International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 12, Issue 10 (October 2025), Pages: 81-87

----------------------------------------------

Original Research Paper

The effect of legal entropy on value-added tax in Mexico, 1978–2023

Author(s):

Affiliation(s):

1Facultad de Ciencias Económicas y Empresariales, Universidad Panamericana, Ciudad de México, México

2Facultad de Economía y Negocios, Universidad Anáhuac México, Huixquilucan, México

3Subdirección de Posgrado e Investigación, Instituto Tecnológico Superior de Tantoyuca, Tecnológico Nacional de México, Veracruz, México

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-4713-5116

Corresponding author's ORCID profile: https://orcid.org/0000-0003-4713-5116

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2025.10.010

Abstract

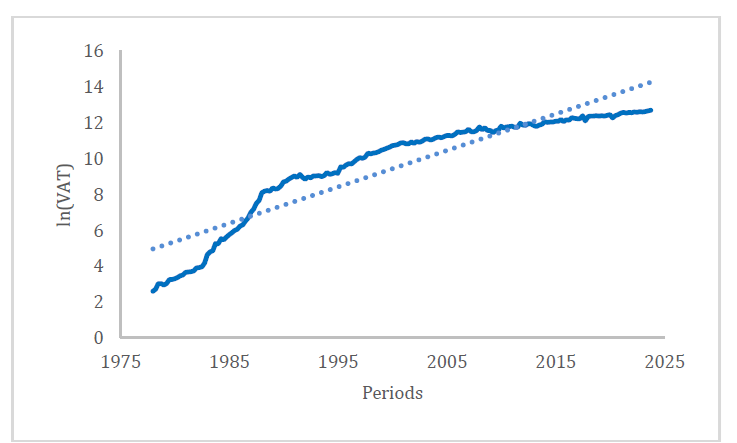

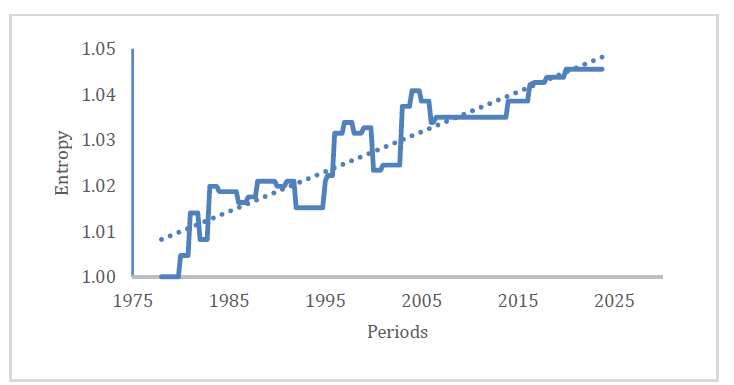

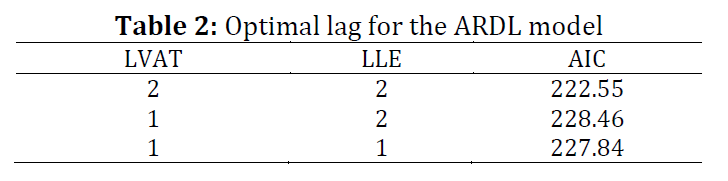

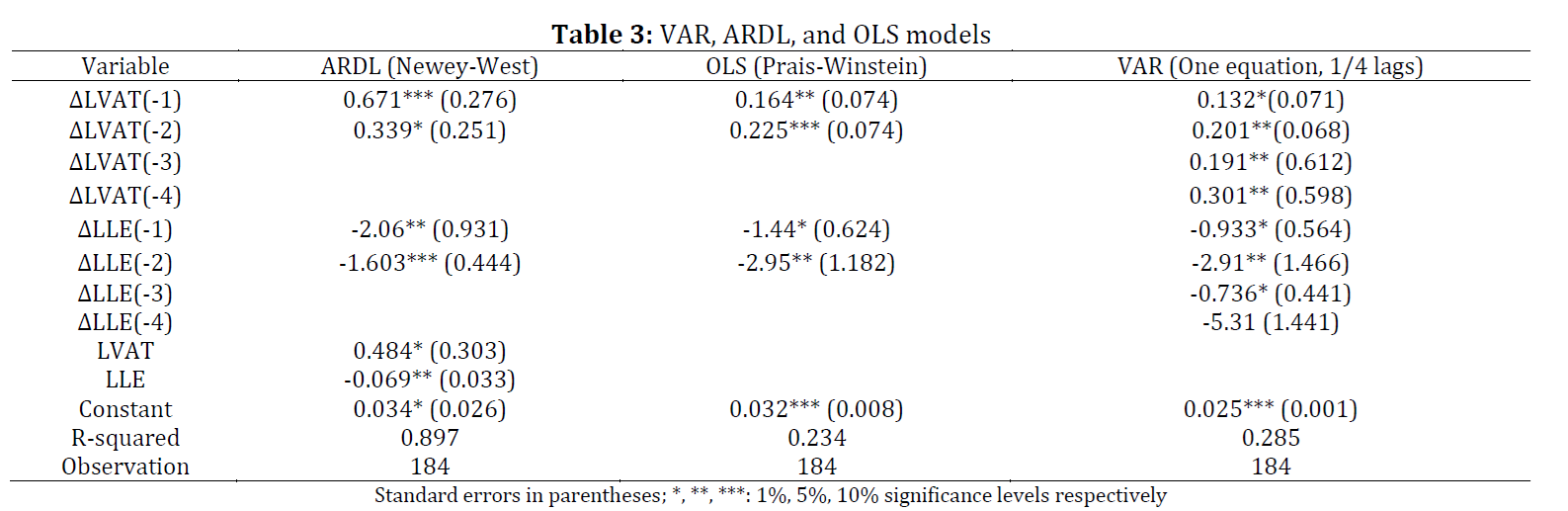

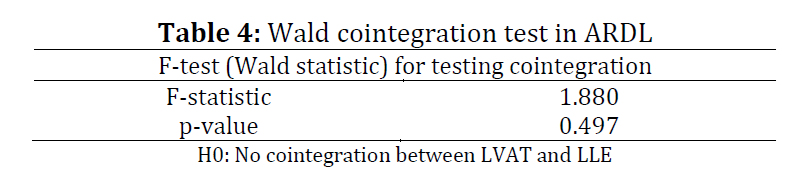

This study investigates the relationship between legal entropy (LE) and value-added tax (VAT) in Mexico. Legal entropy is considered a measure of uncertainty or instability within the legal framework, which may influence tax collection and government revenues. To explore this relationship, the study employs a causality approach combined with an autoregressive distributed lag (ARDL) model to assess both short-term and long-term dynamics. The results indicate a unidirectional causal link running from LE to VAT, suggesting that changes in legal uncertainty directly affect tax performance. However, no long-run cointegration is found between the two variables, implying the absence of a stable equilibrium relationship over time. In the short term, a one percent increase in the entropy index is estimated to reduce VAT revenue by approximately 2.06 percent. These findings highlight the potential risks posed by legal uncertainty for fiscal stability and effective tax policy.

