International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 7 (July 2025), Pages: 134-143

----------------------------------------------

Original Research Paper

Modeling stock price trends and volatility in emerging markets using ARIMA and GARCH approaches

Author(s):

Affiliation(s):

1Department of Mathematics and Statistics, University of Embu, Embu, Kenya

2Department of Computing and Information Technology, University of Embu, Embu, Kenya

3Department of Physical Sciences, University of Embu, Embu, Kenya

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-7990-0946

Corresponding author's ORCID profile: https://orcid.org/0000-0002-7990-0946

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.07.013

Abstract

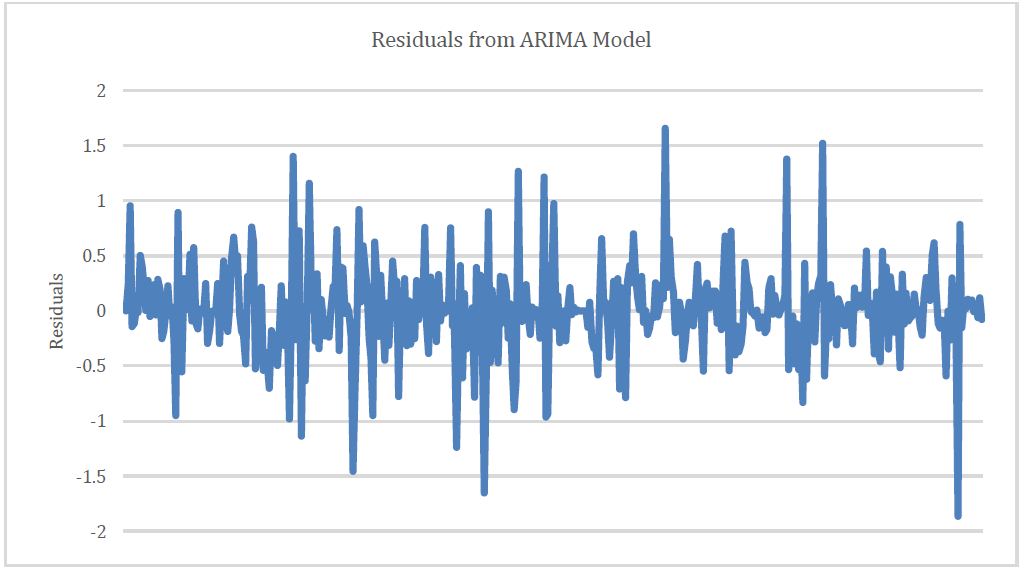

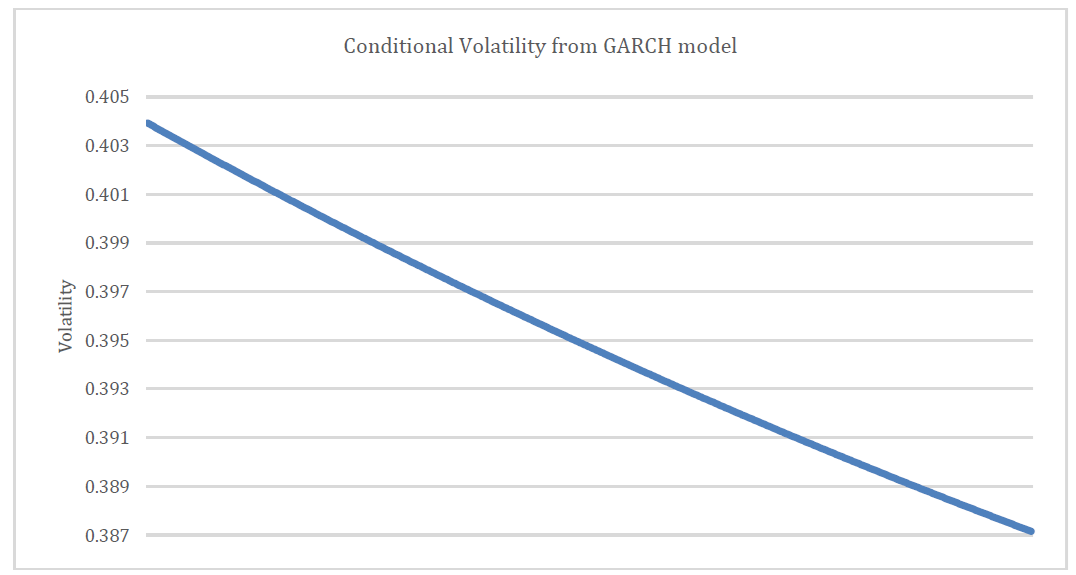

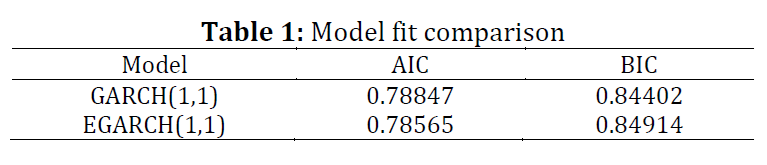

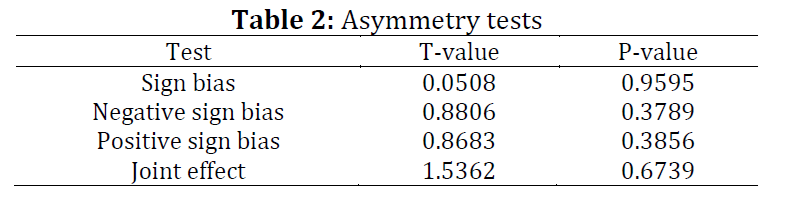

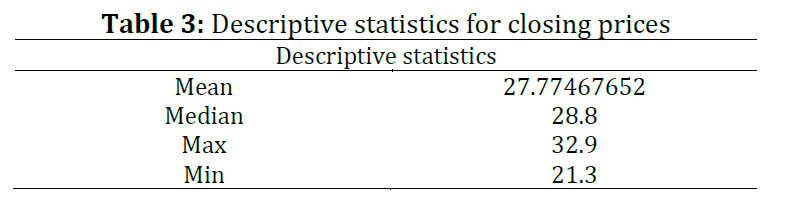

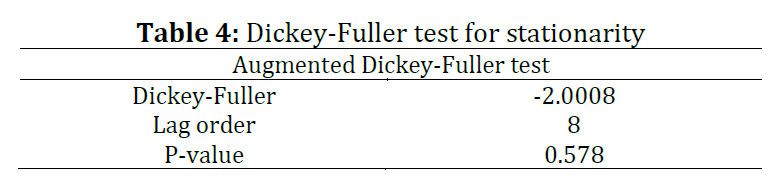

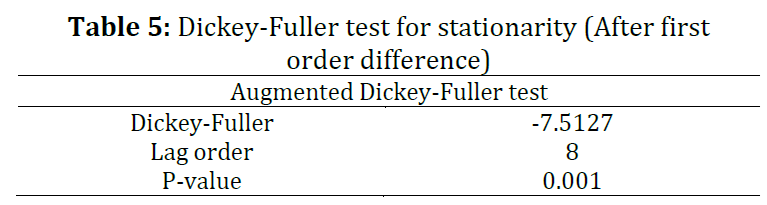

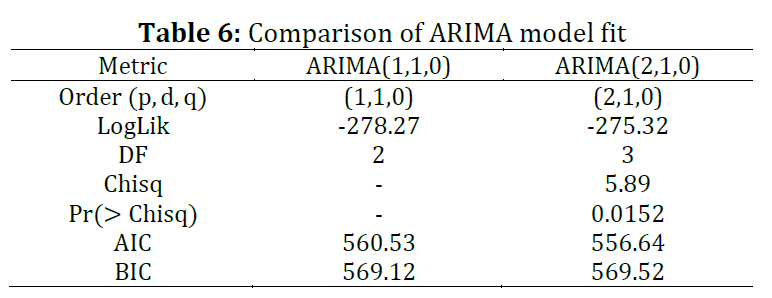

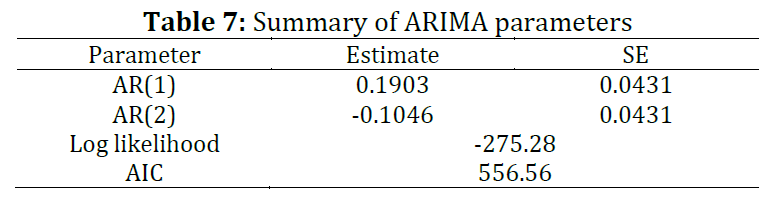

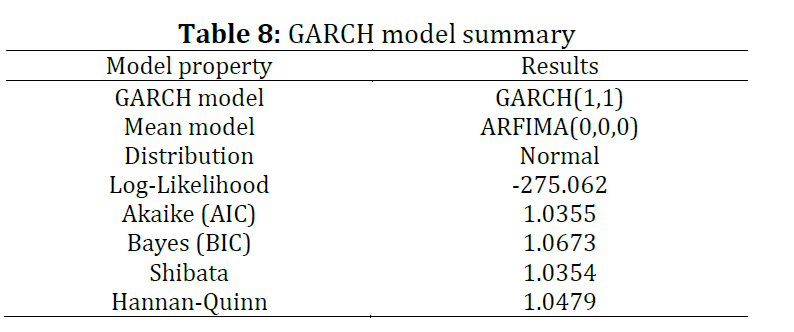

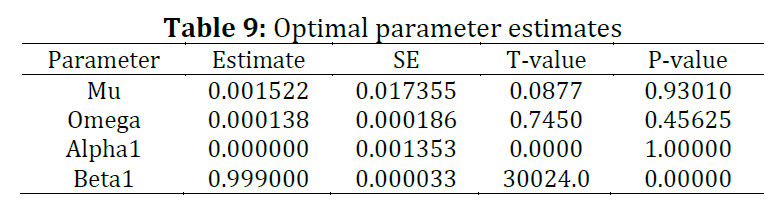

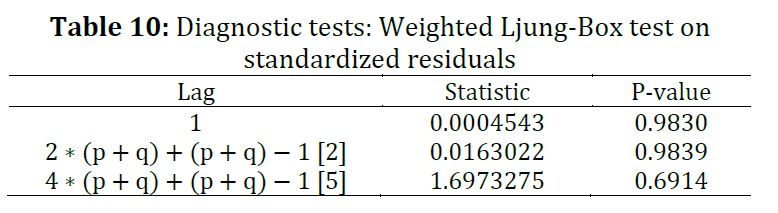

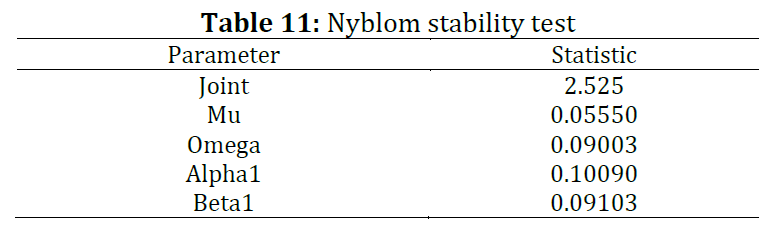

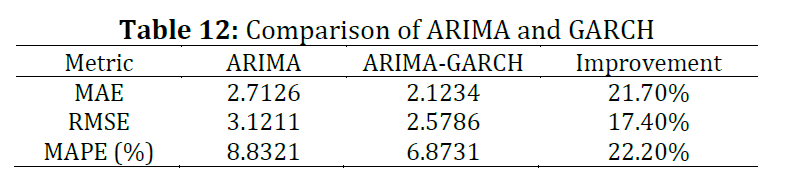

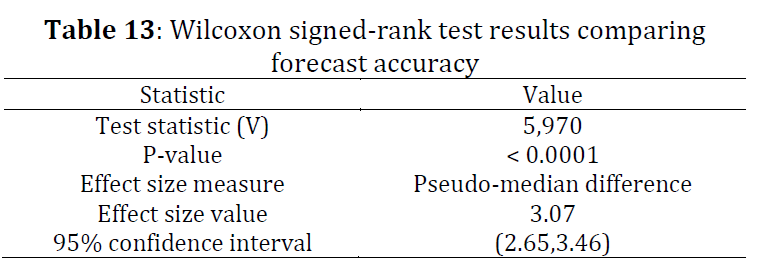

Stock price prediction and volatility modeling are important for making financial decisions, especially in emerging markets like the Nairobi Securities Exchange (NSE). This study examines how well the Autoregressive Integrated Moving Average (ARIMA) and Generalized Autoregressive Conditional Heteroskedasticity (GARCH) models perform in forecasting stock prices and modeling volatility. The ARIMA (2,1,0) model was selected as the best fit using the Akaike Information Criterion (AIC), showing strong performance in capturing long-term price trends. However, an analysis of the residuals showed signs of volatility clustering, meaning ARIMA alone could not capture short-term fluctuations. To solve this, the study added a GARCH (1,1) model, which effectively captured changing volatility and improved prediction accuracy. The combined ARIMA-GARCH model reduced the Root Mean Squared Error (RMSE) from 3.1211 to 2.5786, demonstrating the value of including volatility modeling in financial time series. The results highlight the need for strong statistical models in emerging markets, where stock prices are often affected by external shocks and market inefficiencies. This research offers useful insights for investors, policymakers, and financial analysts by supporting better risk management and more accurate forecasting. Future studies could expand the model to include more stocks, macroeconomic data, and machine learning techniques to further improve results.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Stock prediction, Volatility modeling, ARIMA model, GARCH model, Emerging markets

Article history

Received 21 February 2025, Received in revised form 18 May 2025, Accepted 17 June 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Macharia K, Atitwa E, Mugo D, and Kawira M (2025). Modeling stock price trends and volatility in emerging markets using ARIMA and GARCH approaches. International Journal of Advanced and Applied Sciences, 12(7): 134-143

