International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 8 (August 2025), Pages: 246-254

----------------------------------------------

Original Research Paper

The moderating role of internationalization in the relationship between family ownership and earnings quality: Empirical evidence from Thailand

Author(s):

Affiliation(s):

1Faculty of Business Administration, Rajamangala University of Technology Thanyaburi, Pathum Thani, Thailand

2School of Educational Studies, Sukhothai Thammathirat Open University, Nonthaburi, Thailand

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-3662-9831

Corresponding author's ORCID profile: https://orcid.org/0000-0003-3662-9831

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.08.023

Abstract

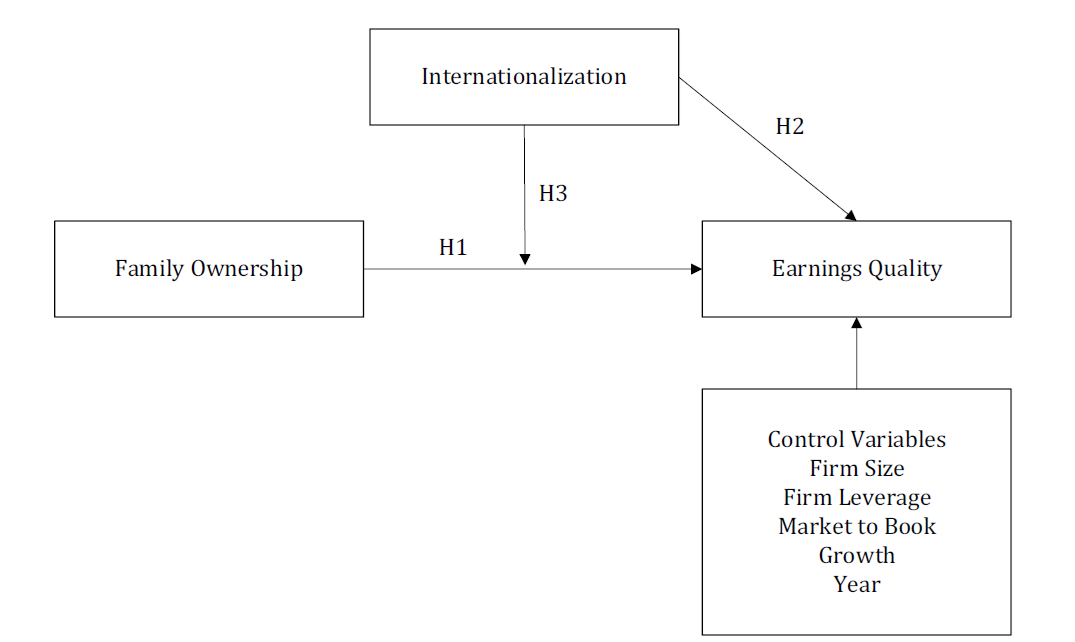

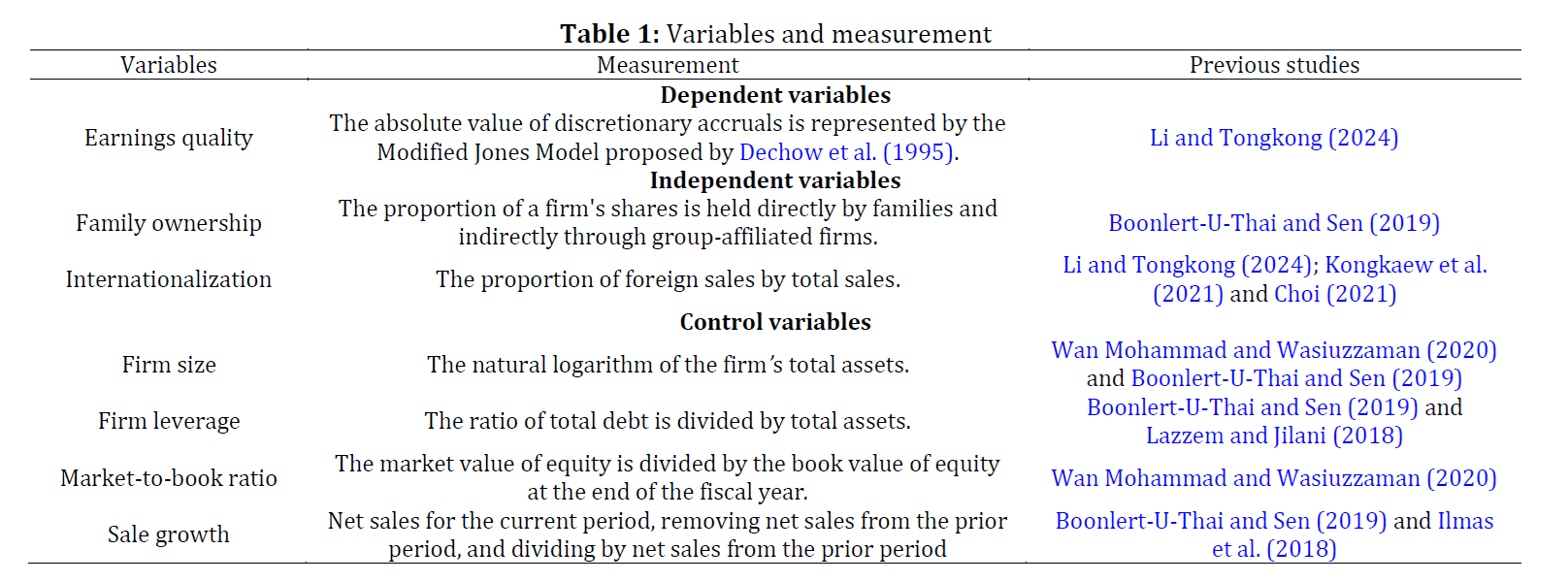

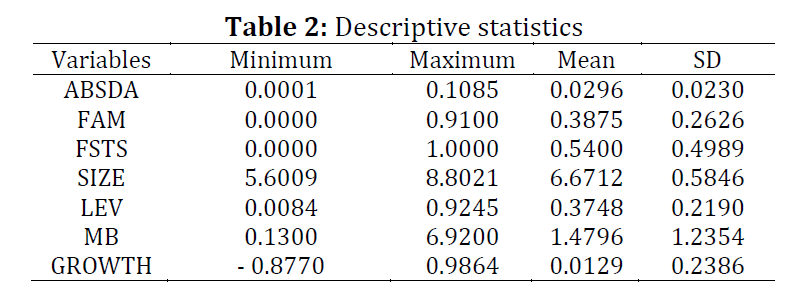

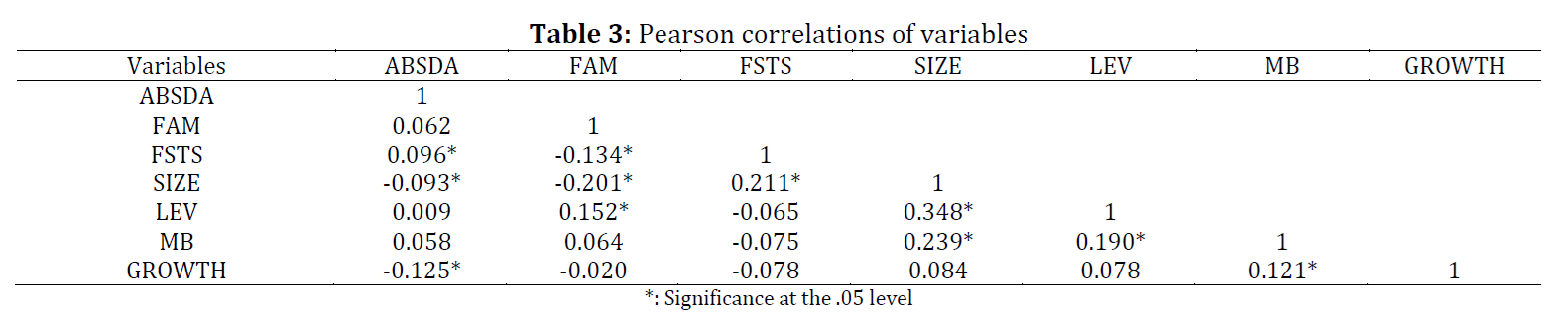

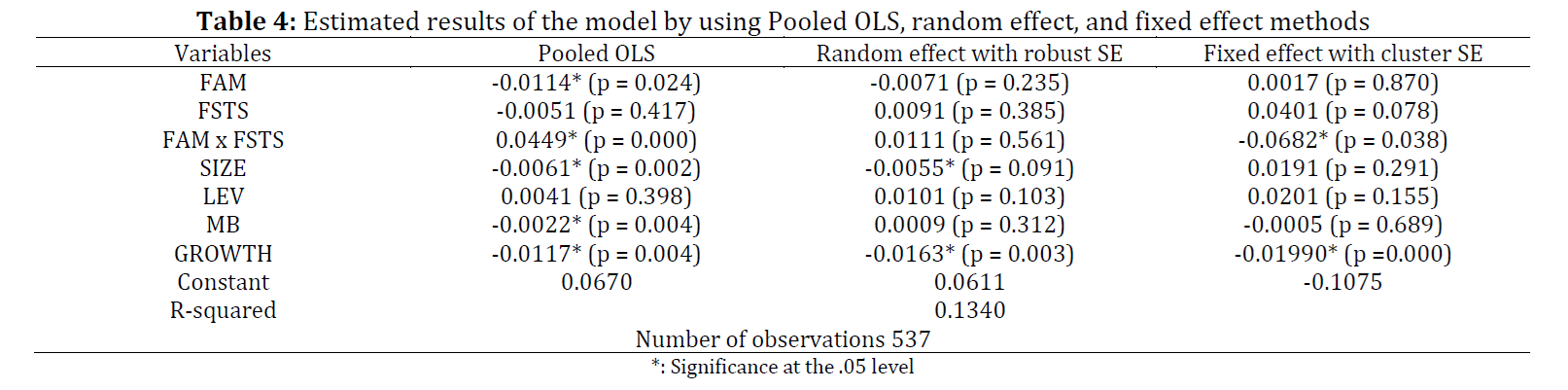

This study investigates how internationalization influences the relationship between family ownership and earnings quality. The analysis is based on 537 firm-year observations from 179 companies listed in Thailand, covering the Agricultural and Food, Consumer Products, Industrials, and Technology sectors during 2017–2019. The study employs firm-fixed-effects panel regression models with cluster-robust standard errors. Earnings quality is measured by the absolute value of discretionary accruals, while internationalization is captured by the foreign-sales-to-total-sales ratio (FSTS). The main findings indicate that family ownership alone does not have a significant impact on earnings quality. However, a higher level of foreign sales is weakly associated with increased abnormal accruals. Importantly, the results show that when foreign sales exceed about 