International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 11 (November 2025), Pages: 72-81

----------------------------------------------

Original Research Paper

Meta-learning for financial market prediction: An efficient approach with reduced computational cost

Author(s):

Affiliation(s):

Department of Mathematics, NED University of Engineering and Technology, Karachi, Pakistan

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0009-0001-9601-6845

Corresponding author's ORCID profile: https://orcid.org/0009-0001-9601-6845

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.11.008

Abstract

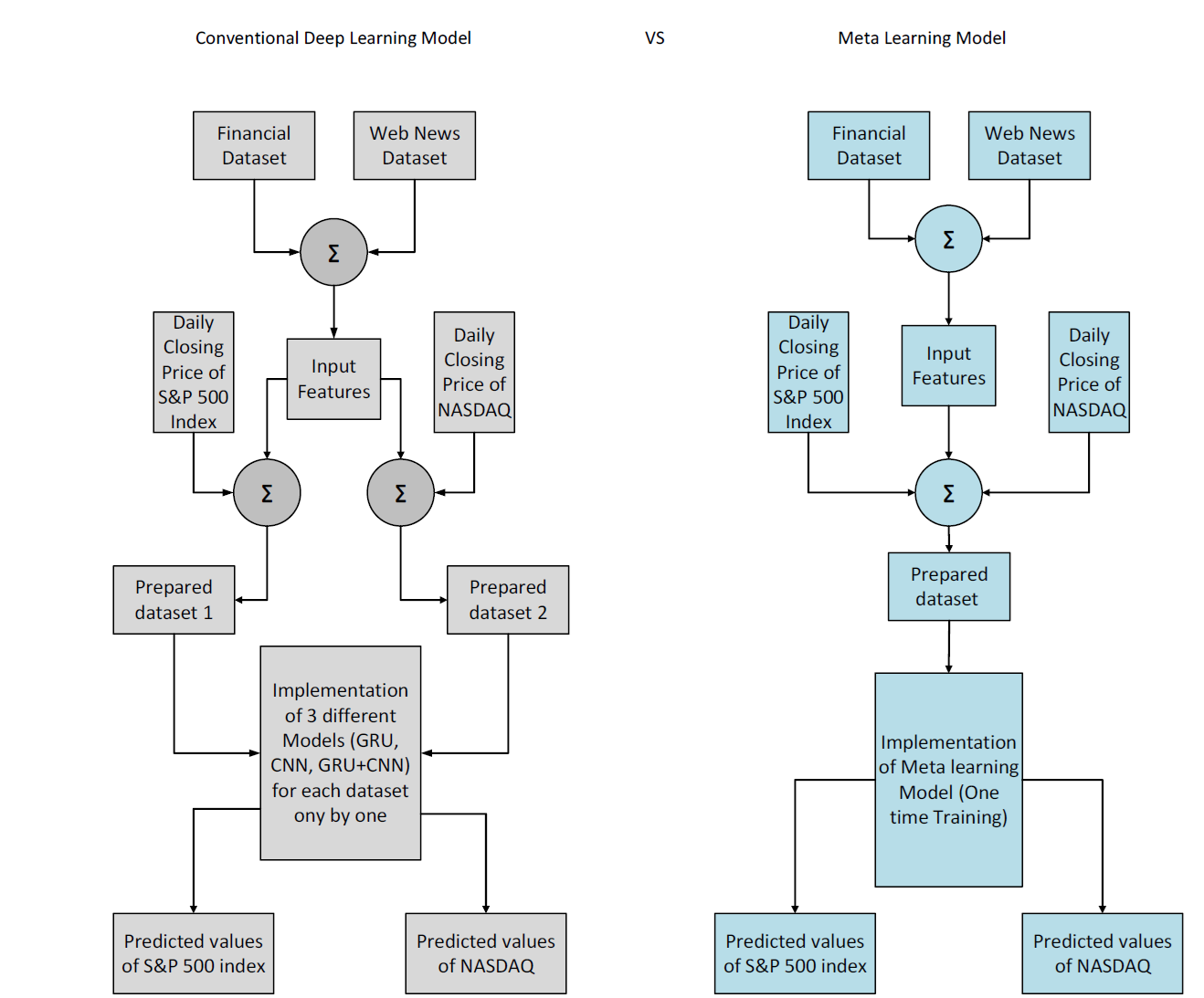

