International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 7 (July 2025), Pages: 230-238

----------------------------------------------

Original Research Paper

Trends in Islamic insurance research: A bibliometric approach

Author(s):

Affiliation(s):

Islamic Economic Law, Universitas Muhammadiyah Surakarta, Surakarta, Indonesia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-9063-6990

Corresponding author's ORCID profile: https://orcid.org/0000-0001-9063-6990

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.07.023

Abstract

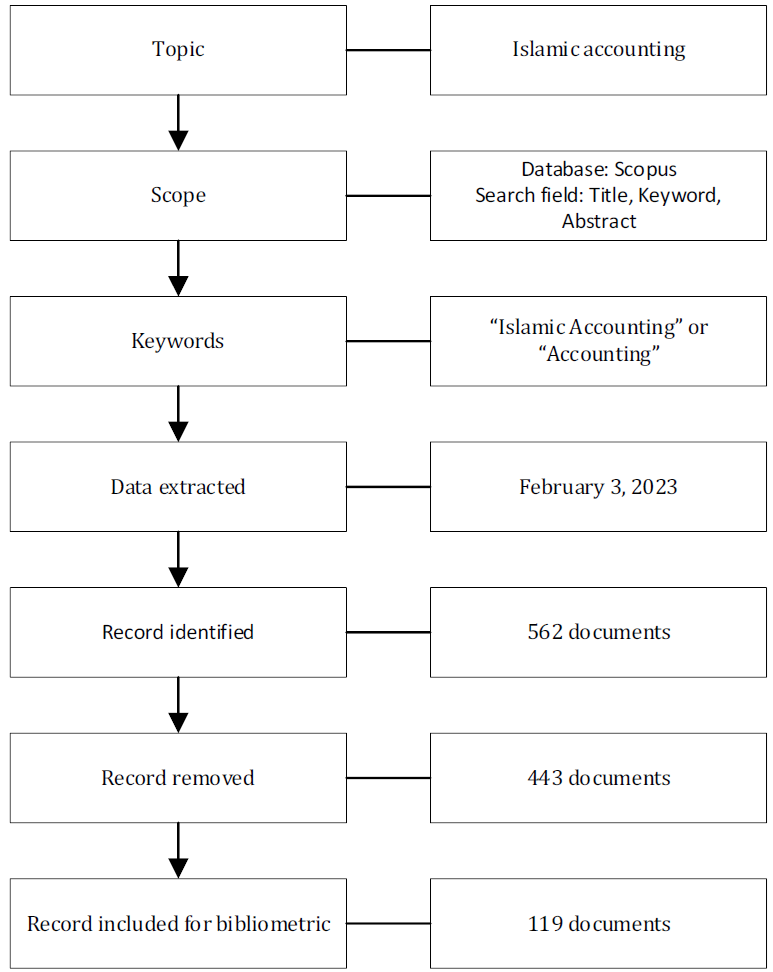

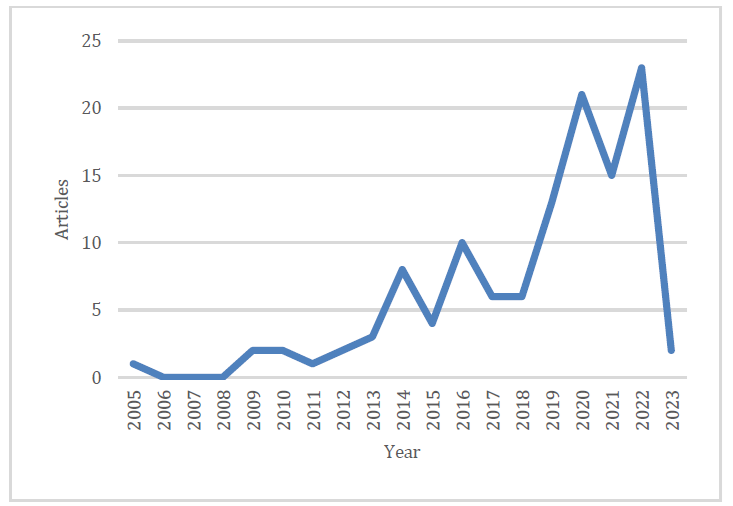

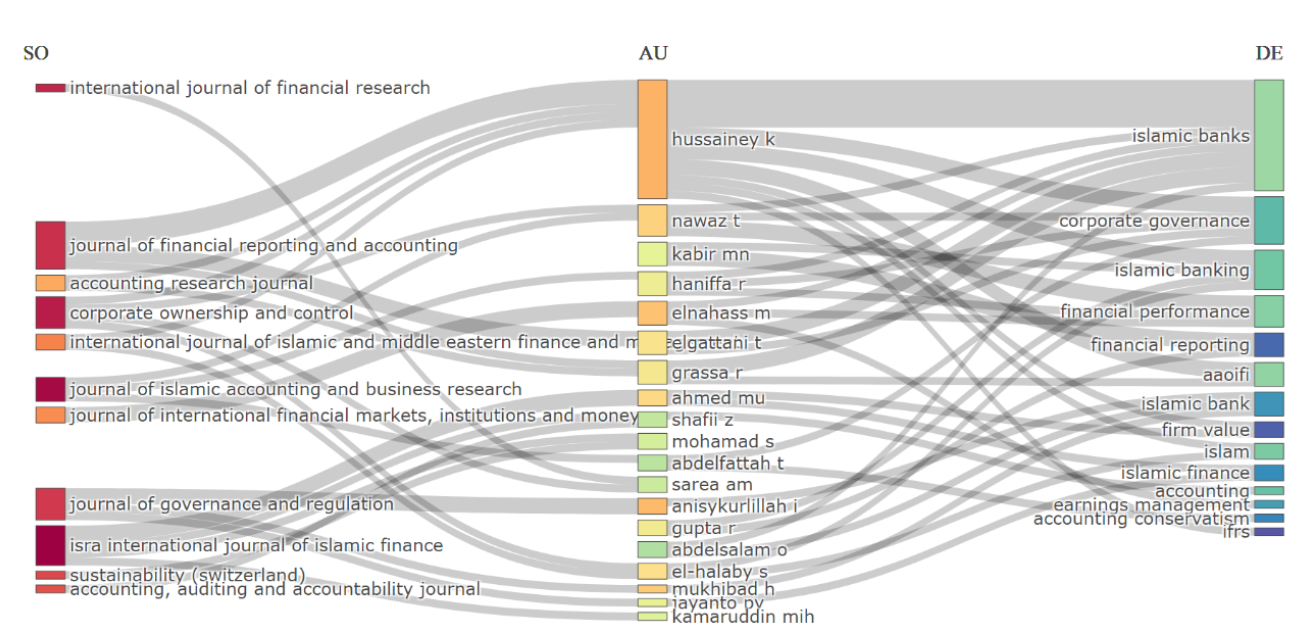

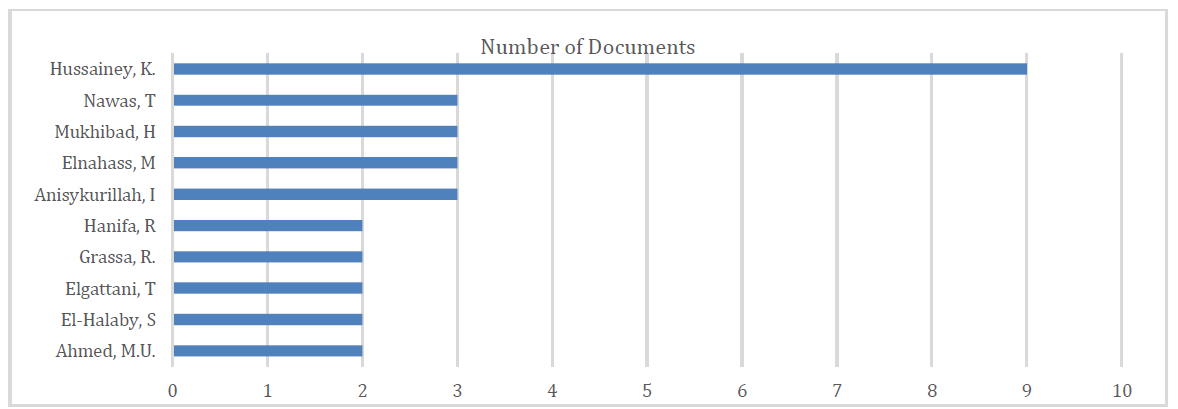

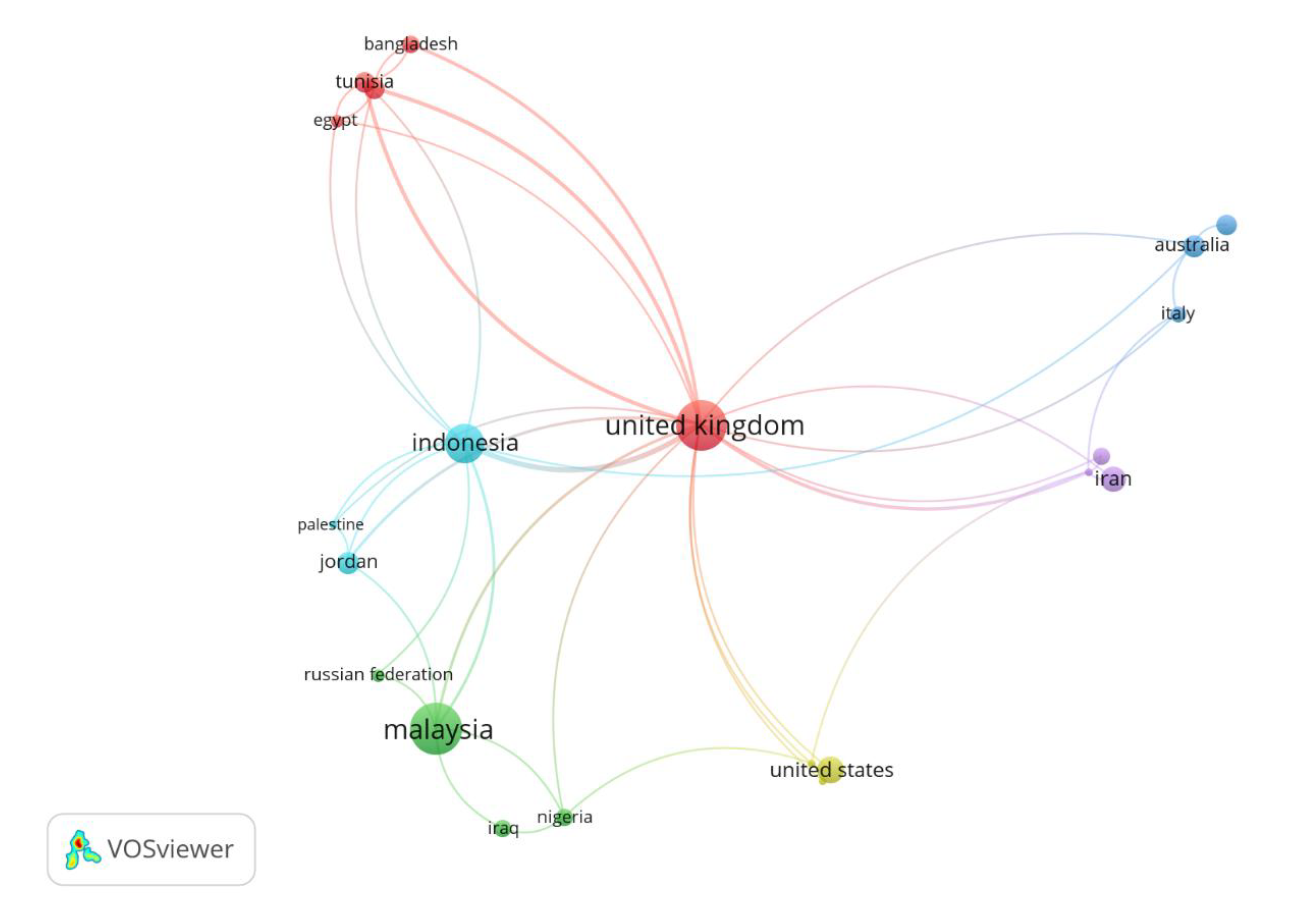

