International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 4 (April 2025), Pages: 51-61

----------------------------------------------

Original Research Paper

The impact of board structure on accounting information quality in the context of modern accounting systems

Author(s):

Affiliation(s):

Department of Accounting, College of Business, Jouf University, AlJouf, Saudi Arab

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7679-3084

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7679-3084

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.04.007

Abstract

This study examines the relationship between the quality of accounting information and the composition and structure of an organization’s board of directors. Given the importance of accurate and transparent financial reporting for decision-making, the study explores how different board characteristics influence the reliability, relevance, and clarity of accounting data. It also considers how organizational features, industry-specific factors, and regulatory environments may moderate this relationship. A mixed-methods approach is used, combining quantitative analysis of financial data with qualitative insights gathered from surveys or interviews with board members and financial executives. By integrating these methods, the study aims to provide a comprehensive understanding of how board structure impacts accounting information quality. The findings have important implications for corporate governance, regulatory policies, and strategic business decisions. This research offers valuable insights for investors, policymakers, auditors, and company leaders, supporting greater accountability and transparency in financial reporting.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Accounting information quality, Board composition, Corporate governance, Financial reporting, Mixed-methods approach

Article history

Received 1 December 2024, Received in revised form 18 March 2025, Accepted 12 April 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Ethical considerations

This research was conducted in accordance with ethical standards. Participation was voluntary, and informed consent was obtained from all participants prior to their involvement. The survey did not involve the collection of personal or sensitive data, and participant anonymity was preserved throughout.

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Alnor NHA (2025). The impact of board structure on accounting information quality in the context of modern accounting systems. International Journal of Advanced and Applied Sciences, 12(4): 51-61