25% of total revenue, family ownership is linked to lower discretionary accruals, suggesting improved earnings quality. Additionally, the advantages of strong governance practices appear to grow as foreign sales increase. This research adds to the literature on corporate governance and international business by showing that the influence of family ownership on financial reporting depends on the firm's international exposure. In practice, investors may perceive internationally active family firms as having lower reporting risk, while regulators may need to focus more on domestic family-owned firms.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Family ownership, Earnings quality, Foreign sales, Discretionary accruals, Corporate governance

Article history

Received 7 March 2025, Received in revised form 1 July 2025, Accepted 2 August 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Moonmuang K, Dampitakse K, and Ngudgrato S (2025). The moderating role of internationalization in the relationship between family ownership and earnings quality: Empirical evidence from Thailand. International Journal of Advanced and Applied Sciences, 12(8): 246-254

Figures

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (31)

- Anderson RC and Reeb DM (2003). Founding-family ownership, corporate diversification, and firm leverage. The Journal of Law and Economics, 46(2): 653–684. https://doi.org/10.1086/377115 [Google Scholar]

- Boonlert-U-Thai K and Sen PK (2019). Family ownership and earnings quality of Thai firms. Asian Review of Accounting, 27(4): 629–649. https://doi.org/10.1108/ARA-03-2018-0085 [Google Scholar]

- Breusch TS and Pagan AR (1980). The Lagrange multiplier test and its applications to model specification in econometrics. The Review of Economic Studies, 47(1): 239–253. https://doi.org/10.2307/2297111 [Google Scholar]

