International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 9 (September 2025), Pages: 79-89

----------------------------------------------

Original Research Paper

The influence of environmental, social, and governance factors on firm performance: Earnings quality as a moderator

Author(s):

Affiliation(s):

Faculty of Business Administration, Rajamangala University of Technology Thanyaburi, Khlong Hok, Thailand

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-8269-7531

Corresponding author's ORCID profile: https://orcid.org/0000-0001-8269-7531

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.09.007

Abstract

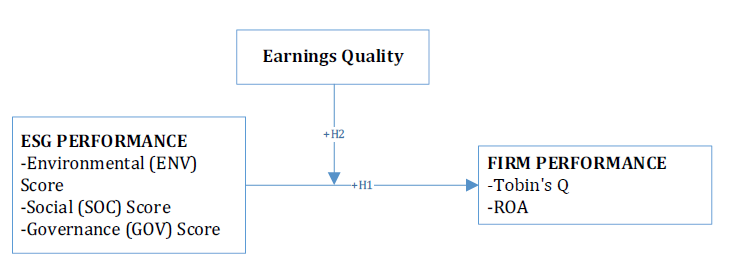

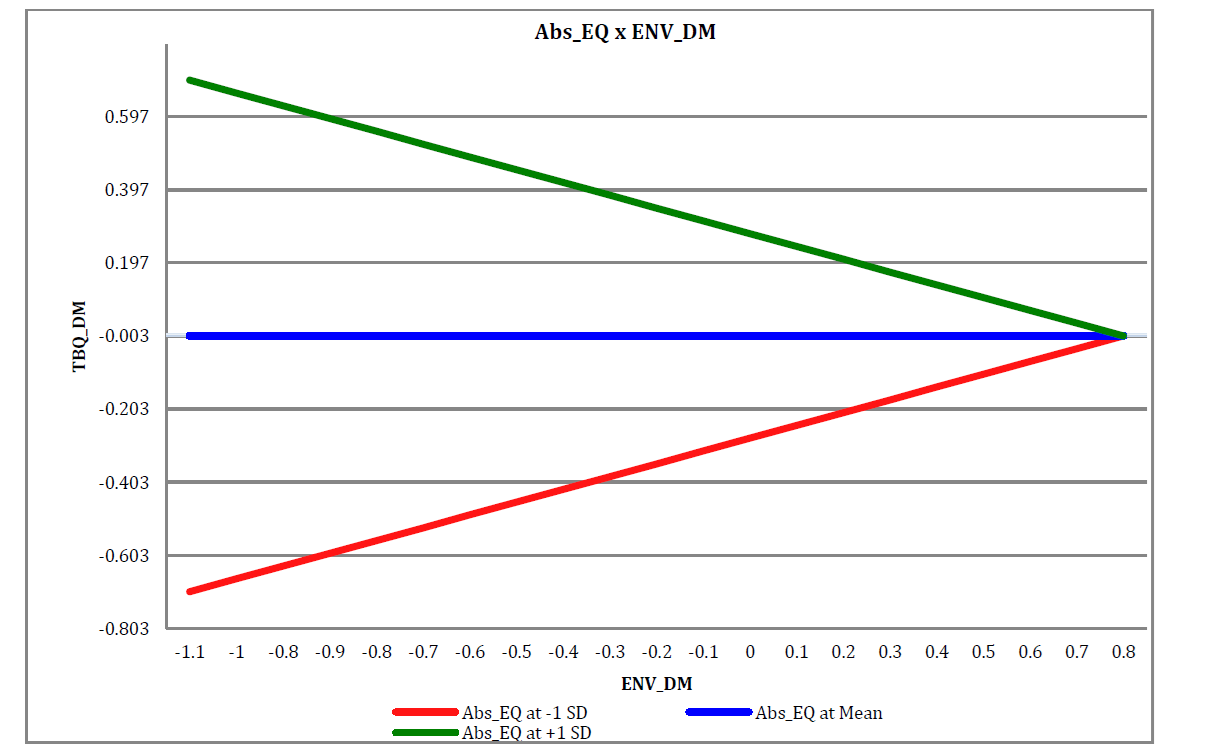

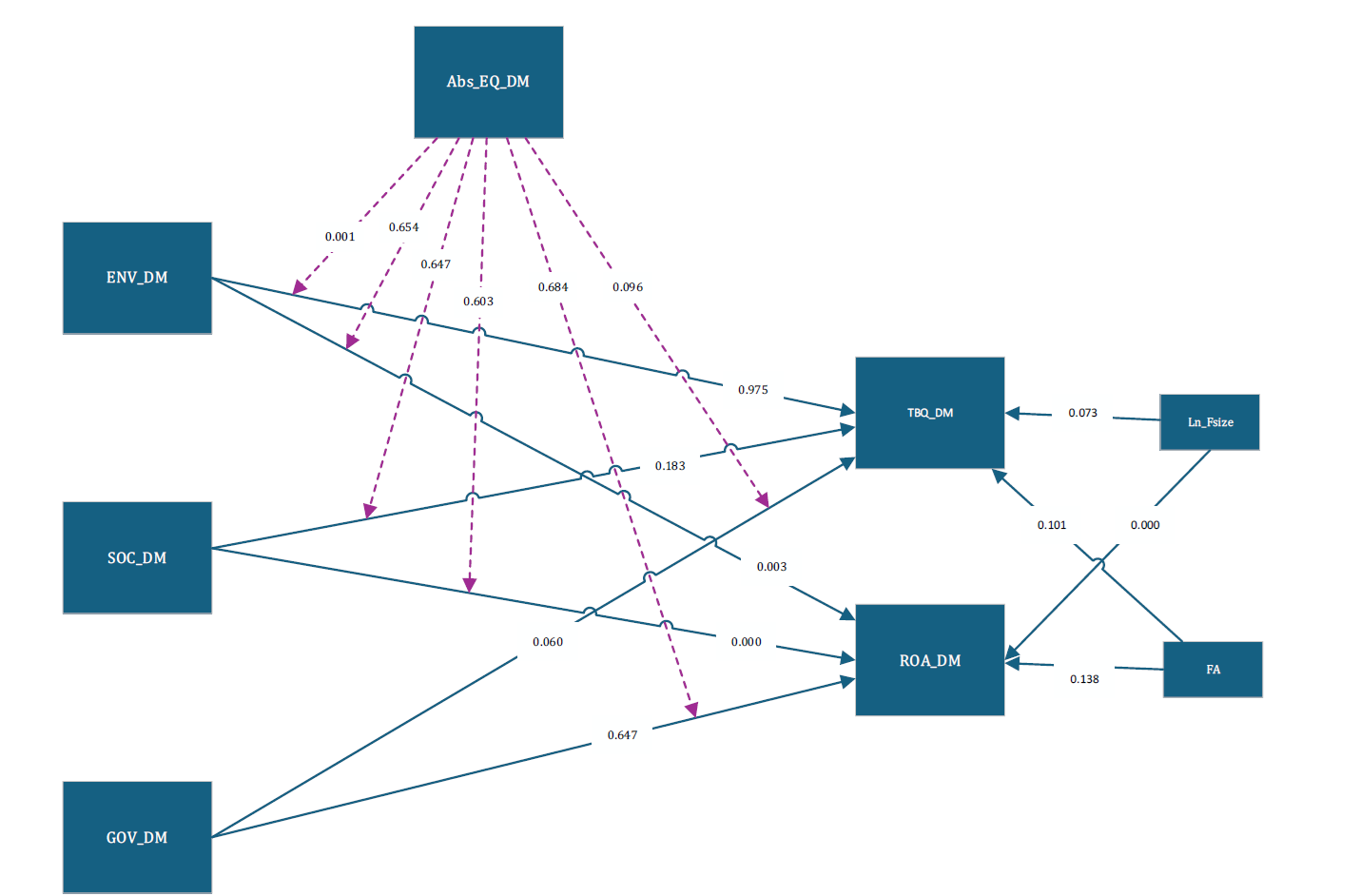

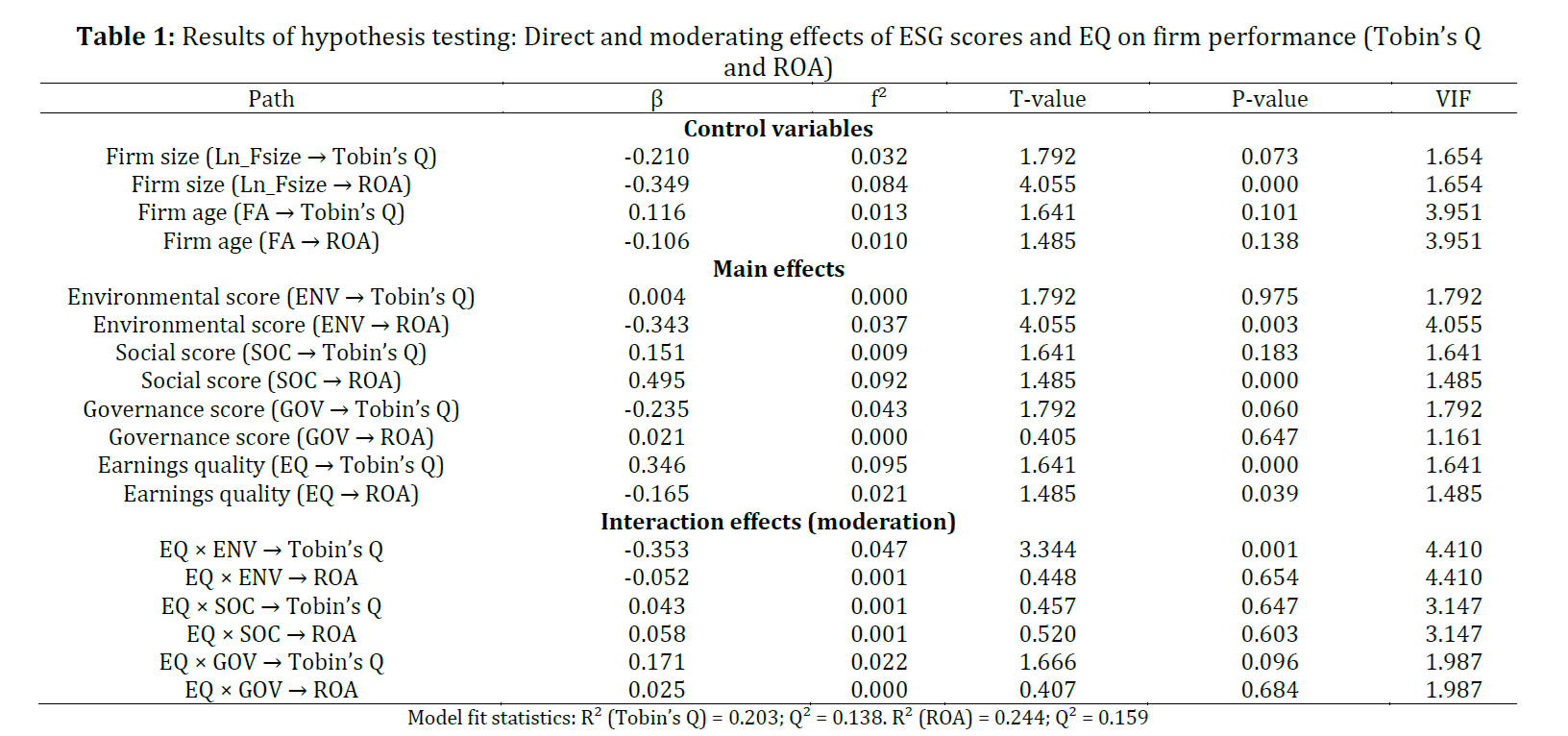

This study investigates the impact of Environmental, Social, and Governance (ESG) factors on firm performance, measured by market performance (Tobin’s Q) and financial performance, with Earnings Quality (EQ) as a moderating variable. The sample includes 208 companies listed on the Stock Exchange of Thailand that remained in the Thailand Sustainability Investment (THSI) index for at least five consecutive years (2018–2022). Partial Least Squares Structural Equation Modeling (PLS-SEM) using SmartPLS software was employed for analysis. The results show that the Social (SOC) Score positively affects Return on Assets (ROA), indicating that social activities may enhance financial performance through increased stakeholder trust. In contrast, the Environmental (ENV) Score negatively affects ROA, suggesting that environmental investments may raise costs without short-term financial returns. The Governance (GOV) Score shows no significant effect on either ROA or Tobin’s Q. EQ plays a significant moderating role by strengthening the positive effect of environmental initiatives on Tobin’s Q, particularly in firms with high EQ, which benefit from improved transparency and investor confidence. These findings support Stakeholder and Agency Theory and highlight the importance of aligning ESG practices with strong financial reporting to promote sustainability and maximize market value.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Environmental factors, Social performance, Governance impact, Earnings quality, Firm performance

Article history

Received 19 March 2025, Received in revised form 17 July 2025, Accepted 7 August 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Charoensuk P, Pholkaew C, and Dampitakse K (2025). The influence of environmental, social, and governance factors on firm performance: Earnings quality as a moderator. International Journal of Advanced and Applied Sciences, 12(9): 79-89

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

----------------------------------------------

References (29)

- Adams CA and Abhayawansa S (2022). Connecting the COVID-19 pandemic, environmental, social and governance (ESG) investing and calls for ‘harmonisation’ of sustainability reporting. Critical Perspectives on Accounting, 82: 102309. https://doi.org/10.1016/j.cpa.2021.102309 [Google Scholar] PMCid:PMC8882606

- Alareeni BA and Hamdan A (2020). ESG impact on performance of US S&P 500-listed firms. Corporate Governance: The International Journal of Business in Society, 20(7): 1409-1428. https://doi.org/10.1108/CG-06-2020-0258 [Google Scholar]

- Al-Matari EM, Al-Swidi AK, and Fadzil FH (2014). The measurements of firm performance's dimensions. Asian Journal of Finance & Accounting, 6(1): 24-49. https://doi.org/10.5296/ajfa.v6i1.4761 [Google Scholar]

- Almubarak WI, Chebbi K, and Ammer MA (2023). Unveiling the connection among ESG, earnings management, and financial distress: Insights from an emerging market. Sustainability, 15(16): 12348. https://doi.org/10.3390/su151612348 [Google Scholar]

- Aqabna SM, Aga M, and Jabari HN (2023). Firm performance, corporate social responsibility and the impact of earnings management during COVID-19: Evidence from MENA region. Sustainability, 15(2): 1485. https://doi.org/10.3390/su15021485 [Google Scholar]

- Ben-Amar W, Chang M, and McIlkenny P (2017). Board gender diversity and corporate response to sustainability initiatives: Evidence from the carbon disclosure project. Journal of Business Ethics, 142: 369-383. https://doi.org/10.1007/s10551-015-2759-1 [Google Scholar]