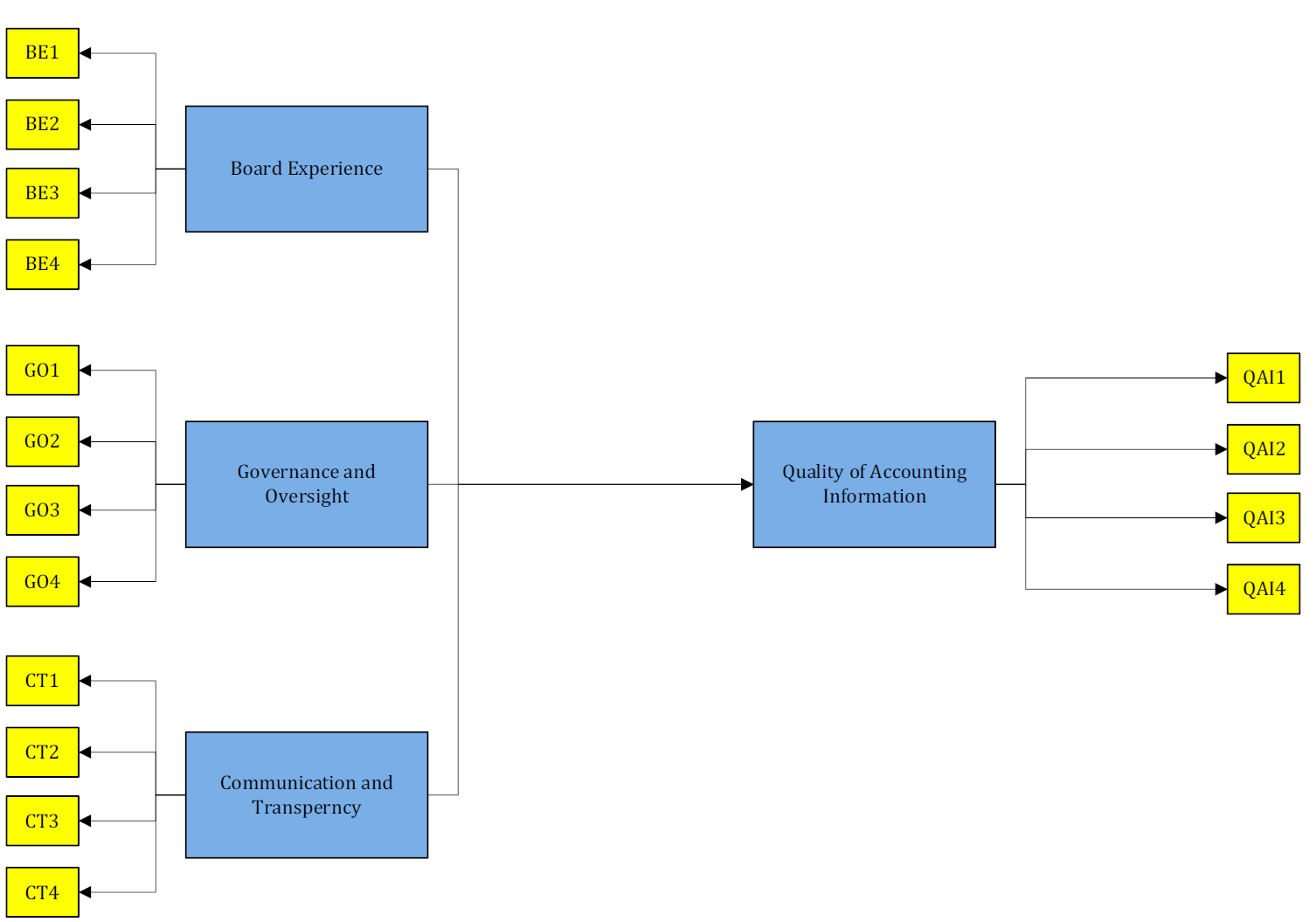

Figures

{kind=link}

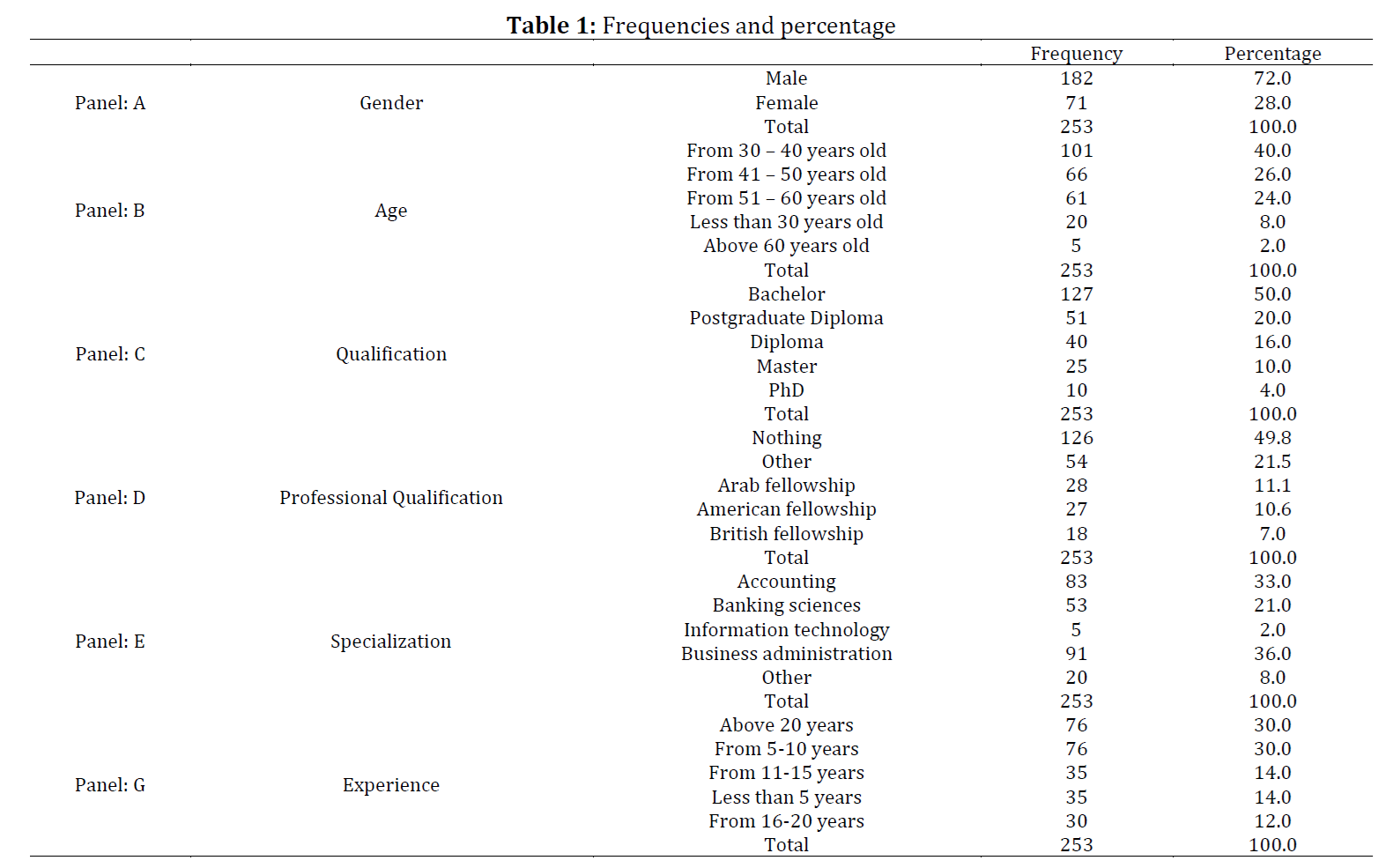

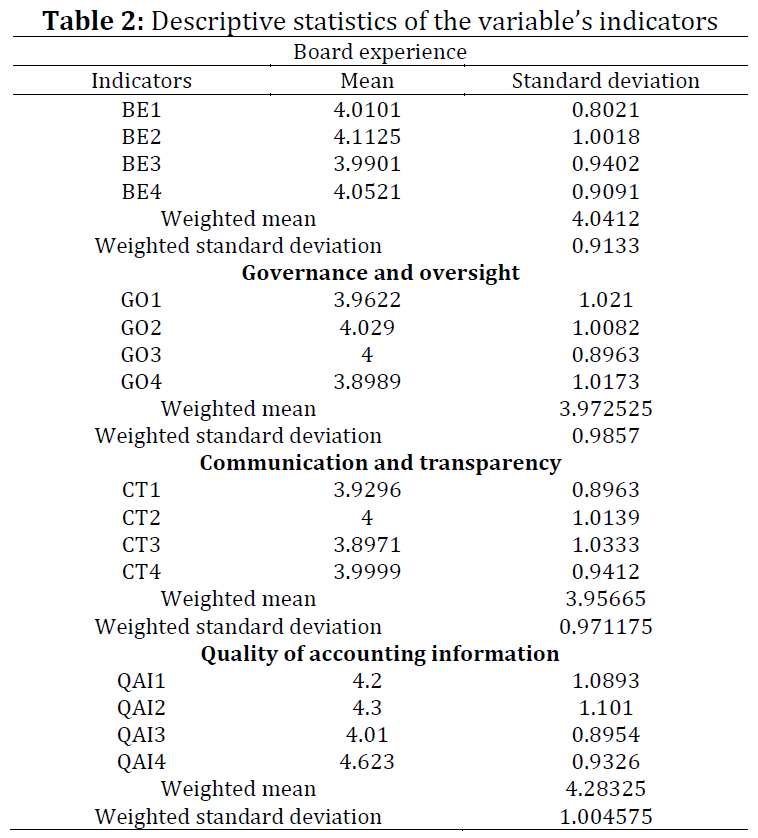

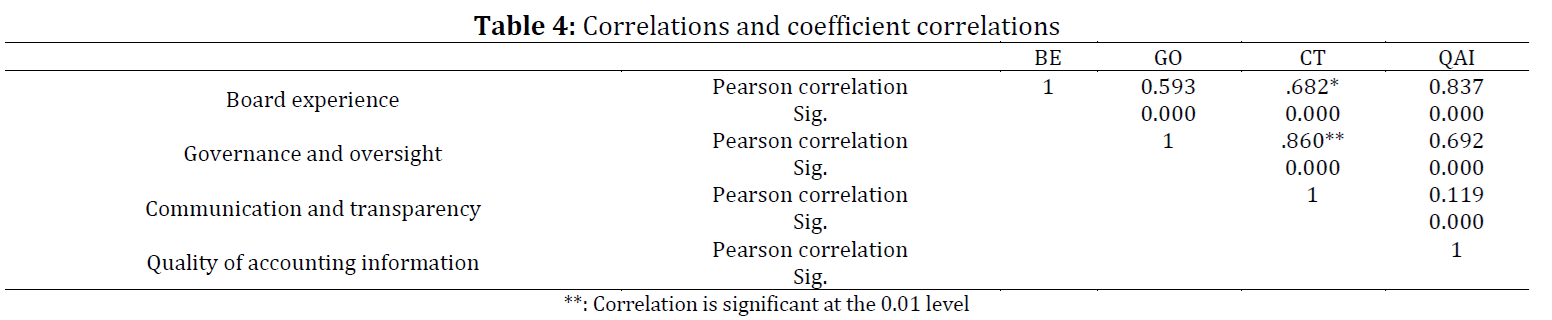

Tables

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (63)

- Abrahams TO, Ewuga SK, Kaggwa S, Uwaoma PU, Hassan AO, and Dawodu SO (2024). Mastering compliance: A comprehensive review of regulatory frameworks in accounting and cybersecurity. Computer Science and IT Research Journal, 5(1): 120-140. https://doi.org/10.51594/csitrj.v5i1.709 [Google Scholar]

- Afolabi A, Ololade BM, and Peters A (2023). Board Attitude towards risk-taking, ownership structure and quality of accounting information of listed insurance companies in Nigeria. Global Journal of Accounting, 9(1): 34-45. https://doi.org/10.54483/sajaar.2023.25.1.1 [Google Scholar]

