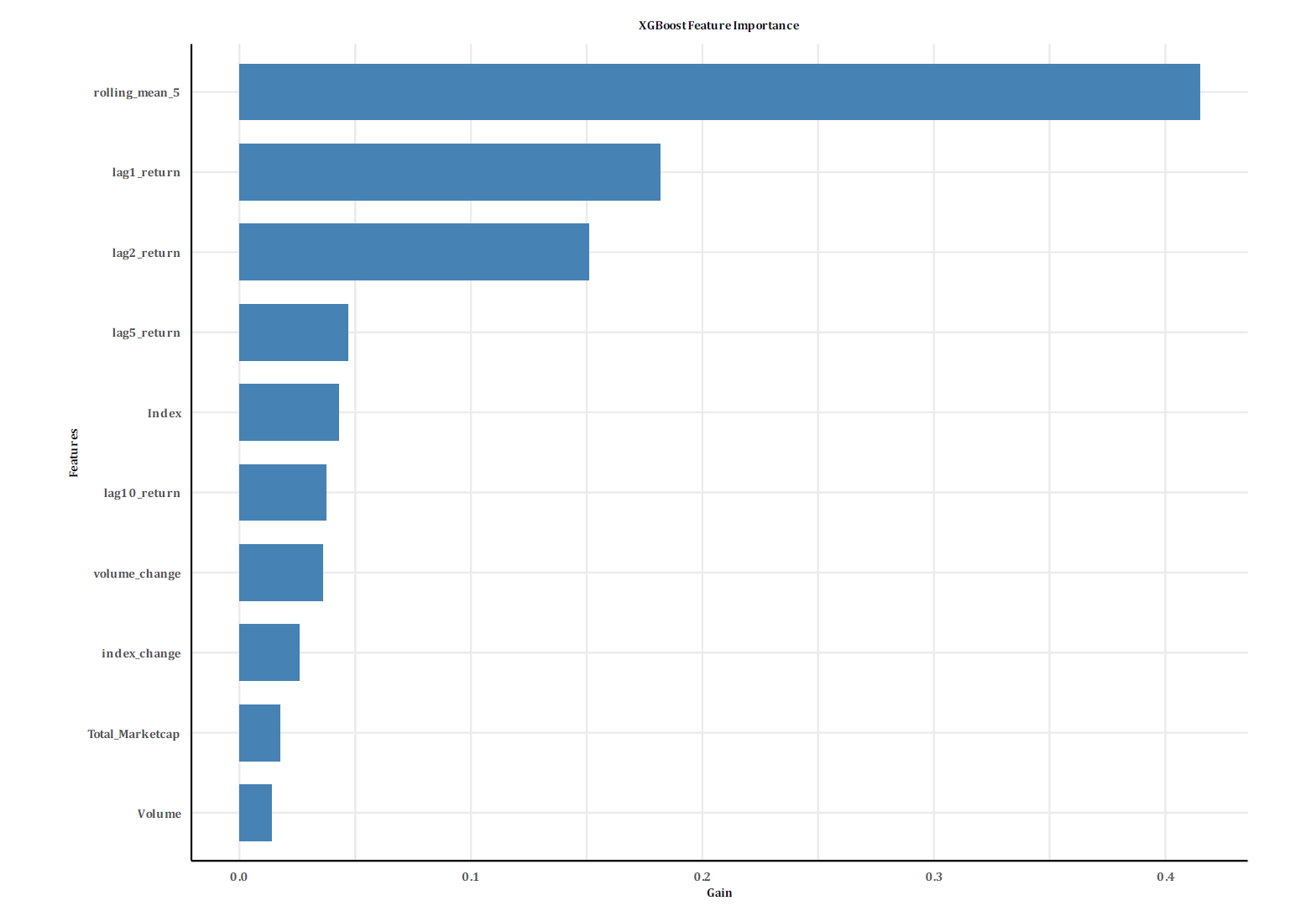

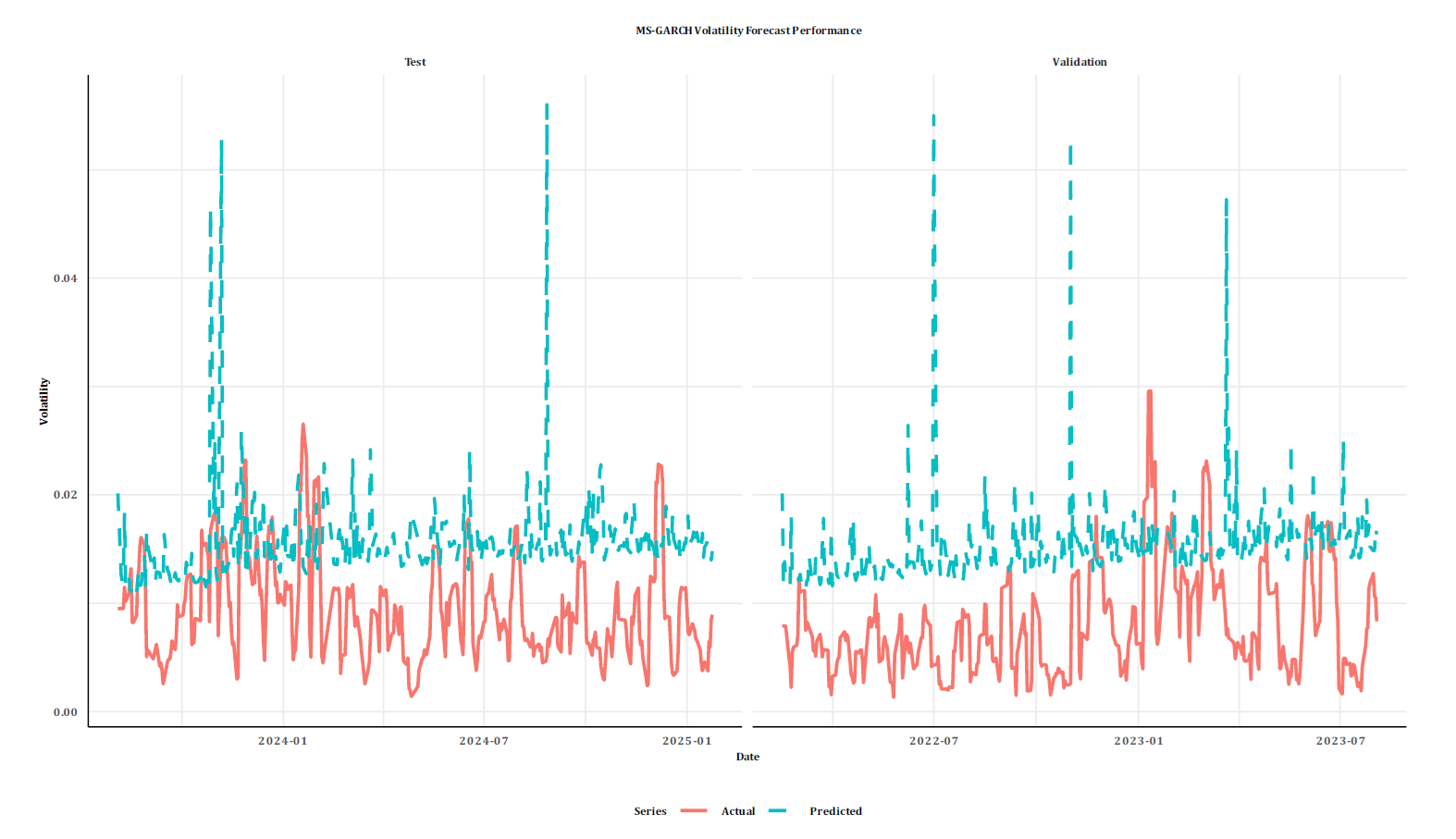

Vietnam’s stock market is one of the fastest-growing in Asia, marked by high volatility and a strong presence of retail investors. This study examines the relationship between volatility, commonly viewed as a measure of risk, and expected returns, challenging the traditional belief that higher risk leads to higher returns. The findings show a statistically significant but economically weak connection, suggesting that volatility has a limited influence on returns. The results highlight the unique characteristics of Vietnam’s market, where speculative trading, retail investor behavior, and structural constraints play a larger role than standard risk-return patterns. Instead of aligning with the capital asset pricing model (CAPM), returns are mainly driven by short-term momentum and market sentiment. This study contributes to asset pricing literature by stressing the need for market-specific models in emerging economies and offers insights for investors and policymakers seeking to strengthen market performance and stability.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Stock volatility, Expected returns, Retail investors, Market sentiment, Emerging markets

Article history

Received 13 April 2025, Received in revised form 7 August 2025, Accepted 22 August 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Pham H, Dang VQ, Tuyet NHT, and Vuong QD (2025). The risk-return relationship in Vietnam’s stock market: A weak connection. International Journal of Advanced and Applied Sciences, 12(9): 220-229

