International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 5 (May 2025), Pages: 156-167

----------------------------------------------

Original Research Paper

Ownership structure, board characteristics, and audit quality demand: Evidence from Saudi-listed companies

Author(s):

Affiliation(s):

Accounting Department, Business College, Al Imam Mohammad Ibn Saud Islamic University (IMSIU), Riyadh 12477, Saudi Arabia

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-3837-7861

Corresponding author's ORCID profile: https://orcid.org/0000-0002-3837-7861

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.05.015

Abstract

This study examines the impact of ownership structure and board characteristics on the demand for high-quality audit services in Saudi-listed firms, drawing on agency and stakeholder theories. Using panel data from 162 firms listed on the Saudi Stock Market (Tadawul) between 2018 and 2023, audit quality is measured by auditor brand (Big Four vs. non-Big Four), with audit fees used as an alternative measure for robustness. A Two-Stage Least Squares (2SLS) regression with instrumental variables is applied to address endogeneity. The findings reveal that firms with higher foreign and institutional ownership are more likely to engage high-quality auditors, while family ownership has no significant effect. Additionally, greater board independence and gender diversity positively influence the demand for audit quality. These results are consistent across different measures of audit quality. The study offers valuable insights for investors, policymakers, and regulators, suggesting that promoting independent and diverse boards, along with encouraging foreign institutional investment, can enhance audit quality, reduce agency costs, and strengthen corporate governance in Saudi Arabia.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Audit quality, Ownership structure, Board characteristics, Corporate governance, Saudi stock market

Article history

Received 19 October 2024, Received in revised form 6 April 2025, Accepted 5 May 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Zehri F (2025). Ownership structure, board characteristics, and audit quality demand: Evidence from Saudi-listed companies. International Journal of Advanced and Applied Sciences, 12(5): 156-167