© 2025 The Authors. Published by IASE.

This is an

Keywords

Legal entropy, Value-added tax, Granger causality, ARDL model, Cointegration

Article history

Received 12 April 2025, Received in revised form 12 September 2025, Accepted 19 September 2025

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Moreno J, Mata L, and Beltrán JH (2025). The effect of legal entropy on value-added tax in Mexico, 1978–2023. International Journal of Advanced and Applied Sciences, 12(10): 81-87

Figures

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (25)

- Artzner P, Delbaen F, Eber JM, and Heath D (1999). Coherent measures of risk. Mathematical Finance, 9: 203–228. https://doi.org/10.1111/1467-9965.00068 [Google Scholar]

- Bacallao J, Castillo-Salgado C, Schneider MC, Mujica OJ, Loyola E, and Manuel V (2002). Índices para medir las desigualdades de salud de carácter social basados en la noción de entropía. Revista Panamericana de Salud Pública, 12(6): 429–435. https://doi.org/10.1590/S1020-49892002001200008 [Google Scholar]

- Bejarano JLP, Bejarano JCP, and Carranza AR (2023). Analysis of the behavior of the flow of prices in the financial market using the entropy of information. Selecciones Matemáticas, 10(1): 164–172. https://doi.org/10.17268/sel.mat.2023.01.15 [Google Scholar]

- Bourcier D and Mazzega P (2007). Toward measures of complexity in legal systems. In the Proceedings of the 11th International Conference on Artificial Intelligence and Law, Association for Computing Machinery, Stanford, USA: 211–215. https://doi.org/10.1145/1276318.1276359 [Google Scholar]

- Calero MP (2019). Entropy in macroeconomic models: Another perspective of production function. REICE: Revista Electrónica De Investigación En Ciencias Económicas, 7(14): 77-86. https://doi.org/10.5377/reice.v7i14.9375 [Google Scholar]

- Devi S (2019). Financial portfolios based on Tsallis relative entropy as the risk measure. Journal of Statistical Mechanics: Theory and Experiment, 2019: 093207. https://doi.org/10.1088/1742-5468/ab3bc5 [Google Scholar]