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9 Table 10 Table 11 Table 12 Table 13

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (28)

- Ali M, Khan DM, Aamir M, Ali A, and Ahmad Z (2021). Predicting the direction movement of financial time series using artificial neural network and support vector machine. Complexity, 2021: 2906463. https://doi.org/10.1155/2021/2906463 [Google Scholar]

- Box G and Jenkins GM (1976). Time series analysis: Forecasting and control. Holden-Day, New York, USA. [Google Scholar]

- Chea A (2021). Doing business in emerging market economies: Challenges and success strategies for Western multinational corporations. International Business Research, 14(9): 82-93. https://doi.org/10.5539/ibr.v14n9p82 [Google Scholar]

- Chhajer P, Shah M, and Kshirsagar A (2022). The applications of artificial neural networks, support vector machines, and long–short term memory for stock market prediction. Decision Analytics Journal, 2: 100015. https://doi.org/10.1016/j.dajour.2021.100015 [Google Scholar]

- Chrysostome E (2022). Scrutinizing emerging markets and exploring the impact of paradigms on knowledge production in international business. Journal of Comparative International Management, 25(1): 1-8. https://doi.org/10.55482/jcim.2022.32936 [Google Scholar]

- Dar AA, Jain A, Malhotra M, Farooqi AR, Albalawi O, Khan MS, and Hiba (2024). Time series analysis with ARIMA for historical stock data and future projections. Soft Computing, 28: 12531–12542. https://doi.org/10.1007/s00500-024-10309-w [Google Scholar]