Figures

No Figure

Tables

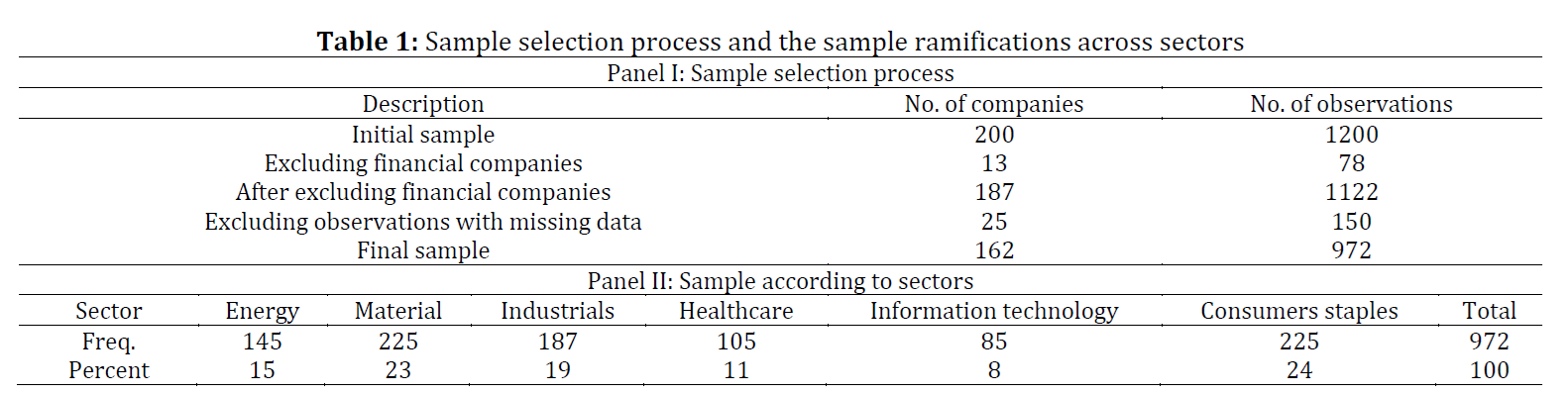

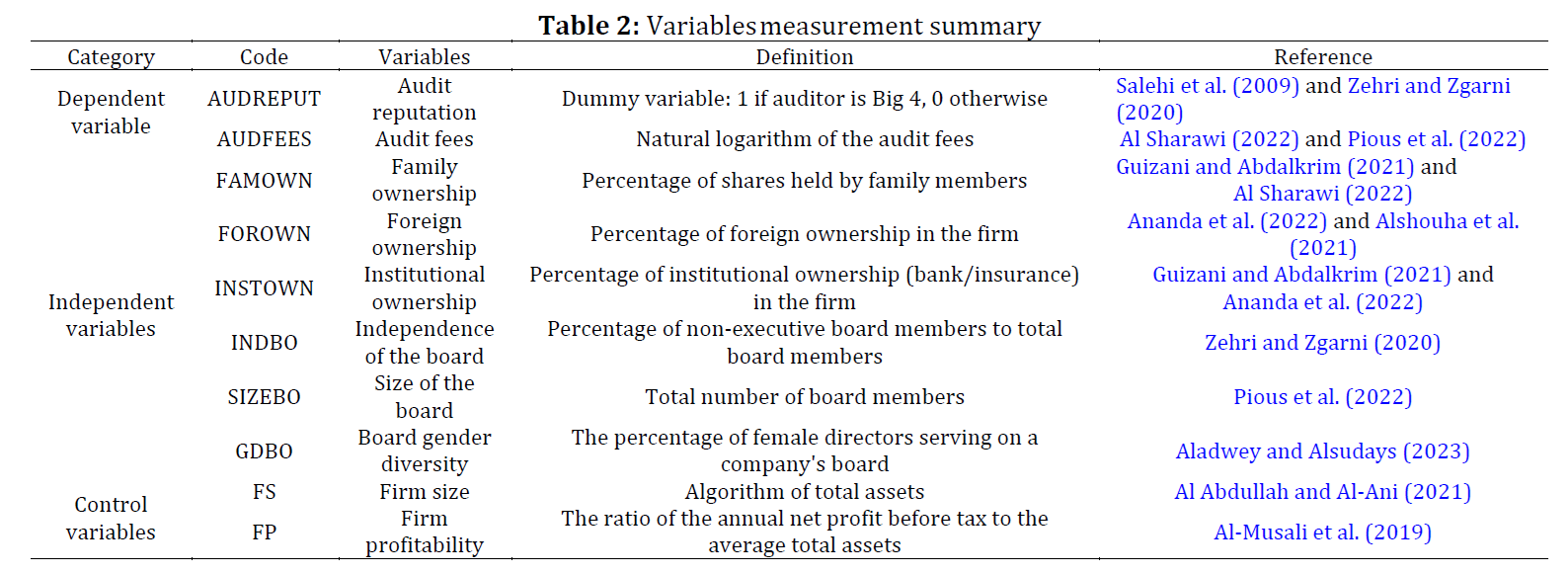

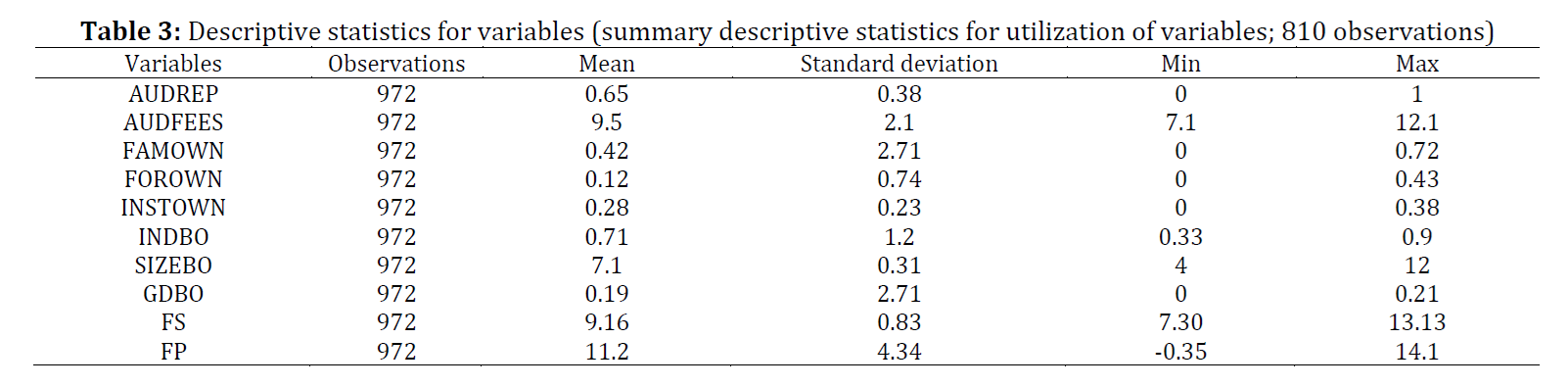

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (47)