- Cameron AC and Miller DL (2015). A practitioner’s guide to cluster-robust inference. Journal of Human Resources, 50(2): 317–372. https://doi.org/10.3368/jhr.50.2.317 [Google Scholar]

- Chin C-L, Chen Y-J, and Hsieh T-J (2009). International diversification, ownership structure, legal origin, and earnings management: Evidence from Taiwan. Journal of Accounting, Auditing and Finance, 24(2): 233–262. https://doi.org/10.1177/0148558X0902400205 [Google Scholar]

- Choi Y-J (2021). The effect of firm's internationalization on accounting earnings persistence. Journal of the Korea Academia-Industrial Cooperation Society, 22(1): 221–230. https://doi.org/10.5762/KAIS.2021.22.8.486 [Google Scholar]

- Claessens S, Djankov S, and Lang LHP (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58(1–2): 81–112. https://doi.org/10.1016/S0304-405X(00)00067-2 [Google Scholar]

- Dechow P, Ge W, and Schrand C (2010). Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics, 50(2–3): 344–401. https://doi.org/10.1016/j.jacceco.2010.09.001 [Google Scholar]

- Dechow PM, Sloan RG, and Sweeney AP (1995). Detecting earnings management. The Accounting Review, 70(2): 193–225. [Google Scholar]

- El Mehdi IK and Seboui S (2011). Corporate diversification and earnings management. Review of Accounting and Finance, 10(2): 164–182. https://doi.org/10.1108/14757701111129634 [Google Scholar]

- Fan JPH and Wong TJ (2002). Corporate ownership structure and the informativeness of accounting earnings in East Asia. Journal of Accounting and Economics, 33(3): 401–425. https://doi.org/10.1016/S0165-4101(02)00047-2 [Google Scholar]

- Francis J, LaFond R, Olsson PM, and Schipper K (2004). Costs of equity and earnings attributes. The Accounting Review, 79(4): 967–1010. https://doi.org/10.2308/accr.2004.79.4.967 [Google Scholar]