- Akisik O and Gal G (2017). The impact of corporate social responsibility and internal controls on stakeholders’ view of the firm and financial performance. Sustainability Accounting, Management and Policy Journal, 8(3): 246-280. https://doi.org/10.1108/SAMPJ-06-2015-0044 [Google Scholar]

- Alaoubi A and Almomani MA (2021). The moderating effect for forensic accounting on the relationship between corporate governance and quality of accounting information in the Jordanian public shareholding companies. International Journal of Academic Research in Accounting and Management Sciences, 11(2): 47-61. https://doi.org/10.6007/IJARAFMS/v11-i2/9663 [Google Scholar]

- Alayli S (2023). The impact of accounting information systems on audit quality: The case of Lebanese SMES. Dutch Journal of Finance and Management, 5(2): 22931. https://doi.org/10.55267/djfm/13675 [Google Scholar]

- Al-Htaybat K and von Alberti-Alhtaybat L (2017). Big data and corporate reporting: Impacts and paradoxes. Accounting, Auditing and Accountability Journal, 30(4): 850-873. https://doi.org/10.1108/AAAJ-07-2015-2139 [Google Scholar]

- Alnor NHA (2024a). Corporate governance characteristics and environmental sustainability affect the business performance among listed Saudi company. Sustainability, 16(19): 8436. https://doi.org/10.3390/su16198436 [Google Scholar]

- Alnor NHA (2024b). The effect of developing human capabilities on the company's performance through developing the company's capabilities. WSEAS Transactions on Business and Economics, 21: 95-108. https://doi.org/10.37394/23207.2024.21.9 [Google Scholar]