- Abbott LJ, Parker S, and Peters GF (2004). Audit committee characteristics and restatements. Auditing: A journal of practice and theory, 23(1): 69-87. https://doi.org/10.2308/aud.2004.23.1.69 [Google Scholar]

- Abdel-Meguid A, Abuzeid M, El-Helaly M, and Shehata N (2023). The relationship between board gender diversity and audit quality in Egypt. Journal of Economic and Administrative Sciences. https://doi.org/10.1108/JEAS-08-2022-0199 [Google Scholar]

- Al Abdullah RJ and AL Ani MK (2021). The impacts of interaction of audit litigation and ownership structure on audit quality. Future Business Journal, 7(1): 19. https://doi.org/10.1186/s43093-021-00067-8 [Google Scholar]

- Al Nasser Z (2020). The effect of royal family members on the board on firm performance in Saudi Arabia. Journal of Accounting in Emerging Economies, 10(3): 487-518. https://doi.org/10.1108/JAEE-04-2017-0041 [Google Scholar]

- Al Sharawi HHM (2022). The impact of ownership structure on external audit quality: A comparative study between Egypt and Saudi Arabia. Investment Management and Financial Innovations, 19(2): 81-94. https://doi.org/10.21511/imfi.19(2).2022.07 [Google Scholar]

- Aladwey LMA and Alsudays RA (2023). Does the cultural dimension influence the relationship between firm value and board gender diversity in Saudi Arabia, mediated by ESG scoring? Journal of Risk and Financial Management, 16(12): 512. https://doi.org/10.3390/jrfm16120512 [Google Scholar]

- Al-Faryan MAS and Dockery E (2021). Testing for efficiency in the Saudi stock market: Does corporate governance change matter? Review of Quantitative Finance and Accounting, 57(1): 61-90. https://doi.org/10.1007/s11156-020-00939-0 [Google Scholar]

- Al-Ghamdi M and Rhodes M (2015). Family ownership, corporate governance and performance: Evidence from Saudi Arabia. International Journal of Economics and Finance, 7(2): 78-89. https://doi.org/10.5539/ijef.v7n2p78 [Google Scholar]

- Aljaaidi K, Sharma R, and Bagais O (2021). The effect of board characteristics on the audit committee meeting frequency. Accounting, 7(4): 899-906. https://doi.org/10.5267/j.ac.2021.1.018 [Google Scholar]

- Al-Matari EM and Al-Hebry AA (2019). The impact of government, foreign and institutional ownership and firm performance on audit quality using regression analysis. Industrial Engineering and Management Systems, 18(3): 395-406. https://doi.org/10.7232/iems.2019.18.3.395 [Google Scholar]

- Al-Musali MA, Qeshta MH, Al-Attafi MA, and Al-Ebel AM (2019). Ownership structure and audit committee effectiveness: evidence from top GCC capitalized firms. International Journal of Islamic and Middle Eastern Finance and Management, 12(3): 407-425. https://doi.org/10.1108/IMEFM-03-2018-0102 [Google Scholar]

- Alrawashdeh B (2021). The effect of family-owned enterprises on the quality of auditing systems. International Journal of Entrepreneurship, 25: 1-11. [Google Scholar]

- Alshouha LF, Ismail WNS, Mojhtar MZ, and Rashid NM (2021). The impact of audit quality on financial performance in Jordan. Solid State Technology, 64(2): 947-959. [Google Scholar]

- Ananda AS, Sumarta NH, Satriya KKT, and Amidjaya PG (2022). Determinants of audit quality: The effect of ownership structure and audit committee activities. EKUITAS (Jurnal Ekonomi Dan Keuangan), 6(3): 333–350. https://doi.org/10.24034/j25485024.y2022.v6.i3.5214 [Google Scholar]