- Emmanuel I and Tolulope OO (2024). Stock price prediction: A systematic review. In the International Conference on Science, Engineering and Business for Driving Sustainable Development Goals, IEEE, Omu-Aran, Nigeria: 1-5. https://doi.org/10.1109/SEB4SDG60871.2024.10629903 [Google Scholar] PMCid:PMC11046499

- Engle RF (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4): 987-1007. https://doi.org/10.2307/1912773 [Google Scholar]

- Gite S, Khatavkar H, Kotecha K, Srivastava S, Maheshwari P, and Pandey N (2021). Explainable stock prices prediction from financial news articles using sentiment analysis. PeerJ Computer Science, 7: e340. https://doi.org/10.7717/peerj-cs.340 [Google Scholar] PMid:33816991 PMCid:PMC7924447

- Kumar D, Sarangi PK, and Verma R (2022). A systematic review of stock market prediction using machine learning and statistical techniques. Materials Today: Proceedings, 49: 3187-3191. https://doi.org/10.1016/j.matpr.2020.11.399 [Google Scholar]

- Kumar I, Dogra K, Utreja C, and Yadav P (2018). A comparative study of supervised machine learning algorithms for stock market trend prediction. In the 2nd International Conference on Inventive Communication and Computational Technologies, IEEE, Coimbatore, India: 1003-1007. https://doi.org/10.1109/ICICCT.2018.8473214 [Google Scholar]

- Luong HV (2022). Emerging destinations. In: Buhalis D (Ed.), Encyclopedia of tourism management and marketing: 54–56. Edward Elgar Publishing, Cheltenham, UK. https://doi.org/10.4337/9781800377486.emerging.destinations [Google Scholar]