- Al-Okaily M, Alsmadi AA, Alrawashdeh N, Al-Okaily A, Oroud Y, and Al-Gasaymeh AS (2023). The role of digital accounting transformation in the banking industry sector: An integrated model. Journal of Financial Reporting and Accounting, 22(2): 308-326. https://doi.org/10.1108/JFRA-04-2023-0214 [Google Scholar]

- Alreshidi E, Mourshed M, and Rezgui Y (2017). Factors for effective BIM governance. Journal of Building Engineering, 10: 89-101. https://doi.org/10.1016/j.jobe.2017.02.006 [Google Scholar]

- Alruwaili TF, Al-Matari EM, Mgammal MH, and Alnor NHA (2024). The influence of ownership structure on corporation performance: Evidence from Saudi listed corporations. Business Strategy Review, 5(1): 450-462. https://doi.org/10.22495/cbsrv5i1siart18 [Google Scholar]

- Alsalim M, Amin H, and Youssef A (2018). The role of corporate governance in achieving accounting information quality (Field study in the Mishraq sulfur state Co.). Studies and Scientific Researches, Economics Edition, 27: 21-48. https://doi.org/10.29358/sceco.v0i0.399 [Google Scholar]

- Annarelli A, Nonino F, and Palombi G (2020). Understanding the management of cyber resilient systems. Computers and Industrial Engineering, 149: 106829. https://doi.org/10.1016/j.cie.2020.106829 [Google Scholar]

- Ansong E and Boateng R (2019). Surviving in the digital era–business models of digital enterprises in a developing economy. Digital Policy, Regulation and Governance, 21(2): 164-178. https://doi.org/10.1108/DPRG-08-2018-0046 [Google Scholar]

- Appelbaum D, Kogan A, and Vasarhelyi MA (2017). Big Data and analytics in the modern audit engagement: Research needs. Auditing: A Journal of Practice and Theory, 36(4): 1-27. https://doi.org/10.2308/ajpt-51684 [Google Scholar]

- Appiah KO, Awunyo-Vitor D, Mireku K, and Ahiagbah C (2016). Compliance with international financial reporting standards: The case of listed firms in Ghana. Journal of Financial Reporting and Accounting, 14(1): 131-156. https://doi.org/10.1108/JFRA-01-2015-0003 [Google Scholar]

- Aryani YA and Suhardjanto D (2016). International financial reporting standards, board governance, and accounting quality: A preliminary Indonesian evidence. Asian Review of Accounting, 24(4): 474-497. https://doi.org/10.1108/ARA-06-2014-0064 [Google Scholar]

- Austin AA, Carpenter TD, Christ MH, and Nielson CS (2021). The data analytics journey: Interactions among auditors, managers, regulation, and technology. Contemporary Accounting Research, 38(3): 1888-1924. https://doi.org/10.1111/1911-3846.12680 [Google Scholar]

- Balakrishnan V and Gan CL (2016). Students’ learning styles and their effects on the use of social media technology for learning. Telematics and Informatics, 33(3): 808-821. https://doi.org/10.1016/j.tele.2015.12.004 [Google Scholar]

- Bentley-Goode KA, Newton NJ, and Thompson AM (2017). Business strategy, internal control over financial reporting, and audit reporting quality. Auditing: A Journal of Practice and Theory, 36(4): 49-69. https://doi.org/10.2308/ajpt-51693 [Google Scholar]

- Benzerrouk ZS, Al-Matari EM, Alhebri A, Alnor NHA, Omer AM, and Mohammed OAA (2024). Curricula, strategies, methods, and approaches to accounting education: Evidence from Algerian Universities. International Journal of Sustainable Development and Planning, 19(8): 2851-2860. https://doi.org/10.18280/ijsdp.190804 [Google Scholar]

- Benzerrouk ZS, Alnor NHA, Al-Matari EM, Alhebri A, and Al-Bukhrani MA (2023). The effect of the banking supervision on anti-money laundering. Humanities and Social Sciences Letters, 11(4): 399-415. https://doi.org/10.18488/73.v11i4.3518 [Google Scholar]