- Ghaleb BAA, Kamardin H, and Tabash MI (2020). Family ownership concentration and real earnings management: Empirical evidence from an emerging market. Cogent Economics and Finance, 8(1): 1751488. https://doi.org/10.1080/23322039.2020.1751488 [Google Scholar]

- Han W and Wu D (2023). Internationalization and earnings management: Evidence from China. Finance Research Letters, 53: 103589. https://doi.org/10.1016/j.frl.2022.103589 [Google Scholar]

- Hausman JA (1978). Specification tests in econometrics. Econometrica: Journal of the Econometric Society, 46(6): 1251–1271. https://doi.org/10.2307/1913827 [Google Scholar]

- Hitt MA, Tihanyi L, Miller T, and Connelly B (2006). International diversification: Antecedents, outcomes, and moderators. Journal of Management, 32(6): 831–867. https://doi.org/10.1177/0149206306293575 [Google Scholar]

- Hussain W, Khan MA, Hussain A, Waseem MA, and Ahmed M (2021). How governance and firm internationalization affect accrual quality. Estudios de Economía Aplicada, 39(3): 36. https://doi.org/10.25115/eea.v39i3.4462 [Google Scholar]

- Ilmas F, Tahir S, and Asrar-ul-Haq M (2018). Ownership structure and debt structure as determinants of discretionary accruals: An empirical study of Pakistan. Cogent Economics and Finance, 6(1): 1439254. https://doi.org/10.1080/23322039.2018.1439254 [Google Scholar]

- Kongkaew T, Tongkong S, and Ngudgratoke S (2021). Moderating effects of founders’ role on the influence of internationalization on IPO performance of listed companies in Thailand. International Journal of Financial Studies, 9(3): 37. https://doi.org/10.3390/ijfs9030037 [Google Scholar]

- Kothari SP, Leone AJ, and Wasley CE (2005). Performance matched discretionary accrual measures. Journal of Accounting and Economics, 39(1): 163–197. https://doi.org/10.1016/j.jacceco.2004.11.002 [Google Scholar]

- Lazzem S and Jilani F (2018). The impact of leverage on accrual-based earnings management: The case of listed French firms. Research in International Business and Finance, 44: 350–358. https://doi.org/10.1016/j.ribaf.2017.07.103 [Google Scholar]

- Li T and Tongkong S (2024). Internationalization of enterprises and quality of financial reports in China: Moderating roles of audit committee characteristics. Journal of Infrastructure, Policy and Development, 8(3): 3193. https://doi.org/10.24294/jipd.v8i3.3193 [Google Scholar]

- Lim CY, Thong TY, and Ding DK (2008). Firm diversification and earnings management: Evidence from seasoned equity offerings. Review of Quantitative Finance and Accounting, 30(1): 69–92. https://doi.org/10.1007/s11156-007-0043-x [Google Scholar]

- Masud MH, Anees F, and Ahmed H (2017). Impact of corporate diversification on earnings management. Journal of Indian Business Research, 9(2): 82–106. https://doi.org/10.1108/JIBR-06-2015-0070 [Google Scholar]

- Mazzioni S and Klann RC (2018). Aspects of the quality of accounting in the international context. Revista Brasileira de Gestão de Negócios, 20(1): 92–111. https://doi.org/10.7819/rbgn.v20i1.2630 [Google Scholar]

- Petersen MA (2008). Estimating standard errors in finance panel data sets: Comparing approaches. The Review of Financial Studies, 22(1): 435–480. https://doi.org/10.1093/rfs/hhn053 [Google Scholar]

- Schipper K and Vincent L (2003). Earnings quality. Accounting Horizons, 17(1): 97–110. https://doi.org/10.2308/acch.2003.17.s-1.97 [Google Scholar]

- Sullivan D (1994). Measuring the degree of internationalization of a firm. Journal of International Business Studies, 25(2): 325–342. https://doi.org/10.1057/palgrave.jibs.8490203 [Google Scholar]

- Tessema A, Kim M, and Dandu J (2018). The impact of ownership structure on earnings quality: The case of South Korea. International Journal of Disclosure and Governance, 15(2): 129–141. https://doi.org/10.1057/s41310-018-0039-x [Google Scholar]

- Wan Mohammad WM and Wasiuzzaman S (2020). Effect of audit committee independence, board ethnicity and family ownership on earnings management in Malaysia. Journal of Accounting in Emerging Economies, 10(1): 74–99. https://doi.org/10.1108/JAEE-01-2019-0001 [Google Scholar]

- Wang D (2006). Founding family ownership and earnings quality. Journal of Accounting Research, 44(3): 619–656. https://doi.org/10.1111/j.1475-679X.2006.00213.x [Google Scholar]