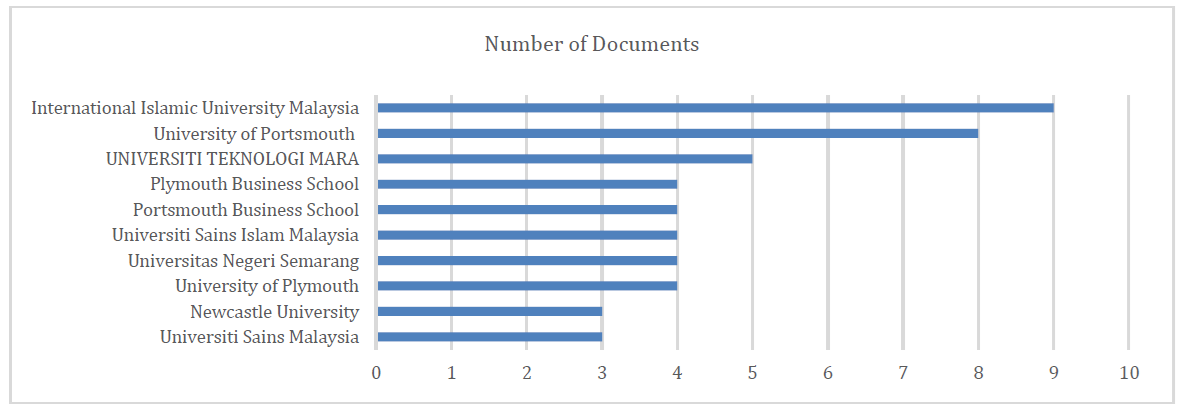

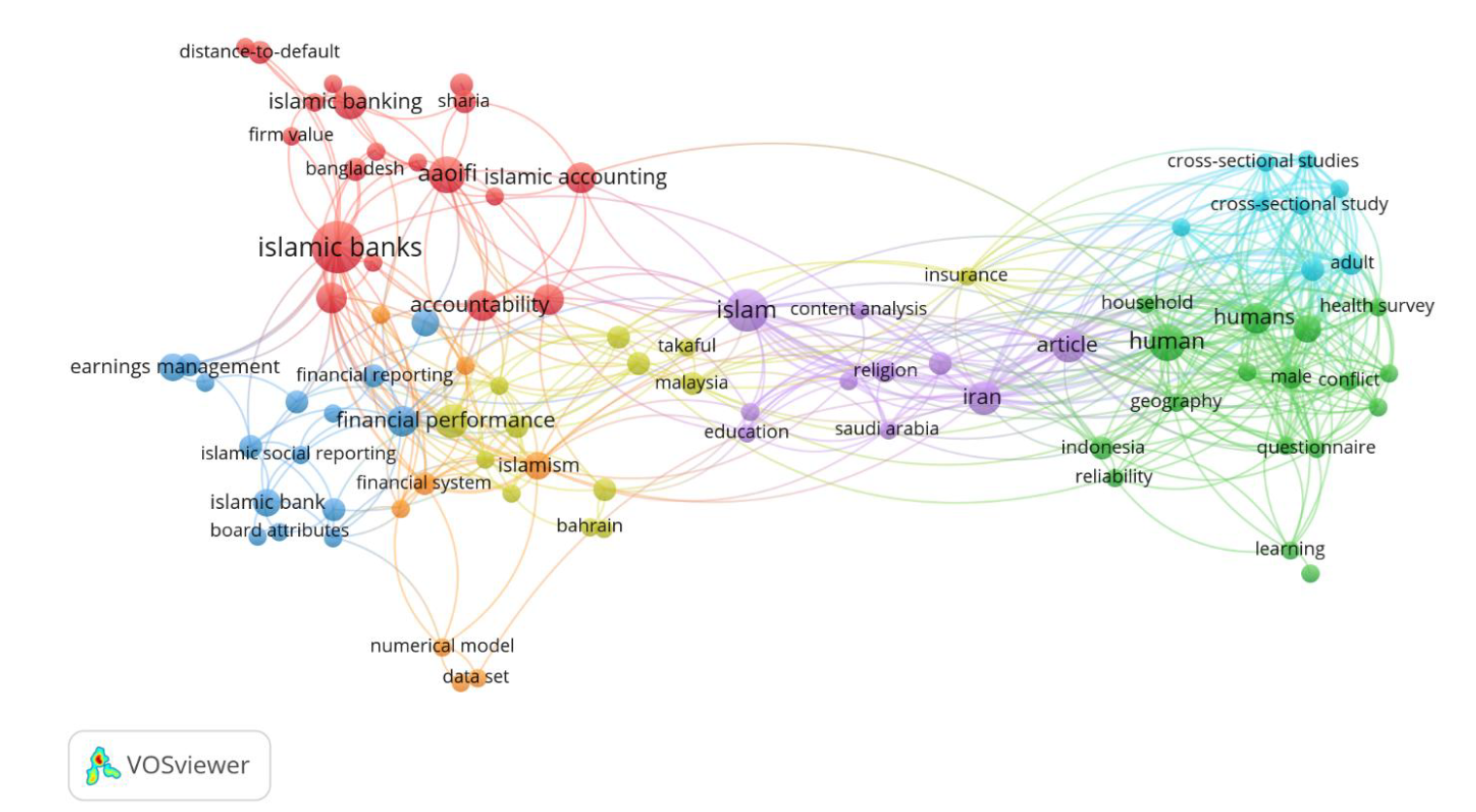

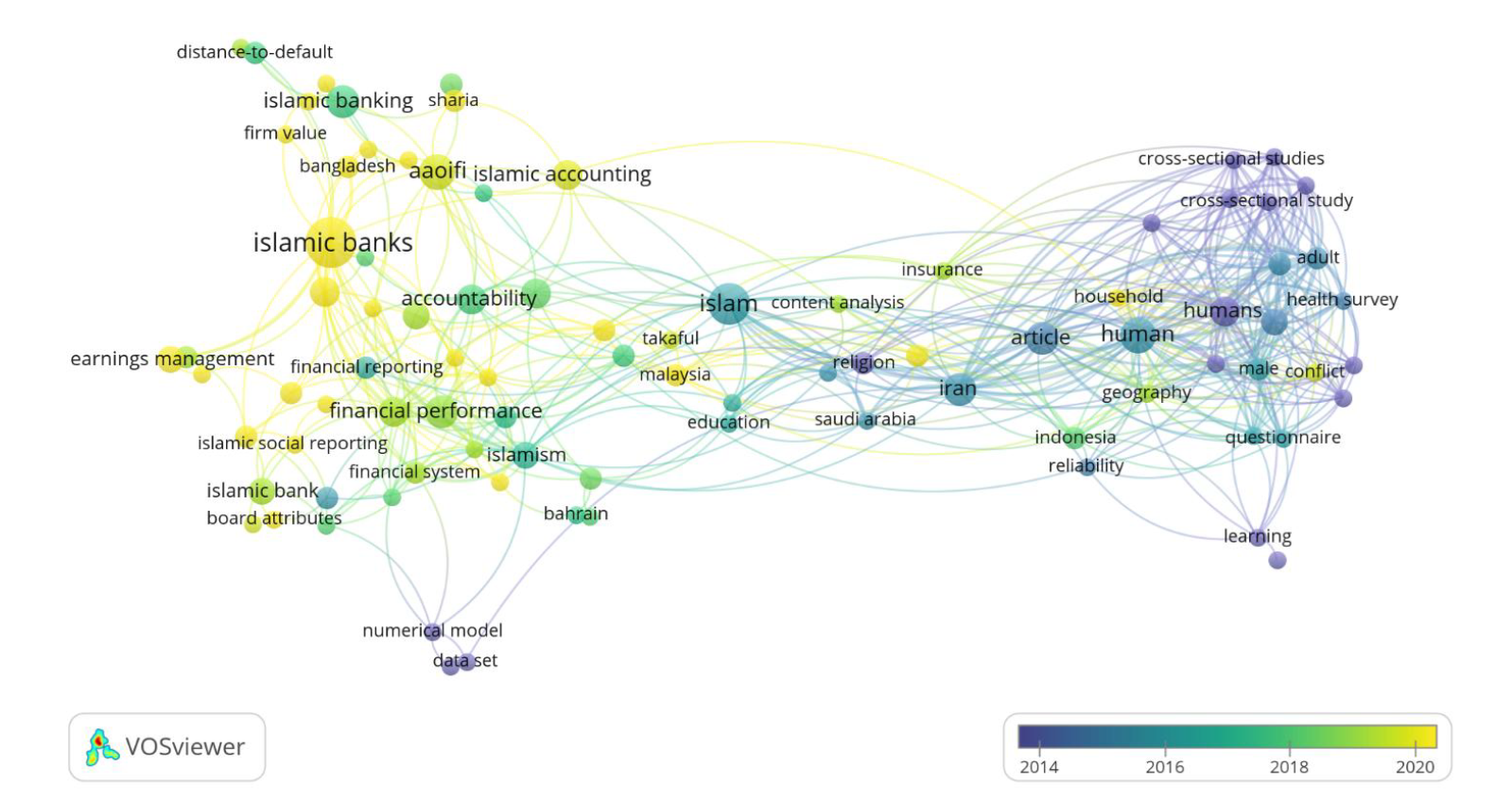

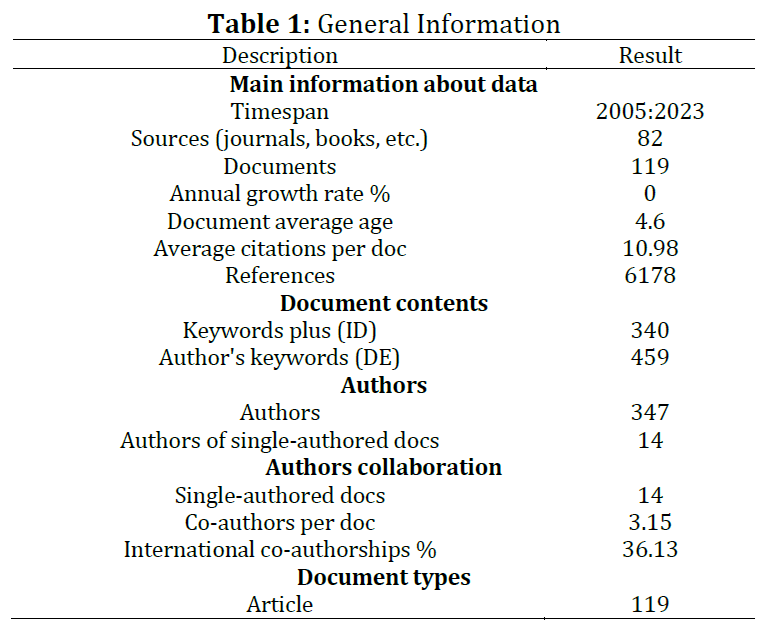

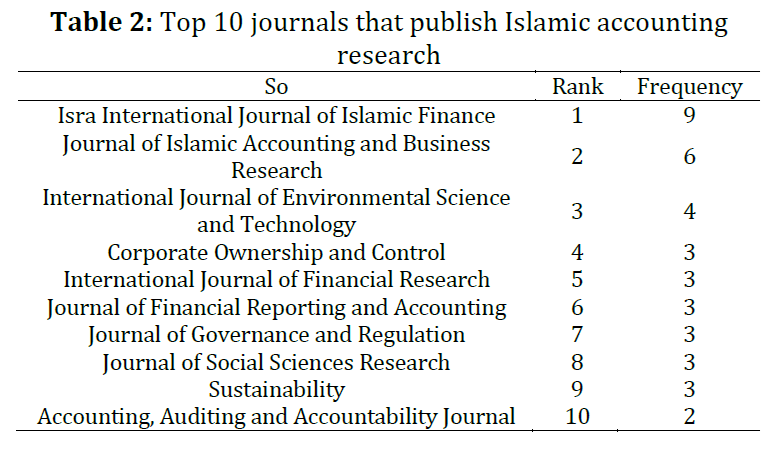

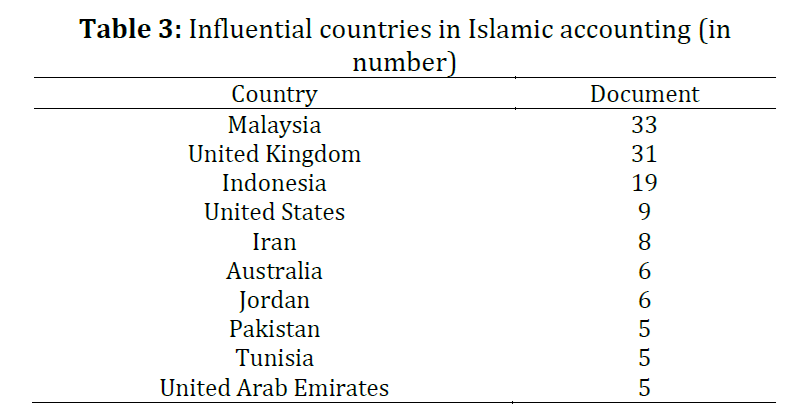

This study explores the alignment of accounting practices with Islamic values, emphasizing accountability as both a legal and spiritual obligation in Islam. Using bibliometric analysis, it examines the development of Islamic accounting research from 2005 to 2023 through Scopus-indexed journals. The analysis, conducted with R Biblioshiny and VOSviewer software, identified 119 relevant documents from an initial 562 records. The findings reveal significant growth in Islamic accounting research, with