- Biermann R and Harsch M (2017). Resource dependence theory. In: Koops J and Biermann R (Eds.), Palgrave handbook of inter-organizational relations in world politics: 135-155. Palgrave Macmillan, London, UK. https://doi.org/10.1057/978-1-137-36039-7_6 [Google Scholar]

- Bose S, Dey SK, and Bhattacharjee S (2023). Big data, data analytics and artificial intelligence in accounting: An overview. In: Akter S and Wamba SF (Eds.). Handbook of big data research methods: 32-51. Edward Elgar, Cheltenham, UK. https://doi.org/10.4337/9781800888555.00007 [Google Scholar]

- Bradley D, Merrifield M, Miller KM, Lomonico S, Wilson JR, and Gleason MG (2019). Opportunities to improve fisheries management through innovative technology and advanced data systems. Fish and Fisheries, 20(3): 564-583. https://doi.org/10.1111/faf.12361 [Google Scholar]

- Camilleri MA (2018). Theoretical insights on integrated reporting: The inclusion of non-financial capitals in corporate disclosures. Corporate Communications: An International Journal, 23(4): 567-581. https://doi.org/10.1108/CCIJ-01-2018-0016 [Google Scholar]

- Cohen J, Krishnamoorthy G, and Wright A (2017). Enterprise risk management and the financial reporting process: The experiences of audit committee members, CFOs, and external auditors. Contemporary Accounting Research, 34(2): 1178-1209. https://doi.org/10.1111/1911-3846.12294 [Google Scholar]

- Cyriac NT and Sadath L (2019). Is cyber security enough-A study on big data security breaches in financial institutions. In 2019 4 th International Conference on Information Systems and Computer Networks, IEEE, Mathura, India: 380-385. https://doi.org/10.1109/ISCON47742.2019.9036294 [Google Scholar]

- Dai J and Vasarhelyi MA (2017). Toward blockchain-based accounting and assurance. Journal of Information Systems, 31(3): 5-21. https://doi.org/10.2308/isys-51804 [Google Scholar]

- Dittes S, Richter S, Richter A, and Smolnik S (2019). Toward the workplace of the future: How organizations can facilitate digital work. Business Horizons, 62(5): 649-661. https://doi.org/10.1016/j.bushor.2019.05.004 [Google Scholar]

- Fenwick M, McCahery JA, and Vermeulen EPM (2019). The end of ‘corporate’ governance: Hello ‘platform’ governance. European Business Organization Law Review, 20: 171-199. https://doi.org/10.1007/s40804-019-00137-z [Google Scholar]

- García‐Sánchez IM, Gómez‐Miranda ME, David F, and Rodríguez‐Ariza L (2019). Analyst coverage and forecast accuracy when CSR reports improve stakeholder engagement: The global reporting initiative‐international finance corporation disclosure strategy. Corporate Social Responsibility and Environmental Management, 26(6): 1392-1406. https://doi.org/10.1002/csr.1755 [Google Scholar]

- García‐Sánchez I-M, Martínez-Ferrero J, and García-Meca E (2017). Gender diversity, financial expertise and its effects on accounting quality. Management Decision, 55(2): 347-382. https://doi.org/10.1108/MD-02-2016-0090 [Google Scholar]

- Ghazal TM, Hasan MK, Alshurideh MT, Alzoubi HM, Ahmad M, Akbar SS, Al Kurdi B, and Akour IA (2021). IoT for smart cities: Machine learning approaches in smart healthcare—A review. Future Internet, 13(8): 218. https://doi.org/10.3390/fi13080218 [Google Scholar]

- Gil M (2025). International online visits on developing the global mindset of accounting and finance students in Mexico. Accounting Education. https://doi.org/10.1080/09639284.2025.2455734 [Google Scholar]

- Gouiaa R and Zéghal D (2014). An analysis of the effect of board characteristics and governance indices on the quality of accounting information. Journal of Governance and Regulation, 3(3): 104-119. https://doi.org/10.22495/jgr_v3_i3_c1_p4 [Google Scholar]