Figures

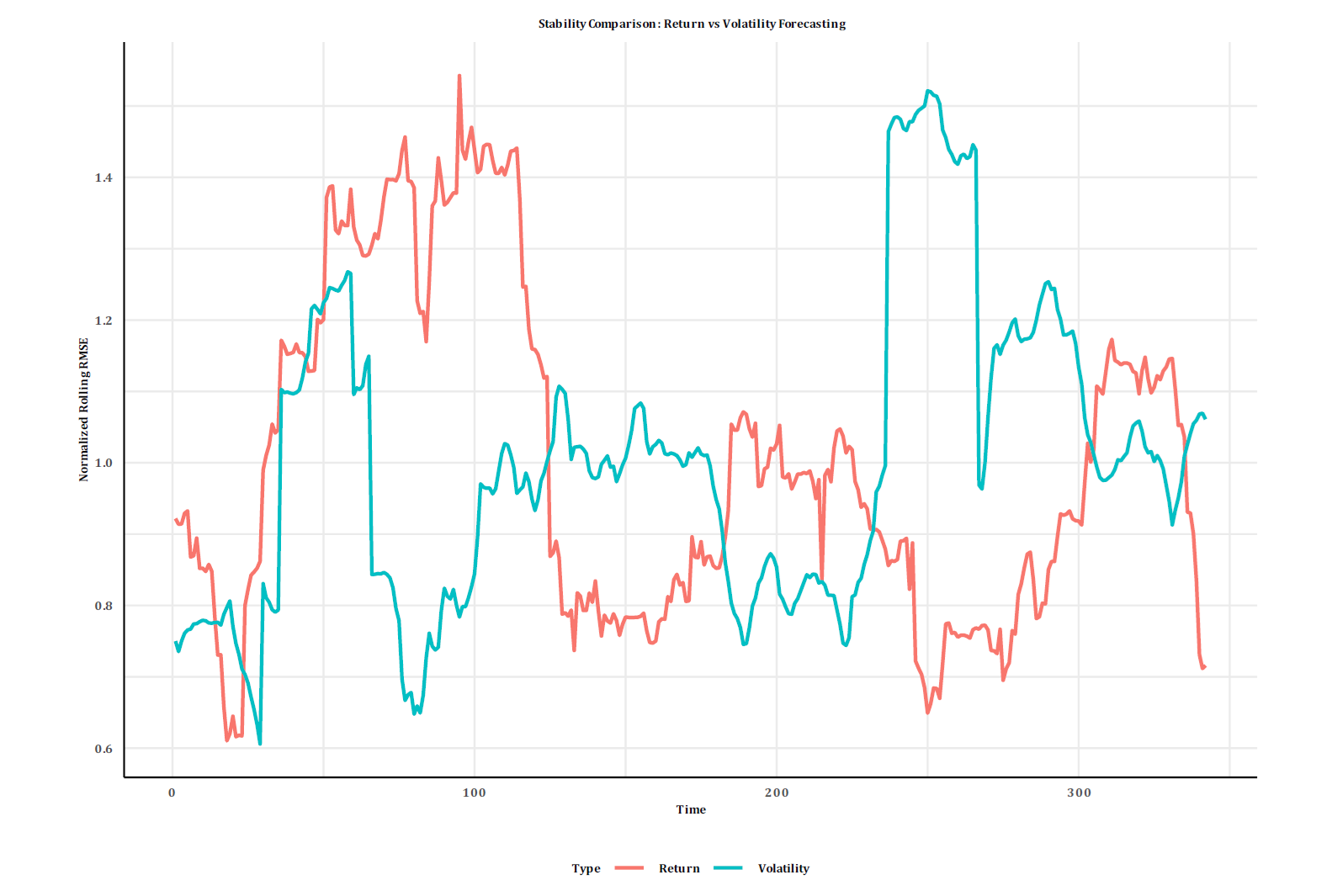

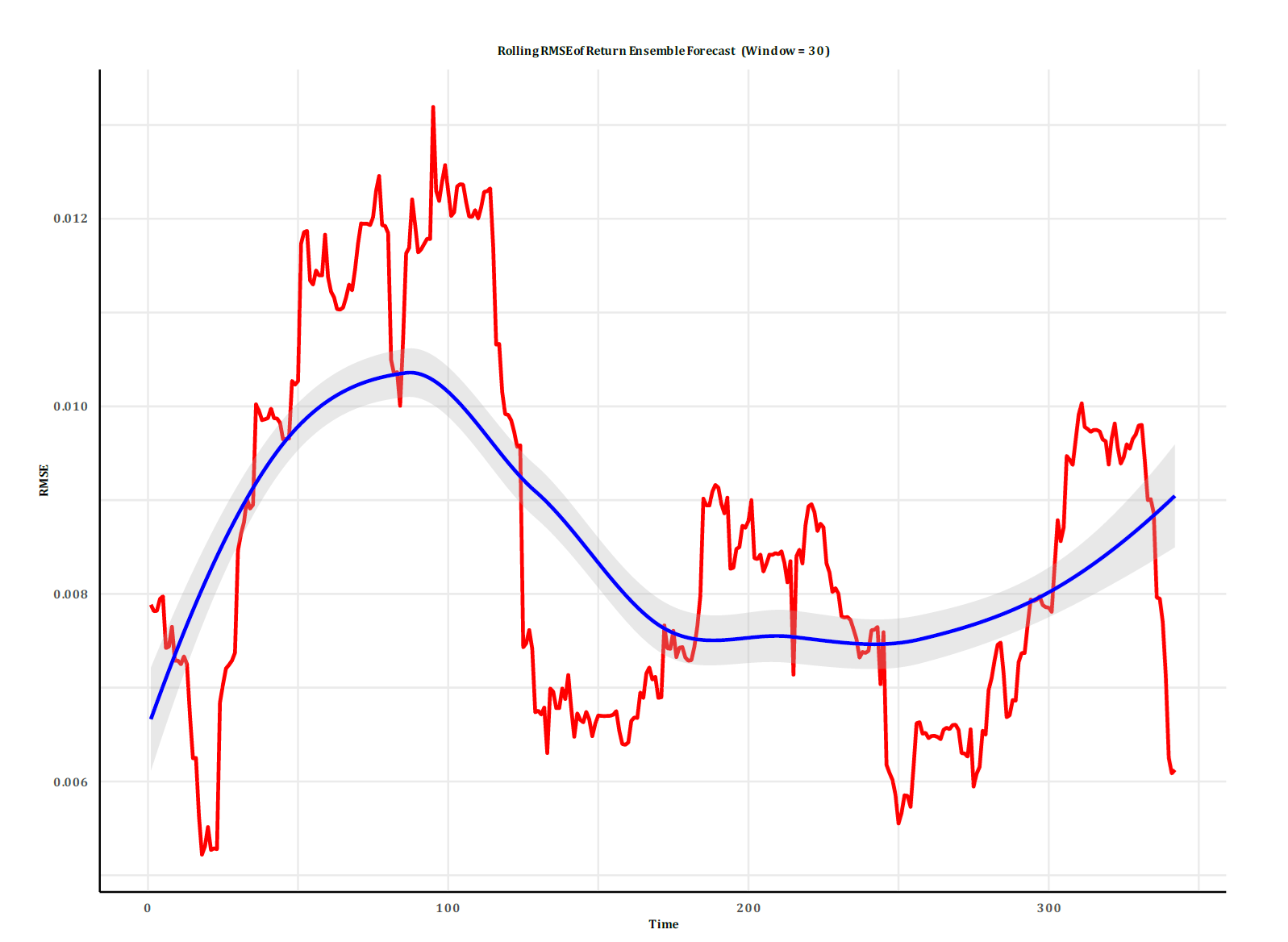

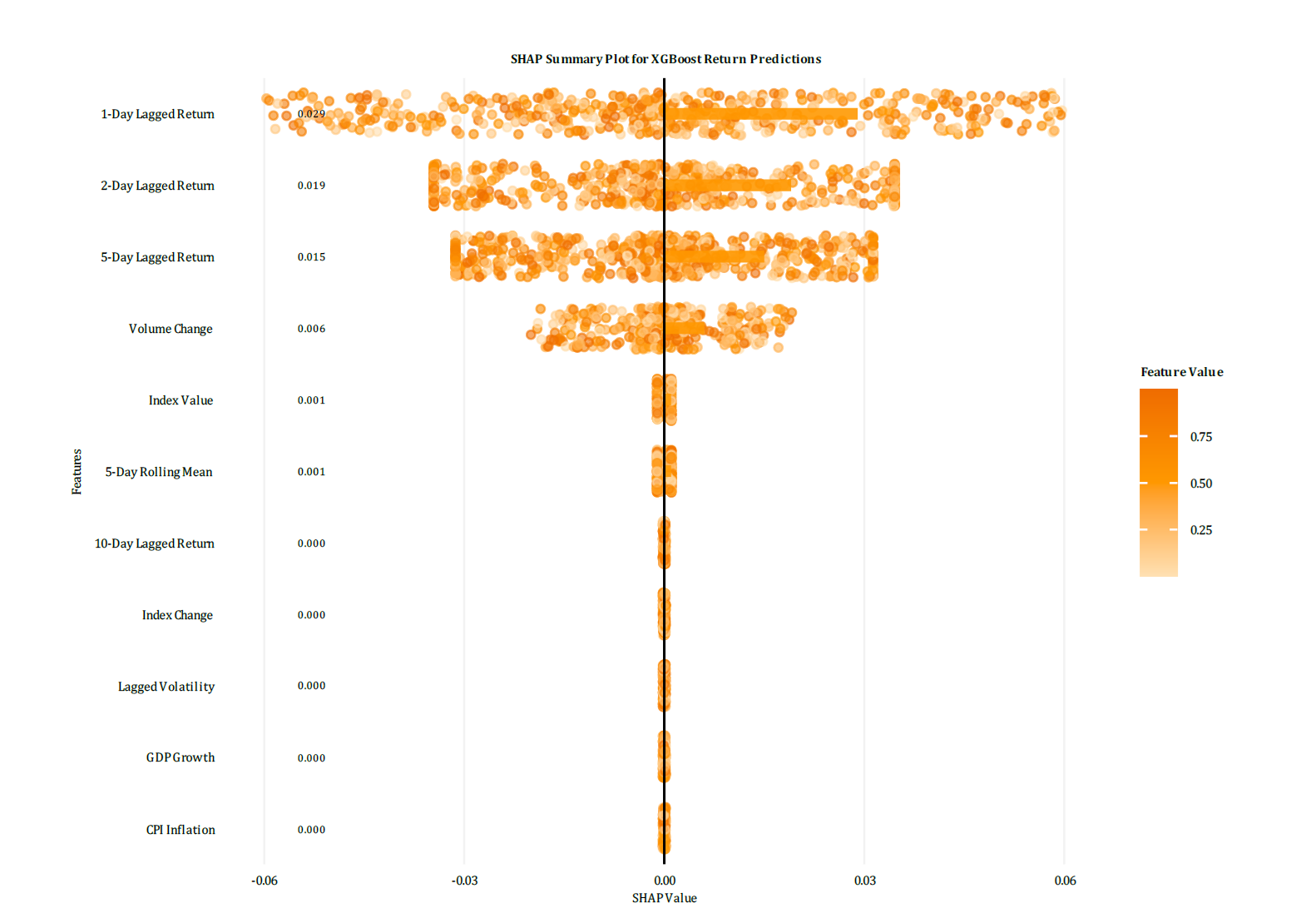

Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

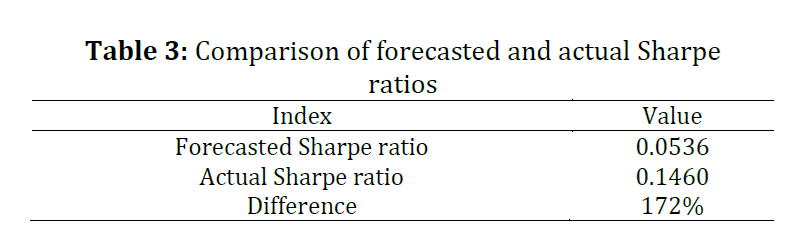

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (32)

- AFC (2025). Vietnam stock exchanges market capitalization March 2025. Asia Frontier Capital. Available online at: https://www.asiafrontiercapital.com/vietnam.html

- Ané T and Geman H (2000). Order flow, transaction clock, and normality of asset returns. The Journal of Finance, 55: 2259–2284. https://doi.org/10.1111/0022-1082.00286 [Google Scholar]

