International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 7 (July 2025), Pages: 34-46

----------------------------------------------

Original Research Paper

Using digital technology to standardize accounting information systems

Author(s):

Affiliation(s):

Accounting and Business Management Department, Thuyloi University, 175 Tay Son, Dong Da, Hanoi, Vietnam

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7034-0105

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7034-0105

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.07.004

Abstract

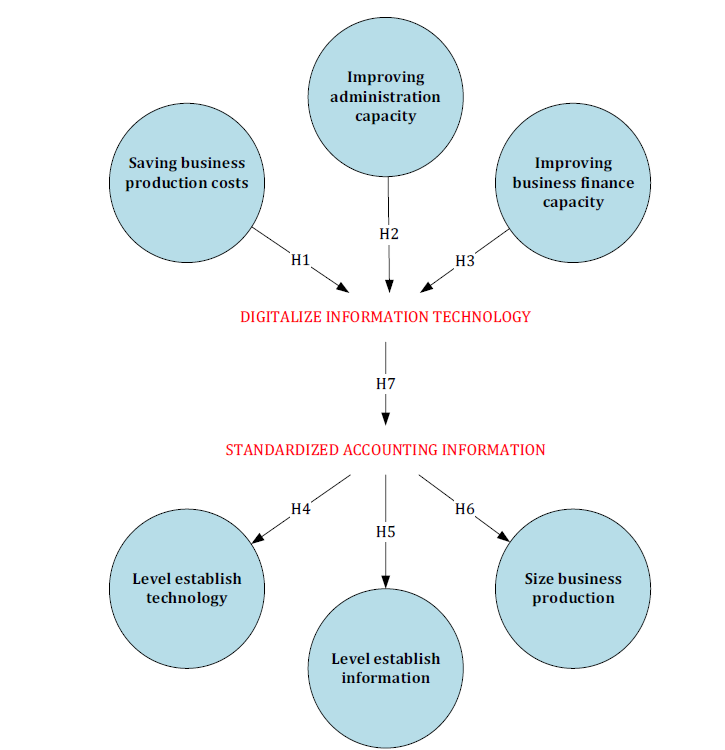

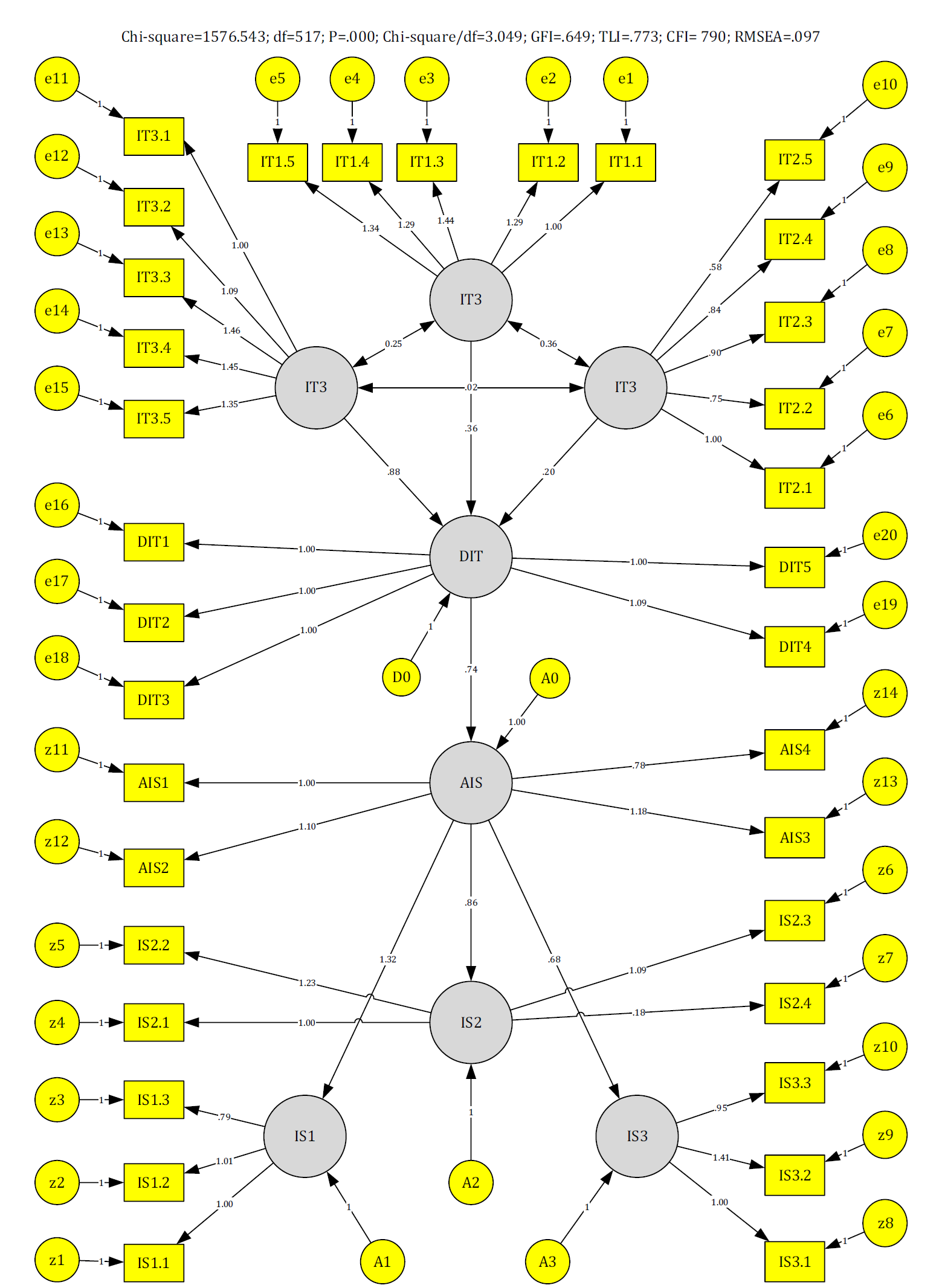

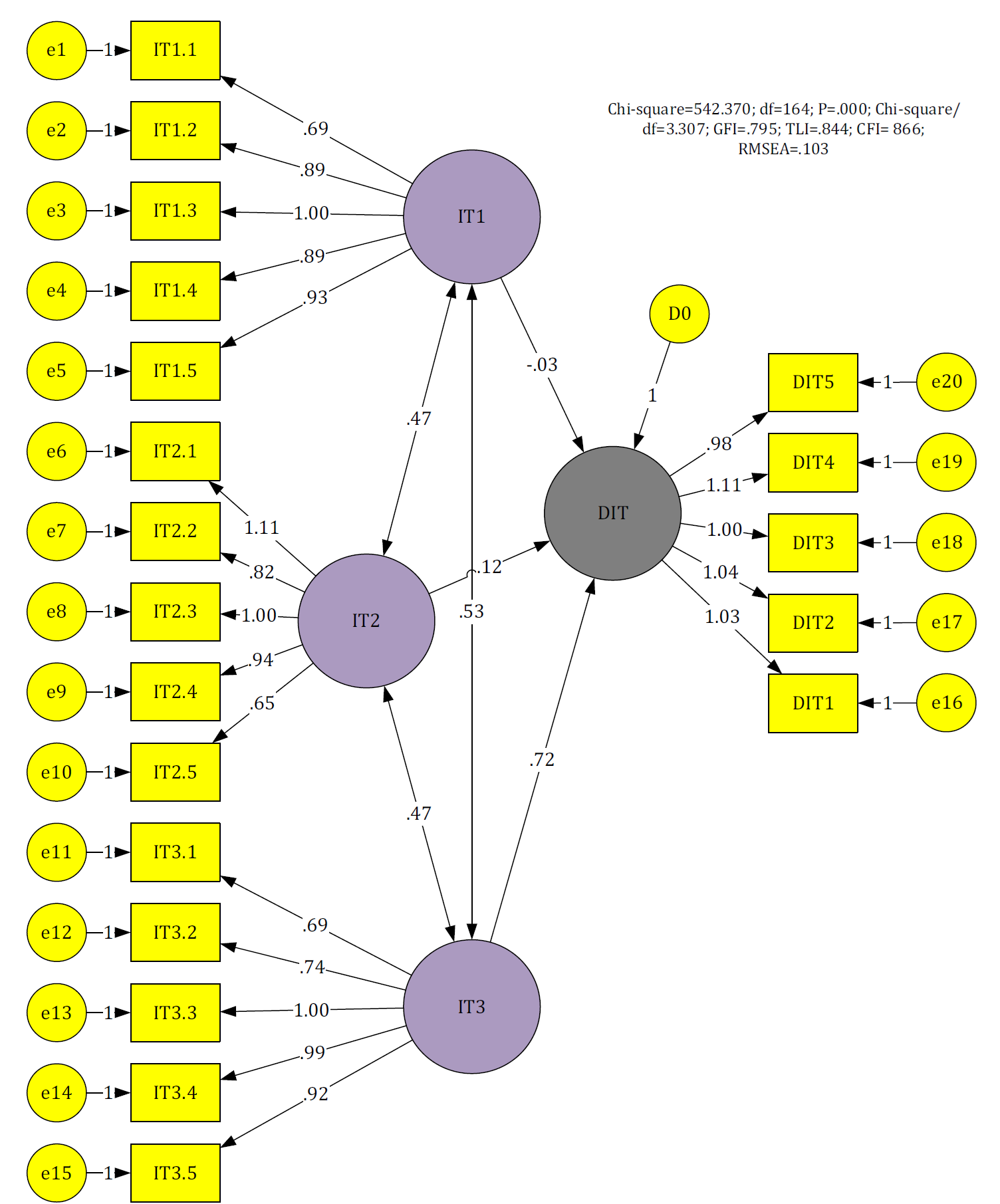

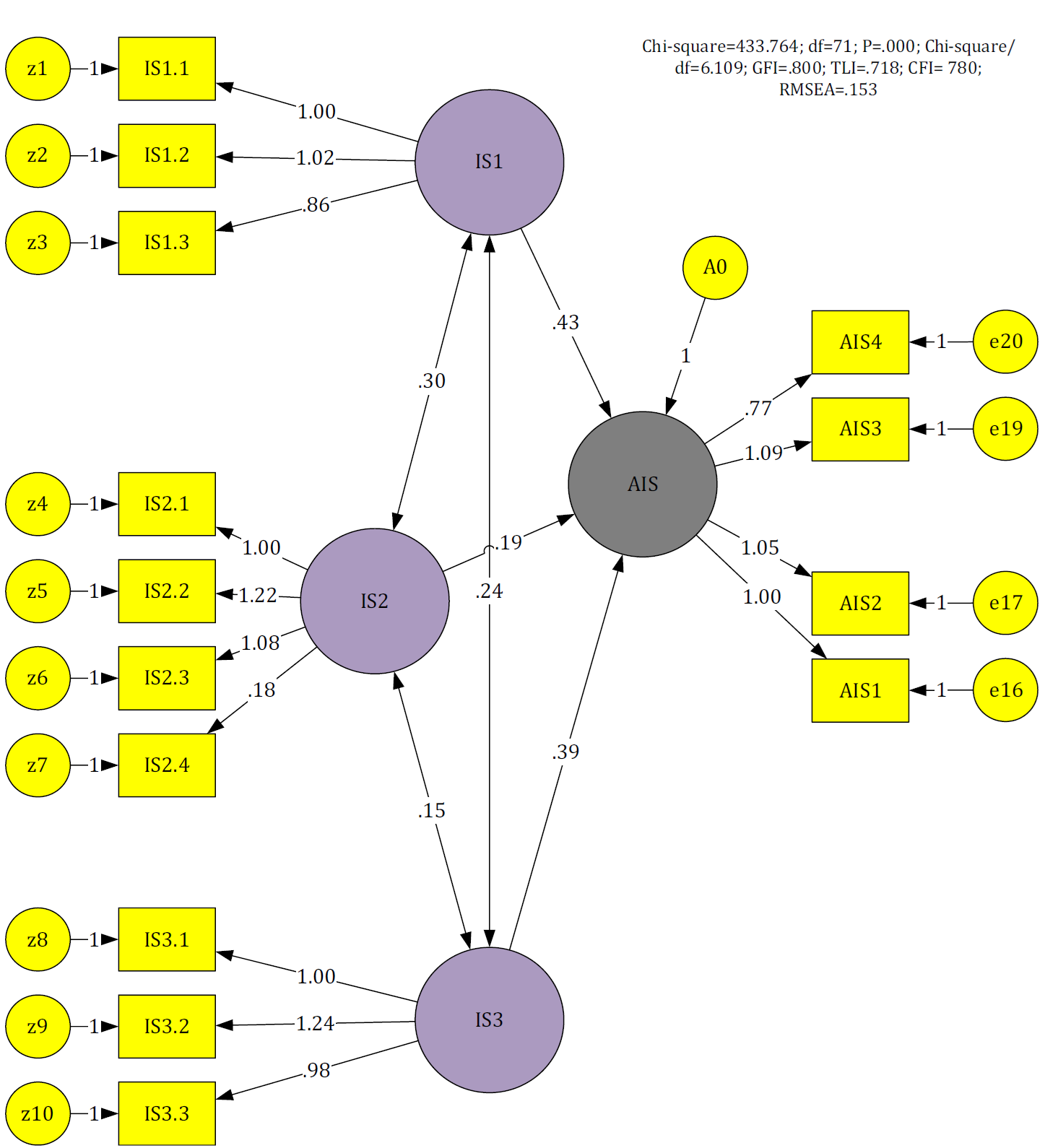

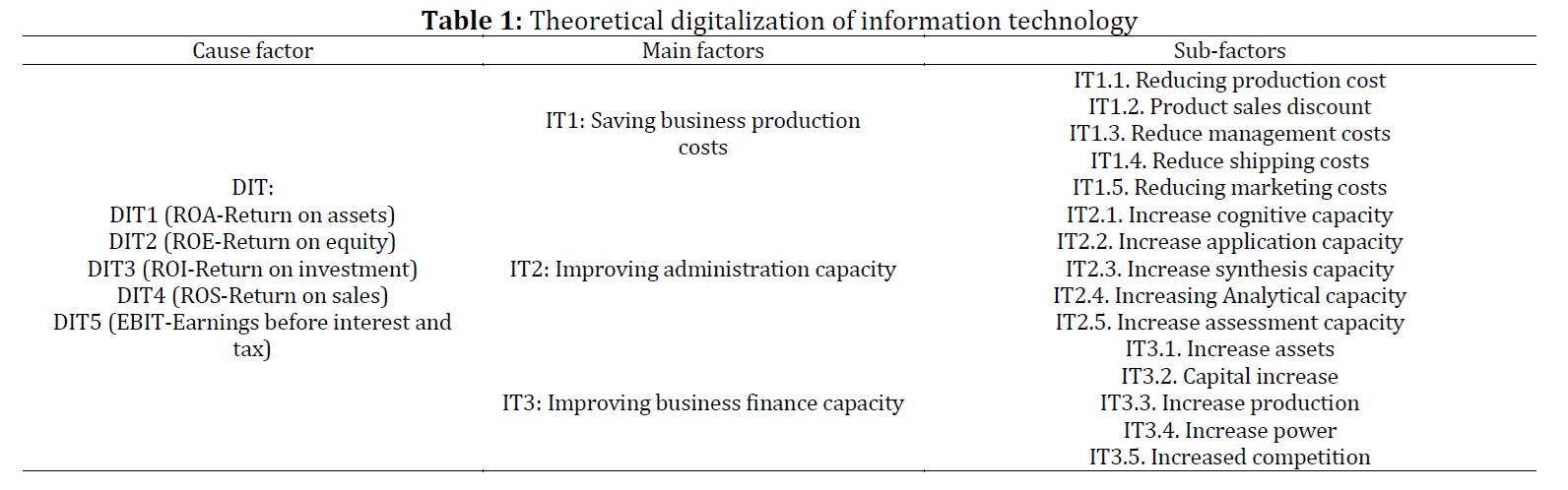