Malaysia, the United Kingdom, and Indonesia leading contributions in publications. The study highlights the increasing prominence of Islamic accounting, reflected in the expansion of empirical research, active authors, and citations. By providing a bibliometric representation of this field, the study offers valuable insights for future research directions and recruitment strategies, serving as a catalyst for further development in Islamic accounting.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Accountability in Islam, Bibliometric analysis, Scopus-indexed journals, Research development, Islamic accounting

Article history

Received 24 August 2024, Received in revised form 11 April 2025, Accepted 27 June 2025

Acknowledgment

This research was funded by the Research and Innovation Institute of Muhammadiyah University of Surakarta.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Febriandika NR and Irawan T (2025). Trends in Islamic insurance research: A bibliometric approach. International Journal of Advanced and Applied Sciences, 12(7): 230-238

Figures

Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6 Fig. 7 Fig. 8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (24)

- Abd Wahab N, Mohd Yusof R, Zainuddin Z, Shamsuddin JN, and Mohamad SF (2023). Charting future growth for Islamic finance talents in Malaysia: A bibliometric analysis on the Islamic finance domains and future research gaps. Journal of Islamic Accounting and Business Research, 14(5): 812-837. https://doi.org/10.1108/JIABR-02-2022-0045 [Google Scholar]

- Abdelsalam O, Dimitropoulos P, Elnahass M, and Leventis S (2016). Earnings management behaviors under different monitoring mechanisms: The case of Islamic and conventional banks. Journal of Economic Behavior and Organization, 132: 155–173. https://doi.org/10.1016/j.jebo.2016.04.022 [Google Scholar]

- Agbodjo S, Toumi K, and Hussainey K (2021). Accounting standards and value relevance of accounting information: A comparative analysis between Islamic, conventional and hybrid banks. Journal of Applied Accounting Research, 22(1): 168–193. https://doi.org/10.1108/JAAR-05-2020-0090 [Google Scholar]

- Amir F and Zuhroh I (2018). The Impacts of AFTA-common effective preferential tariffs on the trade diversion and trade