- Ang A, Hodrick RJ, Xing Y, and Zhang X (2006). The cross-section of volatility and expected returns. The Journal of Finance, 61: 259–299. https://doi.org/10.1111/j.1540-6261.2006.00836.x [Google Scholar]

- Baker M, Bradley B, and Wurgler J (2011). Benchmarks as limits to arbitrage: Understanding the low-volatility anomaly. Financial Analysts Journal, 67(1): 40–54. https://doi.org/10.2469/faj.v67.n1.4 [Google Scholar]

- Batten JA and Vo XV (2014). Liquidity and return relationships in an emerging market. Emerging Markets Finance and Trade, 50(1): 5–21. https://doi.org/10.2753/REE1540-496X500101 [Google Scholar]

- Carhart MM (1997). On persistence in mutual fund performance. The Journal of Finance, 52: 57–82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x [Google Scholar]

- Chen T and Guestrin C (2016). XGBoost: A scalable tree boosting system. In the Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, ACM, San Francisco, USA: 785–794. https://doi.org/10.1145/2939672.2939785 [Google Scholar]

- Cont R (2001). Empirical properties of asset returns: Stylized facts and statistical issues. Quantitative Finance, 1: 223. https://doi.org/10.1080/713665670 [Google Scholar]

- Engle R (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 20(3): 339–350. https://doi.org/10.1198/073500102288618487 [Google Scholar]

- Fama EF and French KR (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1): 3–56. https://doi.org/10.1016/0304-405X(93)90023-5 [Google Scholar]

- Frazzini A and Pedersen LH (2014). Betting against beta. Journal of Financial Economics, 111(1): 1–25. https://doi.org/10.1016/j.jfineco.2013.10.005 [Google Scholar]

- Glosten LR, Jagannathan R, and Runkle DE (1993). On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance, 48: 1779–1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x [Google Scholar]

- Goutte S, Le HV, Liu F, and von Mettenheim HJ (2025). Mcda strategies for portfolio optimization: A case study on Vietnamese stock market dynamics. Annals of Operations Research. https://doi.org/10.1007/s10479-025-06736-z [Google Scholar]

- Haas M, Mittnik S, and Paolella MS (2004). A new approach to Markov-switching GARCH models. Journal of Financial Econometrics, 2(4): 493–530. https://doi.org/10.1093/jjfinec/nbh020 [Google Scholar]