- Epstein RA (1996). Simple rules for a complex world. Harvard University Press, Cambridge, USA. https://doi.org/10.4159/9780674036567 [Google Scholar]

- Escola B, Palma MJ, González S, and Ávalos E (2021). La sostenibilidad en el Ecuador a través de un análisis multicriterio basado en entropía, durante el período 2008-2015 [Sustainability in Ecuador by means of a multicriteria analysis based on entropy, period 2008–2015]. Revista Politécnica, 47(2): 17–26. https://doi.org/10.33333/rp.vol47n2.02 [Google Scholar]

- Espinosa JM and Alvarez AC (2022). Artificial intelligence and its application in the study of the legal complexity of the Value Added Tax Act in Mexico. In: Mora JAN and Aragón MBM (Eds.), Data analytics applications in emerging markets: 177–202. Springer, Singapore, Singapore. https://doi.org/10.1007/978-981-19-4695-0_9 [Google Scholar]

- García RS, Cruz S, and Venegas-Martínez F (2014). Una medida de eficiencia de mercado. Un enfoque de teoría de la información [A market efficiency measurement. An information theory approach]. Contaduría y Administración, 59(4): 137–166. https://doi.org/10.1016/S0186-1042(14)70158-5 [Google Scholar]

- Givati Y (2009). Resolving legal uncertainty: The fulfilled promise of advance tax rulings. Virginia Tax Review 29: 137–175. [Google Scholar]

- Kades E (1997). The laws of complexity and the complexity of law: The implications of computational complexity theory for the law. Rutgers Law Review, 49(2): 403–484. [Google Scholar]

- Katz DM and Bommarito MJ (2014). Measuring the complexity of the law: The United States code. Artificial Intelligence and Law, 22: 337–374. https://doi.org/10.1007/s10506-014-9160-8 [Google Scholar]

- Lassance N and Vrins F (2021). Minimum Rényi entropy portfolios. Annals of Operations Research, 299: 23–46. https://doi.org/10.1007/s10479-019-03364-2 [Google Scholar]

- Long SB and Swingen JA (1987). An approach to the measurement of tax law complexity. Journal of the American Taxation Association, 8(2): 22–36. [Google Scholar]

- Miguel-Velasco AE, Maldonado-Cruz P, Torres-Valdéz JC, and Cruz-Atayde M (2008). La entropía como indicador de las desigualdades regionales en México [Entropy as a regional inequality indicator in Mexico]. Economía, Sociedad y Territorio, 8(27): 693–719. https://doi.org/10.22136/est002008201 [Google Scholar]

- Moreno Espinosa J, Beltrán Godoy JH, and Mata Mata L (2020). Efecto del crecimiento económico y de la complejidad legal sobre el impuesto al valor agregado [Effect of economic growth and legal complexity on the value added tax]. Contaduría y Administración, 65(4): 1-27. https://doi.org/10.22201/fca.24488410e.2020.2230 [Google Scholar]

- Panapoulou E and Pittis N (2004). A comparison of autoregressive distributed lag and dynamic OLS cointegration estimators in the case of a serially correlated cointegration error. The Econometrics Journal, 7(2): 585–617. https://doi.org/10.1111/j.1368-423X.2004.00145.x [Google Scholar]

- Pesaran MH, Shin Y, and Smith RJ (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16: 289–326. https://doi.org/10.1002/jae.616 [Google Scholar]

- Rivas ODM (2014). Estimated diversification level of exports in Nicaragua. Revista Electrónica de Investigación en Ciencias Económicas, 2(4): 1–13. https://doi.org/10.5377/reice.v2i4.1721 [Google Scholar]

- Ruhl JB and Katz DM (2015). Measuring, monitoring, and managing legal complexity. Iowa Law Review, 101(1): 191-244. [Google Scholar]

- Schuck PH (1992). Legal complexity: Some causes, consequences, and cures. Duke Law Journal, 42(1): 1–52. https://doi.org/10.2307/1372753 [Google Scholar]

- Shannon CE (1948). A mathematical theory of communication. The Bell System Technical Journal, 27(3): 379–423. https://doi.org/10.1002/j.1538-7305.1948.tb01338.x [Google Scholar]

- Toda HY and Yamamoto T (1995). Statistical inference in vector autoregressions with possibly integrated processes. Journal of Econometrics, 66(1-2): 225–250. https://doi.org/10.1016/0304-4076(94)01616-8 [Google Scholar]

- Waltl B and Matthes F (2014). Towards measures of complexity: Applying structural and linguistic metrics to German laws. In the Jurix: International conference on legal knowledge and information systems, Krakow, Poland: 153–162. [Google Scholar]