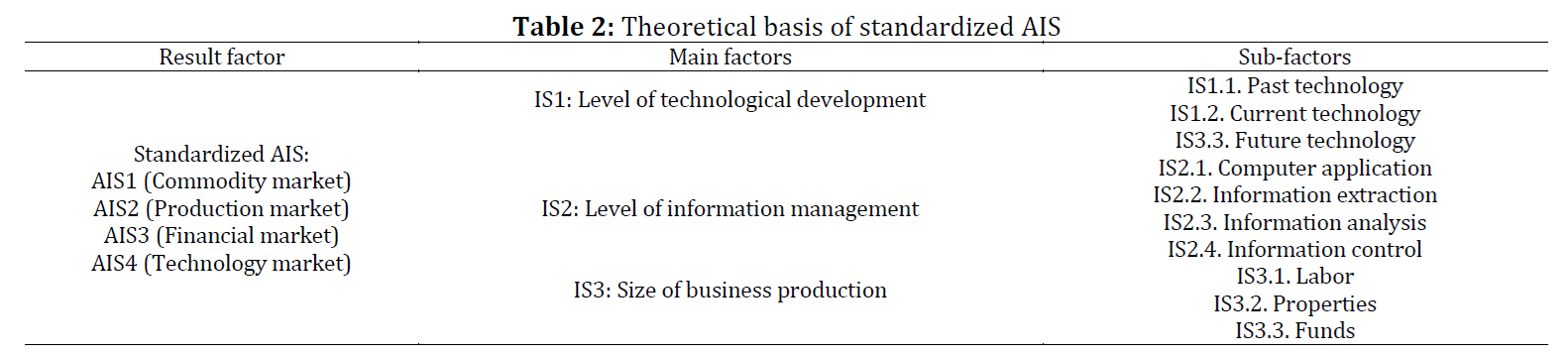

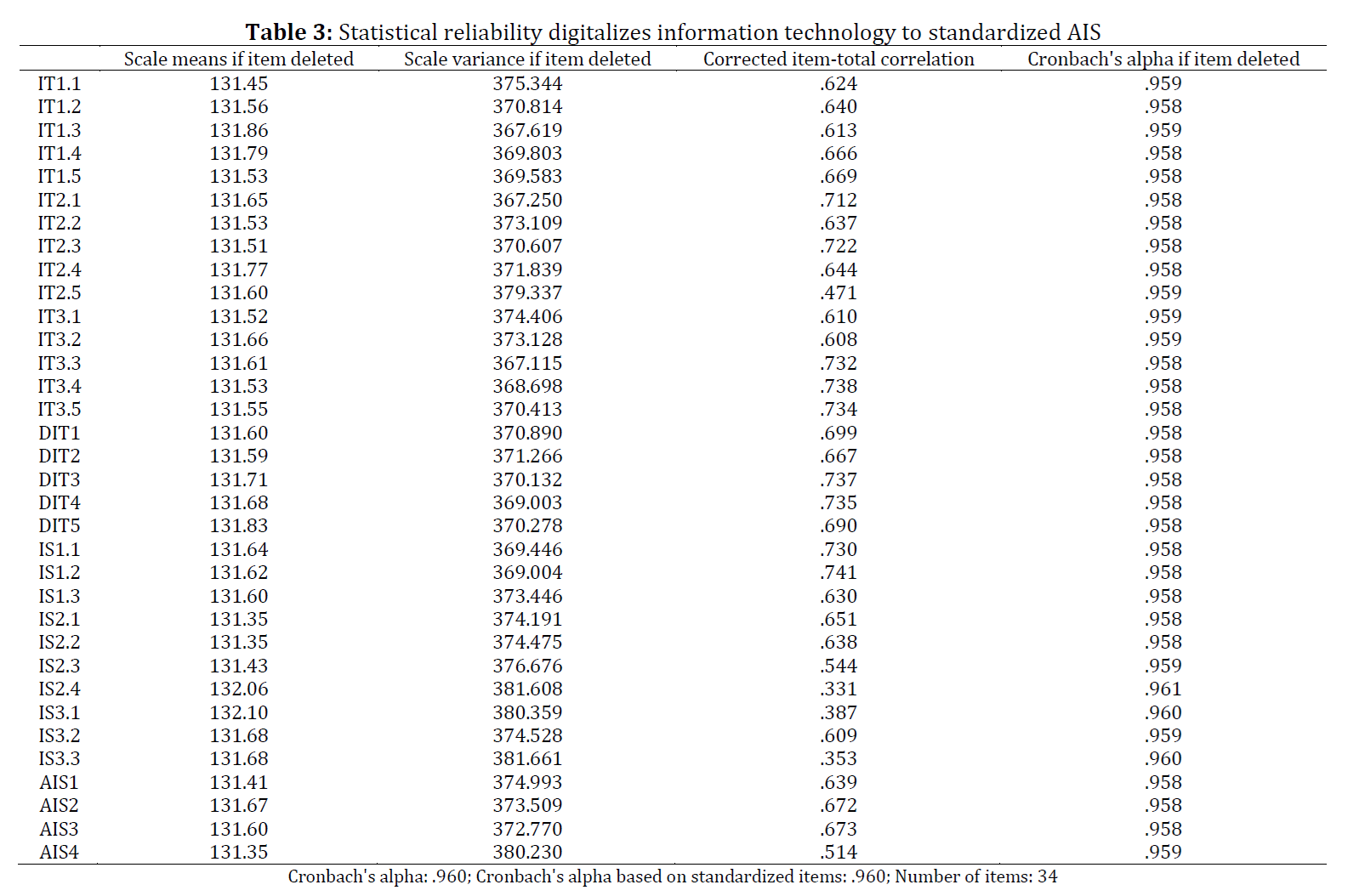

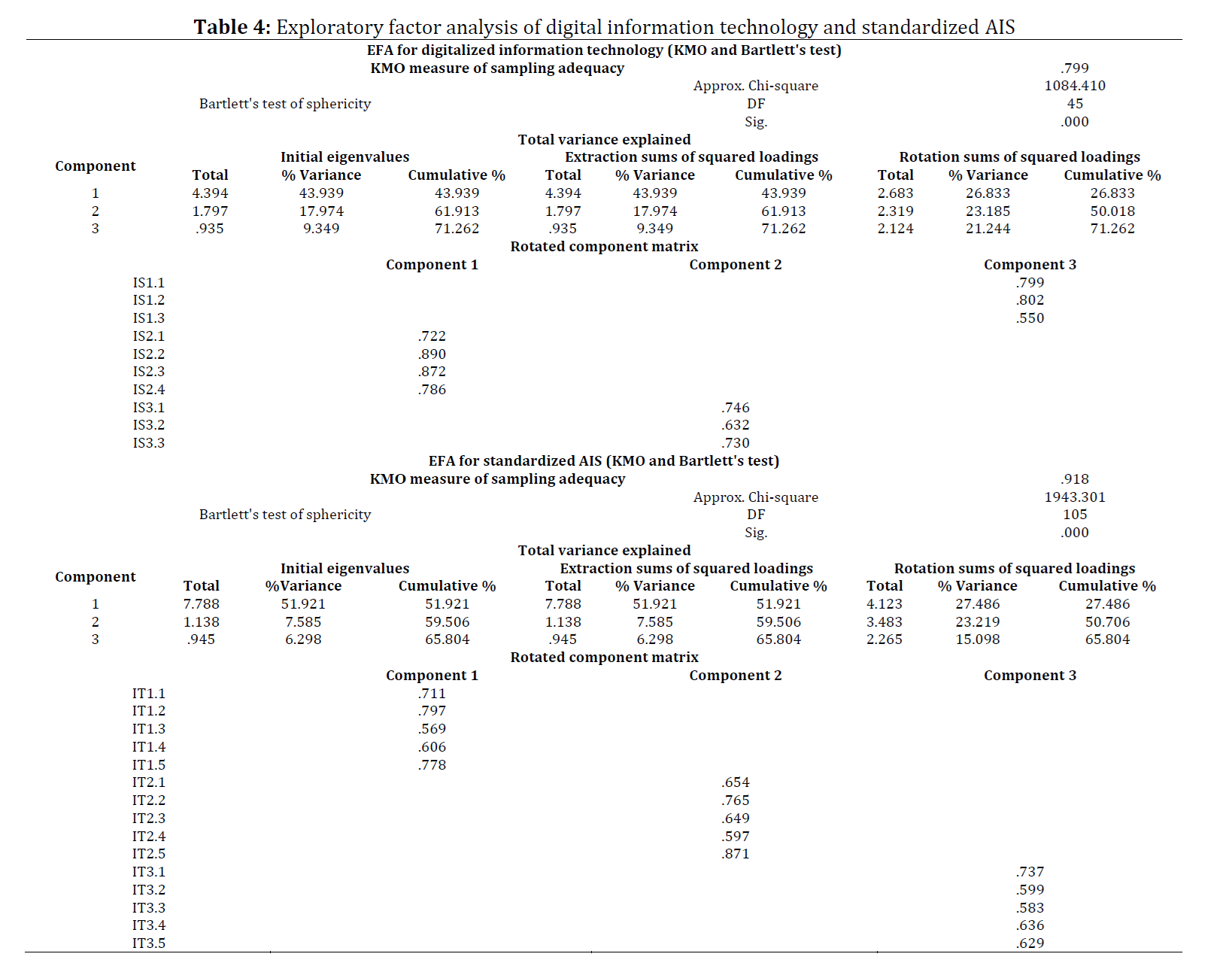

This study explores how digital technology helps to standardize accounting information systems. Using both qualitative and quantitative research methods, it examines socio-economic aspects of production, business, trade, and services. A theoretical framework is created, research hypotheses are presented, and primary data is analyzed using SPSS and AMOS software. The results show that digitalization supports the standardization of accounting systems by lowering production costs, strengthening administrative functions, improving financial performance, and increasing profits. The accounting information system is evaluated based on system scale, information processes, use of technology, and production activities. The study also highlights that for organizations to achieve long-term and stable growth through digital transformation, they need to plan effective business strategies and align their goals with their industry’s characteristics.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Digital technology, Accounting systems, Business strategy, Financial performance, Digital transformation

Article history

Received 3 October 2024, Received in revised form 11 May 2025, Accepted 7 June 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Ethical considerations

All participants provided informed consent prior to participating in the survey. Participation was voluntary, and responses were kept confidential.