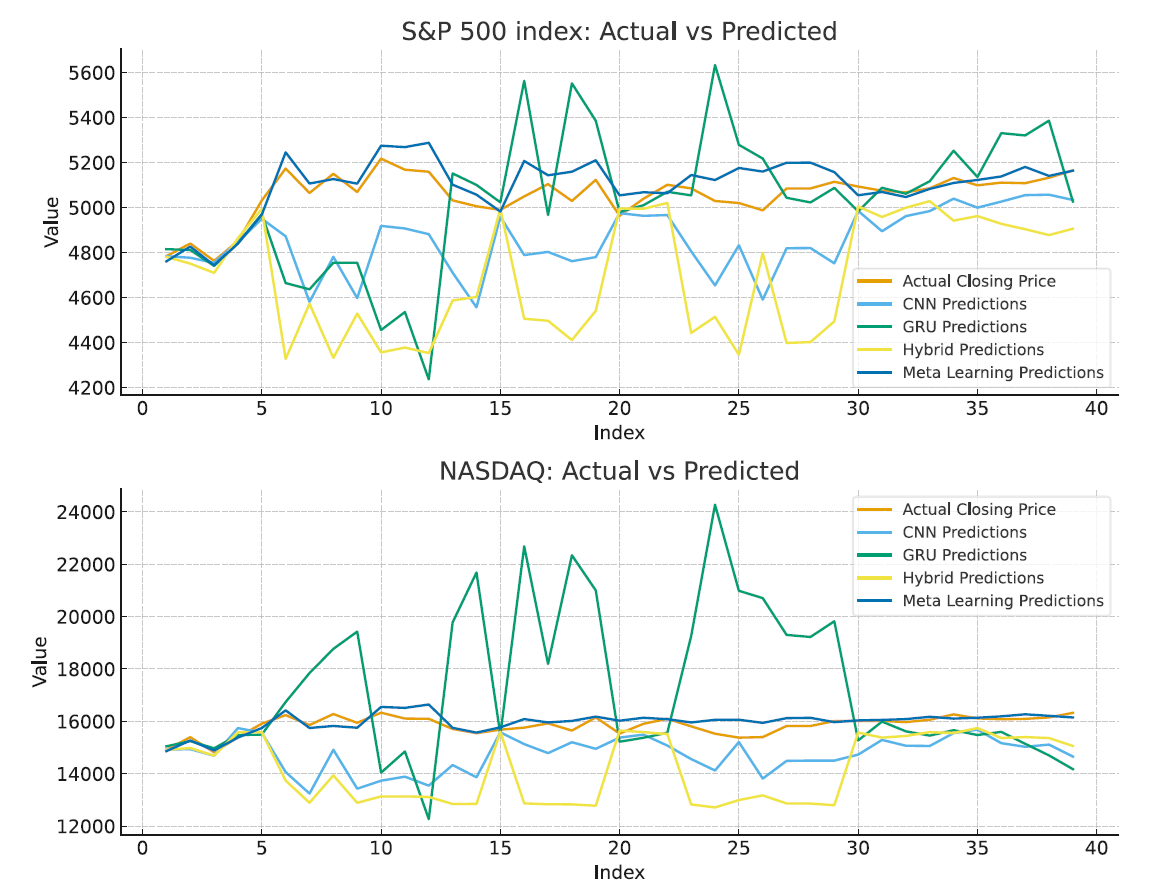

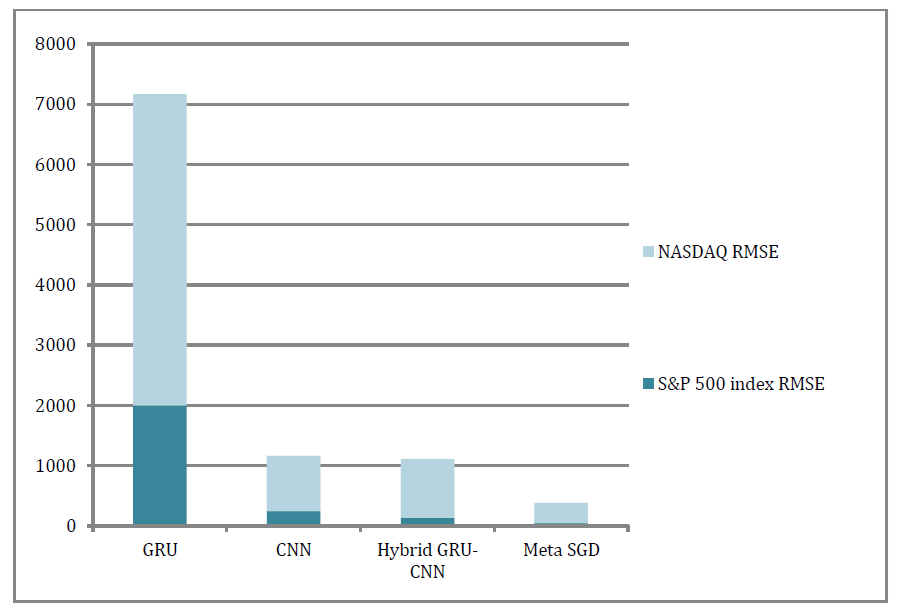

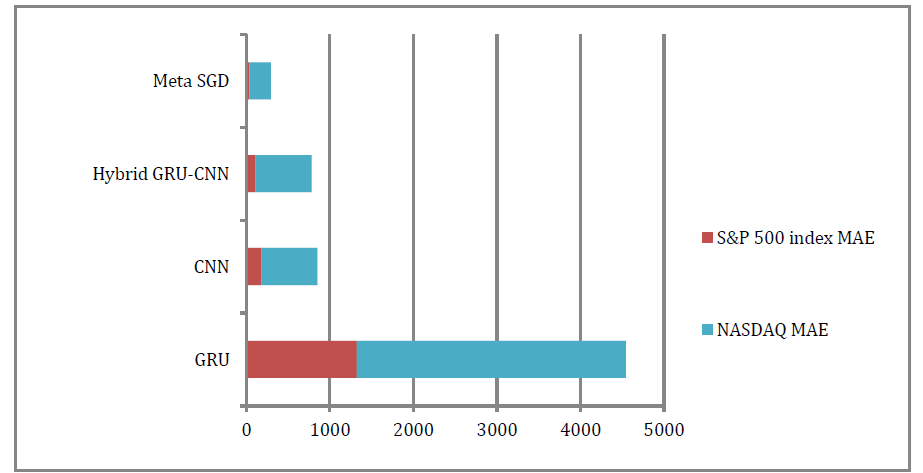

In the era of advanced computational techniques and predictive modeling, the focus has shifted toward reducing latency and minimizing costs. Financial market prediction is not a novel concept, as it has been applied effectively over the past decades to support informed decisions by traders and investors, leading to improved returns. However, machine learning and deep learning models often demand substantial computational power and processing time due to their complex architectures. Meta-learning provides an efficient alternative by reducing computation time and resource requirements for financial forecasting. This study proposes a meta-SGD model to predict future prices of the S&P 500 index and NASDAQ, and compares its performance with deep learning models (CNN and GRU) and a hybrid CNN-GRU model. Evaluation using RMSE, MAE, and R² metrics shows that the meta-learning model outperforms both deep learning and hybrid models, achieving state-of-the-art predictive accuracy with significantly lower computational cost.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Financial market forecasting, Meta-learning, Deep learning, Computational efficiency, Predictive modeling