- Biddle GC, Bowen RM, and Wallace JS (1997). Does EVA® beat earnings? Evidence on associations with stock returns and firm values. Journal of Accounting and Economics, 24(3): 301-336. https://doi.org/10.1016/S0165-4101(98)00010-X [Google Scholar]

- Braun B (2021). Asset manager capitalism as a corporate governance regime. In: Hacker JS, Hertel-Fernandez A, Pierson P, and Thelen K (Eds.), The American political economy: 270–294. 1st Edition, Cambridge University Press, Cambridge, UK. https://doi.org/10.1017/9781009029841.010 [Google Scholar]

- Budsaratragoon P and Jitmaneeroj B (2021). Corporate sustainability and stock value in Asian–pacific emerging markets: Synergies or tradeoffs among ESG factors? Sustainability, 13(11): 6458. https://doi.org/10.3390/su13116458 [Google Scholar]

- Byrne BM (2013). Structural equation modeling with Mplus: Basic concepts, applications, and programming. 1st Edition, Routledge, New York, USA. https://doi.org/10.4324/9780203807644 [Google Scholar]

- Carroll AB (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4): 39-48. https://doi.org/10.1016/0007-6813(91)90005-G [Google Scholar]

- Cheng B, Ioannou I, and Serafeim G (2014). Corporate social responsibility and access to finance. Strategic Management Journal, 35: 1-23. https://doi.org/10.1002/smj.2131 [Google Scholar]