- Grewatsch S and Kleindienst I (2017). When does it pay to be good? Moderators and mediators in the corporate sustainability–corporate financial performance relationship: A critical review. Journal of Business Ethics, 145: 383-416. https://doi.org/10.1007/s10551-015-2852-5 [Google Scholar]

- Gupta D, Khan AA, Kumar A, Baghel MS, and Tiwar A (2024). Socially connected learning harnessing digital platforms for educational engagement. In: Bhatia B and Mushtaq MT (Eds.), Navigating innovative technologies and intelligent systems in modern education: 210-228: IGI Global, Hershy, USA. https://doi.org/10.4018/979-8-3693-5370-7.ch010 [Google Scholar]

- Gupta S, Justy T, Kamboj S, Kumar A, and Kristoffersen E (2021). Big data and firm marketing performance: Findings from knowledge-based view. Technological Forecasting and Social Change, 171: 120986. https://doi.org/10.1016/j.techfore.2021.120986 [Google Scholar]

- Hamza RAEM, Ahmed NH, Mohamed AME, Bennaceur MY, Elhefni AHM, and Elshaabany MM (2024). The impact of artificial intelligence (AI) on the accounting system of Saudi companies. WSEAS Transactions on Business and Economics, 21: 499-511. https://doi.org/10.37394/23207.2024.21.42 [Google Scholar]

- Hutahayan B (2020). The mediating role of human capital and management accounting information system in the relationship between innovation strategy and internal process performance and the impact on corporate financial performance. Benchmarking: An International Journal, 27(4): 1289-1318. https://doi.org/10.1108/BIJ-02-2018-0034 [Google Scholar]

- Jeong Y-C and Kim T-Y (2019). Between legitimacy and efficiency: An institutional theory of corporate giving. Academy of Management Journal, 62(5): 1583-1608. https://doi.org/10.5465/amj.2016.0575 [Google Scholar]

- Joseph J and Gaba V (2020). Organizational structure, information processing, and decision-making: A retrospective and road map for research. Academy of Management Annals, 14(1): 267-302. https://doi.org/10.5465/annals.2017.0103 [Google Scholar]

- Kafi MA and Akter N (2023). Securing financial information in the digital realm: Case studies in cybersecurity for accounting data protection. American Journal of Trade and Policy, 10(1): 15-26. https://doi.org/10.18034/ajtp.v10i1.659 [Google Scholar]

- Kolev KD, Wangrow DB, Barker Iii VL, and Schepker DJ (2019). Board committees in corporate governance: A cross‐disciplinary review and agenda for the future. Journal of Management Studies, 56(6): 1138-1193. https://doi.org/10.1111/joms.12444 [Google Scholar]

- Komal B, Bilal, Ezeani E, Shahzad A, Usman M, and Sun J (2023). Age diversity of audit committee financial experts, ownership structure and earnings management: Evidence from China. International Journal of Finance and Economics, 28(3): 2664-2682. https://doi.org/10.1002/ijfe.2556 [Google Scholar]

- Li T and Tongkong S (2024). Internationalization of enterprises and quality of financial reports in China: Moderating roles of audit committee characteristics. Journal of Infrastructure, Policy and Development, 8(3): 3193. https://doi.org/10.24294/jipd.v8i3.3193 [Google Scholar]

- Löhde ASK, Campopiano G, and Calabrò A (2021). Beyond agency and stewardship theory: Shareholder–manager relationships and governance structures in family firms. Management Decision, 59(2): 390-405. https://doi.org/10.1108/MD-03-2018-0316 [Google Scholar]

- Merendino A, Dibb S, Meadows M, Quinn L, Wilson D, Simkin L, and Canhoto A (2018). Big data, big decisions: The impact of big data on board level decision-making. Journal of Business Research, 93: 67-78. https://doi.org/10.1016/j.jbusres.2018.08.029 [Google Scholar]