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Nam TN, Thanh HH, and Thu TDT (2025). Using digital technology to standardize accounting information systems. International Journal of Advanced and Applied Sciences, 12(7): 34-46

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (34)

- Akerlof GA (2017). The market for “lemons”: Quality uncertainty and the market mechanism. Decision Science, 84(3): 261-273. https://doi.org/10.2307/1879431 [Google Scholar]

- Ashif ASM, Mahmud MT, and Hasan MT (2013). AIS requirement and capacity, an understanding of AIS alignment: Evidence from Bangladesh. International Journal of Applied Research in Business Administration and Economics, 2(6): 22-31. [Google Scholar]

- Azar N, Zakaria Z, and Sulaiman NA (2019). The quality of accounting information: Relevance or value-relevance? Asian Journal of Accounting Perspectives, 12(1): 1-21. https://doi.org/10.22452/AJAP.vol12no1.1 [Google Scholar]

- Bodnar GH and Hopwood WS (2014). Accounting information systems. 11th Edition, Pearson, London, UK. [Google Scholar]

- Budiarto DS, Rahmawati, Prabowo MA, Bandi, Djajanto L, Widodo KP, and Herawan T (2018). Accounting information system (AIS) alignment and non-financial performance in small firm: A contingency perspective. In the Computational Science and Its Applications: 18th International Conference, Springer International Publishing, Melbourne, Australia: 382-394. https://doi.org/10.1007/978-3-319-95165-2_27 [Google Scholar]

- Chong VK (1996). Management accounting systems, task uncertainty and managerial performance: A research note. Accounting, Organizations and Society, 21(5): 415-421. https://doi.org/10.1016/0361-3682(95)00045-3 [Google Scholar]

- Davis FD (1993). User acceptance of information technology: System characteristics, user perceptions and behavioral impacts. International Journal of Man-Machine Studies, 38(3): 475-487. https://doi.org/10.1006/imms.1993.1022 [Google Scholar]

- Esmeray A (2016). The impact of accounting information systems (AIS) on firm performance: Empirical evidence in Turkish small and medium sized enterprises. International Review of Management and Marketing, 6(2): 233-236. [Google Scholar]

- Galbraith JR (1973). Designing complex organizations. Addison-Wesley Longman Publishing, Boston, USA. [Google Scholar]

- Hang NNT and Kim NN (2025). The impact of digital technology on the performance of small and medium-sized enterprises. International Journal of Advanced and Applied Sciences, 12(3): 38-48. https://doi.org/10.21833/ijaas.2025.03.005 [Google Scholar]

- Harris ML and Gibson SG (2006). Determining the common problems of early growth small businesses in Eastern North Carolina. SAM Advanced Management Journal, 71(2): 39-45. [Google Scholar]

- Harris ML, Grubb III WL, and Hebert FJ (2005). Critical problems of rural small businesses: A comparison of African-American and white-owned formation and early growth firms. Journal of Developmental Entrepreneurship, 10(3): 223-238. https://doi.org/10.1142/S1084946705000185 [Google Scholar]

- Hoang TH, Do VQ, and Nguyen NS (2024). Accounting information systems governance in a digital landscape: A comprehensive analysis of key factors and sectoral dynamics. Journal of Governance and Regulation, 13(3): 139–149. https://doi.org/10.22495/jgrv13i3art12 [Google Scholar]

- Hung BQ, Hoa TA, Hoai TT, and Nguyen NP (2023). Advancement of cloud-based accounting effectiveness, decision-making quality, and firm performance through digital transformation and digital leadership: Empirical evidence from Vietnam. Heliyon, 9(6): e16929. https://doi.org/10.1016/j.heliyon.2023.e16929 [Google Scholar] PMid:37332940 PMCid:PMC10275964