- Dechow PM, Sloan RG, and Sweeney AP (1995). Detecting earnings management. Accounting Review, 70(2): 193-225. [Google Scholar]

- Drempetic S, Klein C, and Zwergel B (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 167(2): 333-360. https://doi.org/10.1007/s10551-019-04164-1 [Google Scholar]

- Fatemi A, Fooladi I, and Tehranian H (2015). Valuation effects of corporate social responsibility. Journal of Banking & Finance, 59: 182-192. https://doi.org/10.1016/j.jbankfin.2015.04.028 [Google Scholar]

- Islam R, Haque Z, and Moutushi RH (2022). Earnings quality and financial flexibility: A moderating role of corporate governance. Cogent Business and Management, 9(1): 2097620. https://doi.org/10.1080/23311975.2022.2097620 [Google Scholar]

- Jensen MC and Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [Google Scholar]

- Jones JJ (1991). Earnings management during import relief investigations. Journal of Accounting Research, 29(2): 193-228. https://doi.org/10.2307/2491047 [Google Scholar]

- Kolsi MC, Al-Hiyari A, and Hussainey K (2023). Does environmental, social, and governance performance mitigate earnings management practices? Evidence from US commercial banks. Environmental Science and Pollution Research, 30: 20386-20401. https://doi.org/10.1007/s11356-022-23616-2 [Google Scholar] PMid:36255584 PMCid:PMC9579568

- Li X and Xu L (2021). Human development associated with environmental quality in China. PLOS ONE, 16(2): e0246677. https://doi.org/10.1371/journal.pone.0246677 [Google Scholar] PMid:33571261 PMCid:PMC7877628

- Lin Y, Lu Z, and Wang Y (2023). The impact of environmental, social, and governance (ESG) practices on investment efficiency in China: Does digital transformation matter? Research in International Business and Finance, 66: 102050. https://doi.org/10.1016/j.ribaf.2023.102050 [Google Scholar]

- Nguyen DT, Hoang TG, and Tran HG (2022). Help or hurt? The impact of ESG on firm performance in S&P 500 non-financial firms. Australasian Accounting, Business and Finance Journal, 16(2): 91-102. https://doi.org/10.14453/aabfj.v16i2.7 [Google Scholar]

- Qureshi MA, Kirkerud S, Theresa K, and Ahsan T (2020). The impact of sustainability (environmental, social, and governance) disclosure and board diversity on firm value: The moderating role of industry sensitivity. Business Strategy and the Environment, 29: 1199-1214. https://doi.org/10.1002/bse.2427 [Google Scholar]

- Richardson BJ (2009). Keeping ethical investment ethical: Regulatory issues for investing for sustainability. Journal of Business Ethics, 87: 555-572. https://doi.org/10.1007/s10551-008-9958-y [Google Scholar]

- Richardson BJ (2013). Socially responsible investing for sustainability: Overcoming its incomplete and conflicting rationales. Transnational Environmental Law, 2(2): 311-338. https://doi.org/10.1017/S2047102513000150 [Google Scholar]

- Sherif SU, Asokan P, Sasikumar P, Mathiyazhagan K, and Jerald J (2022). An integrated decision making approach for the selection of battery recycling plant location under sustainable environment. Journal of Cleaner Production, 330: 129784. https://doi.org/10.1016/j.jclepro.2021.129784 [Google Scholar]

- Tobin J (1969). A general equilibrium approach to monetary theory. Journal of Money, Credit and Banking, 1(1): 15-29. https://doi.org/10.2307/1991374 [Google Scholar]

- Tohang V, Hutagaol-Martowidjojo Y, and Pirzada K (2024). The link between ESG performance and earnings quality. Australasian Accounting, Business and Finance Journal, 18(1): 187-204. https://doi.org/10.14453/aabfj.v18i1.12 [Google Scholar]

- Wong WC, Batten JA, Mohamed-Arshad SB, Nordin S, and Adzis AA (2021). Does ESG certification add firm value? Finance Research Letters, 39: 101593. https://doi.org/10.1016/j.frl.2020.101593 [Google Scholar]