Article history

Received 30 March 2025, Received in revised form 22 July 2025, Accepted 15 October 2025

Acknowledgment

We would like to acknowledge NED University of Engineering & Technology for providing the research platform and resources.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Batool K, Baig MM, and Fatima U (2025). Meta-learning for financial market prediction: An efficient approach with reduced computational cost. International Journal of Advanced and Applied Sciences, 12(11): 72-81

Figures

Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6 Fig. 7 Fig. 8 Fig. 9 Fig. 10 Fig. 11 Fig. 12 Fig. 13 Fig. 14

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

----------------------------------------------

References (26)

- Ahmed SF, Alam MSB, Hassan M et al. (2023). Deep learning modelling techniques: Current progress, applications, advantages, and challenges. Artificial Intelligence Review, 56: 13521-13617. https://doi.org/10.1007/s10462-023-10466-8 [Google Scholar]

- Al Mamun A, Hossain MS, Rishad SSI (2024). Machine learning for stock market security measurement: A comparative analysis of supervised, unsupervised, and deep learning models. The American Journal of Engineering and Technology, 6(11): 63-76. https://doi.org/10.37547/tajet/Volume06Issue11-08 [Google Scholar]

- Arashi M and Rounaghi MM (2022). Analysis of market efficiency and fractal feature of NASDAQ stock exchange: Time series modeling and forecasting of stock index using ARMA-GARCH model. Future Business Journal, 8: 14. https://doi.org/10.1186/s43093-022-00125-9 [Google Scholar]

- Batool K, Ahmed MF, and Ismail MA (2022). A hybrid model of machine learning model and econometrics' model to predict volatility of KSE-100 Index. Reviews of Management Sciences, 4(1): 225-239. https://doi.org/10.53909/rms.04.01.0125 [Google Scholar]

- Batool K, Fatima U, and Ahmed MF (2025). Trend prediction of DJIA index based on news extraction from Yahoo Finance. International Journal of Computer Applications, 975: 8887. https://doi.org/10.5120/ijca2025924379 [Google Scholar]

- Bhandari HN, Rimal B, Pokhrel NR, Rimal R, Dahal KR, and Khatri RK (2022). Predicting stock market index using LSTM. Machine Learning with Applications, 9: 100320. https://doi.org/10.1016/j.mlwa.2022.100320 [Google Scholar]

- Chauhan JK, Ahmed T, and Sinha A (2025). A novel deep learning model for stock market prediction using a sentiment analysis system from authoritative financial website's data. Connection Science, 37(1): 2455070. https://doi.org/10.1080/09540091.2025.2455070 [Google Scholar]

- Fatima U, Hina S, and Wasif M (2025). Analysis of community groups in large dynamic social network graphs through fuzzy computation. Systems and Soft Computing, 7: 200239. https://doi.org/10.1016/j.sasc.2025.200239 [Google Scholar]

- Fernández C, Salinas L, and Torres CE (2019). A meta extreme learning machine method for forecasting financial time series. Applied Intelligence, 49: 532-554. https://doi.org/10.1007/s10489-018-1282-3 [Google Scholar]

- Fraz TR, Fatima S, and Uddin M (2022). Comparing the forecast performance of nonlinear models and machine learning process: An empirical evaluation of GARCH family and NAR models in the light of CPEC. International Journal of Computational Intelligence in Control, 14(1): 163-172. [Google Scholar]

- Gorenc Novak M and Velušček D (2016). Prediction of stock price movement based on daily high prices. Quantitative Finance, 16(5): 793-826. https://doi.org/10.1080/14697688.2015.1070960 [Google Scholar]