- Becchetti L, Ciciretti R, and Conzo P (2020). Legal origins and corporate social responsibility. Sustainability, 12(7): 2717. https://doi.org/10.3390/su12072717 [Google Scholar]

- Ben Ali C and Lesage C (2014). Audit fees in family firms: evidence from U.S. listed companies. The Journal of Applied Business Research, 3(3): 807-814. https://doi.org/10.19030/jabr.v30i3.8566 [Google Scholar]

- Boshnak HA, Alsharif M, and Alharthi M (2023). Corporate governance mechanisms and firm performance in Saudi Arabia before and during the COVID-19 outbreak. Cogent Business and Management, 10(1): 2195990. https://doi.org/10.1080/23311975.2023.2195990 [Google Scholar]

- Buallay A, Hamdan A, and Zureigat Q (2017). Corporate governance and firm performance: Evidence from Saudi Arabia. Australasian Accounting, Business and Finance Journal, 11(1): 78-98. https://doi.org/10.14453/aabfj.v11i1.6 [Google Scholar]

- Charbel S, Elie B, and Georges S (2013). Impact of family involvement in ownership management and direction on financial performance of the Lebanese firms. International Strategic Management Review, 1(1-2): 30-41. https://doi.org/10.1016/j.ism.2013.08.003 [Google Scholar]

- DeAngelo LE (1981). Auditor size and audit quality. Journal of Accounting and Economics, 3(3): 183-199. https://doi.org/10.1016/0165-4101(81)90002-1 [Google Scholar]

- Eulaiwi B, Al-Hadi A, Taylor G, Al-Yahyaee KH, and Evans J (2016). Multiple directorships, family ownership and the board nomination committee: International Evidence from the GCC. Emerging Markets Review, 28: 61-88. https://doi.org/10.1016/j.ememar.2016.06.004 [Google Scholar]

- Fossung MF, Mukah ST, Berthelo KW, and Nsai ME (2022). The demand for external audit quality: The contribution of agency theory in the context of Cameroon. Accounting and Finance Research, 11(1): 1-13. https://doi.org/10.5430/afr.v11n1p13 [Google Scholar]

- Guizani M and Abdalkrim G (2021). Ownership structure and audit quality: The mediating effect of board independence. Corporate Governance, 21(5): 754-774. https://doi.org/10.1108/CG-12-2019-0369 [Google Scholar]

- Gujarati DN (2005). Basic econometrics. 4 th McGraw-Hill, New York, USA. [Google Scholar]

- Habib A, Wu J, Bhuiyan MBU, and Sun X (2019). Determinants of auditor choice: Review of the empirical literature. International Journal of Auditing, 23(2):308–335. https://doi.org/10.1111/ijau.12163 [Google Scholar]

- Jensen MC and Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [Google Scholar]

- Kalia D, Basu D, and Kundu S (2023). Board characteristics and demand for audit quality: A meta-analysis. Asian Review of Accounting, 31(1): 153-175. https://doi.org/10.1108/ARA-05-2022-0121 [Google Scholar]

- Khan A, Mihret DG, and Muttakin MB (2016). Corporate political connections, agency costs and audit quality. International Journal of Accounting and Information Management, 24(4): 357-374. https://doi.org/10.1108/IJAIM-05-2016-0061 [Google Scholar]

- Khan A, Muttakin MB, and Siddiqui J (2013). Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. Journal of Business Ethics, 114: 207-223. https://doi.org/10.1007/s10551-012-1336-0 [Google Scholar]

- Khan F, Abdul-Hamid MAB, Fauzi Saidin S, and Hussain S (2023). Organizational complexity and audit report lag in GCC economies: The moderating role of audit quality. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-03-2023-0113 [Google Scholar]

- Lai KMY, Bin Srinidhi B, Gul FA, and Tsui JSL (2017). Board gender diversity, auditor fees, and auditor choice. Contemporary Accounting Research, 34(3): 1681-1714. https://doi.org/10.1111/1911-3846.12313 [Google Scholar]