- Mohamed AME, Alnor NHA, Mohammed OAA, Al-Matari EM, Alhebri A, and Ahmed A (2024). The impact of information technology governance according to the COBIT on performance. International Journal of Advanced and Applied Sciences, 11(3): 127-136. https://doi.org/10.21833/ijaas.2024.03.014 [Google Scholar]

- Murdock G (2016). Citizens, consumers, and public culture. In: Skovmand M and Schrøder KC (Eds.), Media cultures: 17-41. Routledge, London, UK. https://doi.org/10.4324/9781315511931-3 [Google Scholar]

- Panda B and Leepsa NM (2017). Agency theory: Review of theory and evidence on problems and perspectives. Indian Journal of Corporate Governance, 10(1): 74-95. https://doi.org/10.1177/0974686217701467 [Google Scholar]

- Puthusserry P, Khan Z, Nair SR, and King T (2021). Mitigating psychic distance and enhancing internationalization of fintech SMEs from emerging markets: The role of board of directors. British Journal of Management, 32(4): 1097-1120. https://doi.org/10.1111/1467-8551.12502 [Google Scholar]

- Richins G, Stapleton A, Stratopoulos TC, and Wong C (2017). Big data analytics: Opportunity or threat for the accounting profession? Journal of Information Systems, 31(3): 63-79. https://doi.org/10.2308/isys-51805 [Google Scholar]

- Riyadh HA, Al-Shmam MA, and Ahmed MG (2024). Empirical relationship between board characteristics, earnings management, insolvency risk, and corporate social responsibility. Cogent Business and Management, 11(1): 2321300. https://doi.org/10.1080/23311975.2024.2321300 [Google Scholar]

- Shukla S, George JP, Tiwari K, and Kureethara JV (2022). Data security. In: Shukla S, George JP, Tiwari K, and Kureethara JV (Eds.), Data ethics and challenges: 41-59. Springer, Singapore, Singapore. https://doi.org/10.1007/978-981-19-2211-4 [Google Scholar]

- Singh HP and Alhulail HN (2023). Information technology governance and corporate boards’ relationship with companies’ performance and earnings management: A longitudinal approach. Sustainability, 15(8): 6492. https://doi.org/10.3390/su15086492 [Google Scholar]

- Tran Thanh Thuy N (2025). Effect of accounting information system quality on decision-making success and non-financial performance: Does non-financial information quality matter? Cogent Business and Management, 12(1): 2447913. https://doi.org/10.1080/23311975.2024.2447913 [Google Scholar]

- Vasarhelyi MA, Alles MG, and Kogan A (2018). Principles of analytic monitoring for continuous assurance. In: Chan DY, Chiu V, and Vasarhelyi MA (Eds.), Continuous auditing: Theory and application. 191-217. Emerald Publishing Limited, Bingley, UK. https://doi.org/10.1108/978-1-78743-413-420181009 [Google Scholar]

- Vaske JJ, Beaman J, and Sponarski CC (2017). Rethinking internal consistency in Cronbach's alpha. Leisure Sciences, 39(2): 163-173. https://doi.org/10.1080/01490400.2015.1127189 [Google Scholar]

- Vitolla F, Raimo N, and Rubino M (2020). Board characteristics and integrated reporting quality: An agency theory perspective. Corporate Social Responsibility and Environmental Management, 27(2): 1152-1163. https://doi.org/10.1002/csr.1879 [Google Scholar]

- Vlachopoulou M, Ziakis C, Vergidis K, and Madas M (2021). Analyzing agrifood-tech e-business models. Sustainability, 13(10): 5516. https://doi.org/10.3390/su13105516 [Google Scholar]

- Wolf S (2023). Trusted and open corporate data: Why adoption of the LEI/vLEI is key to enhancing risk management practices in the face of rapid digital transformation. Journal of Risk Management in Financial Institutions, 17(1): 13-21. https://doi.org/10.69554/HWQU2950 [Google Scholar]