- Hung BT, Chakrabarti P, and Chatterjee P (2023). Stock prediction using multi deep learning algorithms. In: Kautish S, Chatterjee P, Pamucar D, Pradeep N, and Singh D (Eds.), Computational intelligence for modern business systems: Emerging applications and strategies: 97-113. Springer, Singapore, Singapore. https://doi.org/10.1007/978-981-99-5354-7_6 [Google Scholar] PMCid:PMC11046495

- Huy DTN and Hang NT (2021). Factors that affect stock price and beta CAPM of Vietnam banks and enhancing management information system–case of Asia Commercial Bank. Revista Geintec-Gestao Inovacao E Tecnologias, 11(2): 302-308. https://doi.org/10.47059/revistageintec.v11i2.1667 [Google Scholar]

- Jain D, Mittal SK, and Choudhary V (2022). Modeling stock market return volatility: GARCH evidence from Nifty Realty Index. Finance India, 36(1): 159-169. [Google Scholar]

- Magner NS, Lavin JF, Valle MA, and Hardy N (2020). The volatility forecasting power of financial network analysis. Complexity, 2020: 7051402. https://doi.org/10.1155/2020/7051402 [Google Scholar]

- Marszałek A and Burczyński T (2014). Modeling and forecasting financial time series with ordered fuzzy candlesticks. Information Sciences, 273: 144-155. https://doi.org/10.1016/j.ins.2014.03.026 [Google Scholar]

- Masalegou SMB, Kazemie MAA, Monfared JH, and Rezaeian A (2022). A stock market prediction model based on deep learning networks. Journal of System Management, 8(4): 1-17. https://doi.org/10.30495/jsm.2022.1954072.1623 [Google Scholar]

- Mattera R and Otto P (2024). Network log-ARCH models for forecasting stock market volatility. International Journal of Forecasting, 40(4): 1539-1555. https://doi.org/10.1016/j.ijforecast.2024.01.002 [Google Scholar]

- Noor K and Fatima U (2024). Meta learning strategies for comparative and efficient adaptation to financial datasets. IEEE Access, 13: 24158-24170. https://doi.org/10.1109/ACCESS.2024.3516490 [Google Scholar]

- Padma AP and Mishra AK (2022). Forecasting on stock market time series data using data mining techniques. Dogo Rangsang Research Journal, 9(1): 351-358. [Google Scholar]

- Samarawickrama AJP and Fernando TGI (2017). A recurrent neural network approach in predicting daily stock prices an application to the Sri Lankan stock market. In the International Conference on Industrial and Information Systems, IEEE, Peradeniya, Sri Lanka: 1-6. https://doi.org/10.1109/ICIINFS.2017.8300345 [Google Scholar]

- Santara A, Naik A, Sheet D, Ghosh P, Mitra P, and Das N (2017). MESA: Meta learning for stochastic asset management. In the 26th International Joint Conference on Artificial Intelligence, Melbourne, Australia: 1-16. [Google Scholar]

- Steinbacher M, Steinbacher M, and Steinbacher M (2025). Using CNN to model stock prices. Computational Economics. https://doi.org/10.1007/s10614-025-10887-3 [Google Scholar]

- Tian Y, Zhao X, and Huang W (2022). Meta-learning approaches for learning-to-learn in deep learning: A survey. Neurocomputing, 494: 203-223. https://doi.org/10.1016/j.neucom.2022.04.078 [Google Scholar]

- Xiang H, Lin J, Chen CH, and Kong Y (2020). Asymptotic meta learning for cross validation of models for financial data. IEEE Intelligent Systems, 35(2): 16-24. https://doi.org/10.1109/MIS.2020.2973255 [Google Scholar]

- Zhao Q, Hao Y, and Li X (2024). Stock price prediction based on hybrid CNN-LSTM model. Applied and Computational Engineering, 104: 110-115. https://doi.org/10.54254/2755-2721/104/20241065 [Google Scholar]