- Meher BK, Singh M, Birau R, and Anand A (2024). Forecasting stock prices of fintech companies of India using random forest with high-frequency data. Journal of Open Innovation: Technology, Market, and Complexity, 10(1): 100180. https://doi.org/10.1016/j.joitmc.2023.100180 [Google Scholar]

- Mohan S, Mullapudi S, Sammeta S, Vijayvergia P, and Anastasiu DC (2019). Stock price prediction using news sentiment analysis. In the 5th International Conference on Big Data Computing Service and Applications, IEEE, Newark, USA: 205-208. https://doi.org/10.1109/BigDataService.2019.00035 [Google Scholar]

- Owusu F (2023). Analysis of market volatility and economic factors in emerging markets. International Journal of Modern Risk Management, 1(1): 1-11. https://doi.org/10.47604/ijmrm.2093 [Google Scholar]

- Raza HMZ, Haider G, and Haider SZ (2024). Forecasting stock prices: Exploring the potential of ARIMA model for short-term predictions. International Journal of Management Research and Emerging Sciences, 14(4): 1-21. https://doi.org/10.56536/ijmres.v14i4.654 [Google Scholar]

- Suji FC and Kitur B (2022). Influence of strategic direction and human capital on competitive advantage in the telecommunications industry in Kenya: A case of Safaricom Limited. International Journal of Research Publications, 109(1): 264-283. https://doi.org/10.47119/IJRP1001091920223904 [Google Scholar]

- Ullah N and Asghar U (2023). Efficient market hypothesis: An exploratory study of FTSE-100 stock market. Journal of Business and Tourism, 9(1): 12–20. https://doi.org/10.34260/jbt.v9i01.269 [Google Scholar]

- Vijh M, Chandola D, Tikkiwal VA, and Kumar A (2020). Stock closing price prediction using machine learning techniques. Procedia Computer Science, 167: 599-606. https://doi.org/10.1016/j.procs.2020.03.326 [Google Scholar]

- Werawithayaset P and Tritilanunt S (2019). Stock closing price prediction using machine learning. In the 17th International Conference on ICT and Knowledge Engineering, IEEE, Bangkok, Thailand: 1-8. https://doi.org/10.1109/ICTKE47035.2019.8966836 [Google Scholar]

- Wu S, Liu Y, Zou Z, and Weng TH (2022). S_I_LSTM: Stock price prediction based on multiple data sources and sentiment analysis. Connection Science, 34(1): 44-62. https://doi.org/10.1080/09540091.2021.1940101 [Google Scholar]

- Xu C (2023). Efficient market hypothesis in contemporary applications: A systematic review on theoretical models, experimental validation, and practical application. Highlights in Business, Economics and Management, 21: 231–239. https://doi.org/10.54097/hbem.v21i.14337 [Google Scholar]

- Yang M, Zhang Q, Yi A, and Peng P (2021). Geopolitical risk and stock market volatility in emerging economies: Evidence from GARCH‐MIDAS model. Discrete Dynamics in Nature and Society, 2021(1): 1159358. https://doi.org/10.1155/2021/1159358 [Google Scholar]

- Yeung K (2024). ARIMA model application in predicting NVIDIA’s stock price. Advances in Economics, Management and Political Sciences, 128(1): 220–230. https://doi.org/10.54254/2754-1169/2024.18620 [Google Scholar]

- Yuan F (2024). Research on time-series financial data prediction and analysis based on deep recurrent neural network. Applied and Computational Engineering, 69(1): 140-146. https://doi.org/10.54254/2755-2721/69/20241498 [Google Scholar]

- Zafar A (2023). Emerging markets in a world of chaos. Springer, Berlin, Germany. https://doi.org/10.1007/978-3-031-29949-0 [Google Scholar]

- Zhang D and Lou S (2021). The application research of neural network and BP algorithm in stock price pattern classification and prediction. Future Generation Computer Systems, 115: 872-879. https://doi.org/10.1016/j.future.2020.10.009 [Google Scholar]

- Zhao J, Zeng D, Liang S, Kang H, and Liu Q (2021). Prediction model for stock price trend based on recurrent neural network. Journal of Ambient Intelligence and Humanized Computing, 12: 745-753. https://doi.org/10.1007/s12652-020-02057-0 [Google Scholar]