- Ismail NA (2009). Factors influencing AIS effectiveness among manufacturing SMEs: Evidence from Malaysia. The Electronic Journal of Information Systems in Developing Countries, 38(1): 1-19. https://doi.org/10.1002/j.1681-4835.2009.tb00273.x [Google Scholar]

- Kaplan RS and Roll R (1972). Investor evaluation of accounting information: Some empirical evidence. The Journal of Business, 45(2): 225-257. https://doi.org/10.1086/295446 [Google Scholar]

- Kareem HM, Aziz KA, Maelah R, Yunus YM, and Dauwed M (2019). Enterprises performance based accounting information system: Success factors. Asian Journal of Scientific Research, 12(1): 29-40. https://doi.org/10.3923/ajsr.2019.29.40 [Google Scholar]

- Kharuddin S, Ashhari ZM, and Nassir AM (2010). Information system and firms’ performance: The case of Malaysian small medium enterprises. International Business Research, 3(4): 28-35. https://doi.org/10.5539/ibr.v3n4p28 [Google Scholar]

- Khazanchi D (2005). Information technology (IT) appropriateness: The contingency theory of “fit” and IT implementation in small and medium enterprises. Journal of Computer Information Systems, 45(3): 88-95. [Google Scholar]

- Louadi ME (1998). The relationship among organization structure, information technology and information processing in small Canadian firms. Canadian Journal of Administrative Sciences/Revue Canadienne des Sciences de l'Administration, 15(2): 180-199. https://doi.org/10.1111/j.1936-4490.1998.tb00161.x [Google Scholar]

- Manurung ET and Manurung EM (2019). A new approach of bank credit assessment for SMES. Academy of Accounting and Financial Studies Journal, 23(3): 1-13. [Google Scholar]

- Mitchell F, Reid GC, and Smith J (2000). Information system development in the small firm: The use of management accounting. CIMA Publishing, London, UK. [Google Scholar]

- Mitchell F, Reid GC, and Terry NG (1997). Venture capital supply and accounting information system development. Entrepreneurship Theory and Practice, 21(4): 45-62. https://doi.org/10.1177/104225879702100404 [Google Scholar]

- Mulyani S and Arum EDP (2016). The influence of manager competency and internal control effectiveness toward accounting information quality. International Journal of Applied Business and Economic Research, 14(1): 181-190. [Google Scholar]

- Nguyen HQ, Oanh T, Le TT, Hoang HT, Truong TV, and Pham HT (2023). Factors affecting digital transformation in accounting: The case of Vietnamese enterprises. Journal for ReAttach Therapy and Developmental Diversities, 6: 934–945. [Google Scholar]

- Perren L and Grant P (2000). The evolution of management accounting routines in small businesses: A social construction perspective. Management Accounting Research, 11(4): 391-411. https://doi.org/10.1006/mare.2000.0141 [Google Scholar]

- Prasad A and Green P (2015). Organizational competencies and dynamic accounting information system capability: Impact on AIS processes and firm performance. Journal of Information Systems, 29(3): 123-149. https://doi.org/10.2308/isys-51127 [Google Scholar]

- Rama DV and Jones FL (2006). Accounting information systems: A business process approach. Thomson, Toronto, Canada. [Google Scholar]

- Romney M, Steinbart P, Mula J, McNamara R, and Tonkin T (2012). Accounting information systems Australasian edition. Pearson Higher Education AU, Melbourne, Australia. [Google Scholar]

- Stokes D and Blackburn R (2002). Learning the hard way: The lessons of owner-managers who have closed their businesses. Journal of Small Business and Enterprise Development, 9(1): 17-27. https://doi.org/10.1108/14626000210419455 [Google Scholar]

- Trabulsi RU (2018). The impact of accounting information systems on organizational performance: The context of Saudi's SMEs. International Review of Management and Marketing, 8(2): 69-73. [Google Scholar]

- van Bertalanffy L (2008). General system theory: Foundations, development, applications. George Braziller, New York, USA. [Google Scholar]

- Venkatesh V and Zhang X (2010). Unified theory of acceptance and use of technology: US vs. China. Journal of Global Information Technology Management, 13(1): 5-27. https://doi.org/10.1080/1097198X.2010.10856507 [Google Scholar]

- Weill P and Olson MH (1989). An assessment of the contingency theory of management information systems. Journal of Management Information Systems, 6(1): 59-86. https://doi.org/10.1080/07421222.1989.11517849 [Google Scholar]