- Harvey CR (1995). Predictable risk and returns in emerging markets. The Review of Financial Studies, 8(3): 773–816. https://doi.org/10.1093/rfs/8.3.773 [Google Scholar]

- Hastie T, Tibshirani R, and Friedman J (2009). The elements of statistical learning: Data mining, inference, and prediction. Second Edition, Springer, New York, USA. https://doi.org/10.1007/978-0-387-84858-7 [Google Scholar]

- Henrique BM, Sobreiro VA, and Kimura H (2019). Literature review: Machine learning techniques applied to financial market prediction. Expert Systems with Applications, 124: 226–251. https://doi.org/10.1016/j.eswa.2019.01.012 [Google Scholar]

- Lintner J (1965). The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 47(1): 13–37. https://doi.org/10.2307/1924119 [Google Scholar]

- Loc TD, Lanjouw G, and Lensink R (2006). The impact of privatization on firm performance in a transition economy. Economics of Transition, 14: 349-389. https://doi.org/10.1111/j.1468-0351.2006.00251.x [Google Scholar]

- Markowitz H (1952). Portfolio selection. The Journal of Finance, 7(1): 77–91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x [Google Scholar]

- Narayan PK and Narayan S (2010). Modelling the impact of oil prices on Vietnam’s stock prices. Applied Energy, 87(1): 356–361. https://doi.org/10.1016/j.apenergy.2009.05.037 [Google Scholar]

- Nartea GV, Kong D, and Wu J (2017). Do extreme returns matter in emerging markets? Evidence from the Chinese stock market. Journal of Banking & Finance, 76: 189–197. https://doi.org/10.1016/j.jbankfin.2016.12.008 [Google Scholar]

- Nelson DB (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica, 59(2): 347–370. https://doi.org/10.2307/2938260 [Google Scholar]

- Nguyen LTM (2023). COVID-19 pandemic and stock returns volatility: Evidence from Vietnam’s stock market. Ho Chi Minh City Open University Journal of Science – Economics and Business Administration, 13(1): 156–168. https://doi.org/10.46223/HCMCOUJS.econ.en.13.1.2054.2023 [Google Scholar]

- Nguyen T, Locke S, and Reddy K (2015). Ownership concentration and corporate performance from a dynamic perspective: Does national governance quality matter? International Review of Financial Analysis, 41: 148–161. https://doi.org/10.1016/j.irfa.2015.06.005 [Google Scholar]

- Rouwenhorst KG (1999). Local return factors and turnover in emerging stock markets. The Journal of Finance, 54: 1439–1464. https://doi.org/10.1111/0022-1082.00151 [Google Scholar]

- Sharpe WF (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19: 425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x [Google Scholar]

- Truong LD, Cao GN, Friday HS, and Doan NT (2023). Overreaction in a frontier market: Evidence from the Ho Chi Minh stock exchange. International Journal of Financial Studies, 11(2): 58. https://doi.org/10.3390/ijfs11020058 [Google Scholar]

- VIR (2024). Vietnam’s stock market remains resilient in 2024. Vietnam Investment Review. Available online at: https://vir.com.vn/vietnams-stock-market-remains-resilient-in-2024-113372.html

- Vo XV and Phan THA (2019). Herd behavior and idiosyncratic volatility in a frontier market. Pacific-Basin Finance Journal, 53: 321–330. https://doi.org/10.1016/j.pacfin.2018.10.005 [Google Scholar]

- Wang W and Liang Z (2024). Financial distress early warning for Chinese enterprises from a systemic risk perspective: Based on the adaptive weighted XGBoost-bagging model. Systems, 12(2): 65. https://doi.org/10.3390/systems12020065 [Google Scholar]

- Zaremba A and Czapkiewicz A (2017). Digesting anomalies in emerging European markets: A comparison of factor pricing models. Emerging Markets Review, 31: 1–15. https://doi.org/10.1016/j.ememar.2016.12.002 [Google Scholar]