creation of synthetic rubber and factice from oil in Indonesia. Muhammadiyah International Journal of Economics and Business, 1(1): 1-12. https://doi.org/10.23917/mijeb.v1i1.7299 [Google Scholar]

- Ardiansyah M (2022). Accounting conservatism in the perspective of positive accounting theory: A study of Islamic banking in Indonesia. Asian Economic and Financial Review, 12(6): 380-396. https://doi.org/10.55493/5002.v12i6.4500 [Google Scholar]

- Bahri NA, Triyuwono I, and Prihatiningtias YW (2021). Asset's concept based on zuhud: Reflection value of simplicity in Islam. Riset Akuntansi Dan Keuangan Indonesia, 6(2): 215-228. https://doi.org/10.23917/reaksi.v6i2.13800 [Google Scholar]

- Basri H, Nabiha AS, and Majid MSA (2016). Accounting and accountability in religious organizations: An Islamic contemporary scholars' perspective. Gadjah Mada International Journal of Business, 18(2): 207-230. https://doi.org/10.22146/gamaijb.12574 [Google Scholar]

- Ebrahim A and Abdelfattah T (2021). The substance and form of Islamic Finance instruments: An accounting perspective. Journal of Islamic Accounting and Business Research, 12(6): 872-886. https://doi.org/10.1108/JIABR-10-2019-0200 [Google Scholar]

- Febriandika NR, Kusuma D, and Yayuli Y (2023c). Zakat compliance behavior in formal zakat institutions: An integration model of religiosity, trust, credibility, and accountability. International Journal of Advanced and Applied Sciences, 10: 187-194. https://doi.org/10.21833/ijaas.2023.06.022 [Google Scholar]