- Mitra S, Hossain M, and Deis D (2007). The empirical relationship between ownership characteristics and audit fees. Review of Quantitative Finance and Accounting, 28(3): 257-285. https://doi.org/10.1007/s11156-006-0014-7 [Google Scholar]

- Mustafa AS, Che-Ahmad A, and Chandren S (2018). Board diversity, audit committee characteristics and audit quality: The moderating role of control-ownership wedge. Business and Economic Horizons, 14(3): 587-614. https://doi.org/10.15208/beh.2018.42 [Google Scholar]

- Olabisi J, Abeokuta, Kajola SO, Abioro MA and Oworu OO (2020). Determinants of audit quality: Evidence from Nigerian listed insurance companies. Journal of Volgograd State University Economics, 22(2): 183-191. https://doi.org/10.15688/ek.jvolsu.2020.2.17 [Google Scholar]

- Peni E and Vahamaa S (2010). Female executives and earnings management. Managerial Finance, 36(7): 629-645. https://doi.org/10.1108/03074351011050343 [Google Scholar]

- Pious O, Arthur B, Bimpong P, and Kyeremeh G (2022). The impact of board characteristics on audit quality, evidence-based on listed firms in Ghana. International Journal of Economics, Business and Management Research, 6(10): 64-85. https://doi.org/10.51505/IJEBMR.2022.61005 [Google Scholar]

- Sahasranamam S, Arya B, and Sud M (2020). Ownership structure and corporate social responsibility in an emerging market. Asia Pacific Journal of Management, 37(4): 1165-1192. https://doi.org/10.1007/s10490-019-09649-1 [Google Scholar]

- Saidu M and Aifuwa HO (2020). Board characteristics and audit quality: The moderating role of gender diversity. International Journal of Business and Law Research, 8(1): 144-155. https://doi.org/10.2139/ssrn.3544733 [Google Scholar]

- Salehi M, Mansoury A, and Pirayesh R (2009). Firm size and audit regulation and fraud detection: Empirical evidence from Iran. ABAC Journal, 29(1): 53-65. https://doi.org/10.5539/ijef.v1n1p165 [Google Scholar]

- Sanad Z and Al Lawati H (2023). Board gender diversity and firm performance: the moderating role of financial technology. Competitiveness Review: An International Business Journal. https://doi.org/10.1108/CR-05-2023-0103 [Google Scholar]

- Scott WR (2008). Approaching adulthood: The maturing of institutional theory. Theory and Society, 37: 427-442. https://doi.org/10.1007/s11186-008-9067-z [Google Scholar]

- Semykina A and Wooldridge JM (2010). Estimating panel data models in the presence of endogeneity and selection. Journal of Econometrics, 157(2): 375-380. https://doi.org/10.1016/j.jeconom.2010.03.039 [Google Scholar]

- Tawfik OI, Alsmady AA, Rahman RA, and Alsayegh MF (2022). Corporate governance mechanisms, royal family ownership and corporate performance: Evidence in Gulf Cooperation Council (GCC) market. Heliyon, 8(12): e12389. https://doi.org/10.1016/j.heliyon.2022.e12389 [Google Scholar] PMid:36636223 PMCid:PMC9830172

- Yu H, Liang C, Liu Z, and Wang H (2023). News-based ESG sentiment and stock price crash risk. International Review of Financial Analysis, 88: 102646. https://doi.org/10.1016/j.irfa.2023.102646 [Google Scholar]

- Zehri F and Ben Flah I (2024). Impact of Saudi corporate governance code and governance structures on industrial firms' performance in Saudi Arabia. International Journal of Advanced and Applied Sciences, 11(4): 216-227. https://doi.org/10.21833/ijaas.2024.04.023 [Google Scholar]

- Zehri F and Zgarni I (2020). Internal and external corporate governance mechanisms and earnings management: An international perspective. Accounting and Management Information Systems, 19(1): 33-64. https://doi.org/10.24818/jamis.2020.01008 [Google Scholar]

- Zgarni I, Hloui K, and Zehri F (2016). Effective audit committee, audit quality and earnings management: Evidence from Tunisia. Journal of Accounting in Emerging Economies, 6(2): 138-155. https://doi.org/10.1108/JAEE-09-2013-0048 [Google Scholar]