- Febriandika NR, Millatina AN, Luthfiyatillah, and Herianingrum S (2020). Customer e-loyalty of Muslim millennials in Indonesia: Integrated model of trust, user experience and branding in e-commerce webstore. In the Proceedings of the 2020 11 th International Conference on E-Education, E-Business, E-Management, and E-learning, ACM, Osaka, Japan: 369-376. https://doi.org/10.1145/3377571.3377638 [Google Scholar]

- Febriandika NR, Wati RM, and Hasanah M (2023a). Russia's invasion of Ukraine: The reaction of Islamic stocks in the energy sector of Indonesia. Investment Management and Financial Innovations, 20(1): 218-227. https://doi.org/10.21511/imfi.20(1).2023.19 [Google Scholar]

- Grassa R, Moumen N, and Hussainey K (2021). Do ownership structures affect risk disclosure in Islamic banks? International evidence. Journal of Financial Reporting and Accounting, 19(3): 369-391. https://doi.org/10.1108/JFRA-02-2020-0036 [Google Scholar]

- Hanif M and Iqbal A (2014). An evaluation of takaful insurance: Case of Pakistan. Journal of Islamic Economics, Banking and Finance, 13(1): 122-146. https://doi.org/10.12816/0051159 [Google Scholar]

- Hulme EW (1923). Statistical bibliography in relation to the growth of modern civilization: Two lectures delivered in the University of Cambridge in May 1922. Nature, 112: 585–586. https://doi.org/10.1038/112585a0 [Google Scholar]

- Mulyasari W and Mayangsari S (2020). Environmental management accounting, Islamic social reporting, and corporate governance mechanism on Sharia-approved companies in Indonesia. International Journal of Financial Research, 11(1): 284-292. https://doi.org/10.5430/ijfr.v11n1p284 [Google Scholar]

- Nahar HS and Yaacob H (2023). A tribute to the Journal of Islamic Accounting and Business Research: (More than) a decade of serving the Ummah. Journal of Islamic Accounting and Business Research, 14(2): 209–229. https://doi.org/10.1108/JIABR-12-2021-0312 [Google Scholar]

- Nawaz T, Haniffa R, and Hudaib M (2021). On intellectual capital efficiency and Shariah governance in Islamic banking business model. International Journal of Finance and Economics, 26(3): 3770–3787. https://doi.org/10.1002/ijfe.1986 [Google Scholar]

- Pritchard A (1969). Statistical bibliography or bibliometrics. Journal of Documentation, 25: 348-349. https://doi.org/10.1108/eb026482 [Google Scholar]

- Purbasari H, Bawono ADB, Ramadhanti M, and Kurniawati L (2020). Earnings and cash flow information on its value relevance by the book value. Riset Akuntansi dan Keuangan Indonesia, 5(1): 46-53. https://doi.org/10.23917/reaksi.v5i1.10679 [Google Scholar]

- Sahyouni A and Wang M (2019). Liquidity creation and bank performance: Evidence from MENA. ISRA International Journal of Islamic Finance, 11(1): 27–45. https://doi.org/10.1108/IJIF-01-2018-0009 [Google Scholar]

- Umar UH and Kurawa JM (2019). Business succession from an Islamic accounting perspective. ISRA International Journal of Islamic Finance, 11(2): 267–281. https://doi.org/10.1108/IJIF-06-2018-0059 [Google Scholar]

- Voronova EY and Umarov HS (2021). Islamic (partner) accounting and its comparison with international financial accounting standards (IFRS). Universal Journal of Accounting and Finance, 9(2): 267–274. https://doi.org/10.13189/ujaf.2021.090217 [Google Scholar]

- Wahyuni S, Pujiharto P, and Hartikasari AI (2020). Sharia Maqashid index and its effect on the value of the firm of Islamic commercial bank in Indonesia. Riset Akuntansi Dan Keuangan Indonesia, 5(1): 36-45. https://doi.org/10.23917/reaksi.v5i1.9493 [Google Scholar]

- You J, Chen X, Chen L, Chen J, Chai B, Kang A, Lei X, and Wang S (2022). A systematic bibliometric review of low impact development research articles. Water, 14(17): 2675. https://doi.org/10.3390/w14172675 [Google Scholar]