International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 11, Issue 1 (January 2024), Pages: 56-67

----------------------------------------------

Original Research Paper

Exploring the impact of digital accounting and digital zakat on improving business sustainability in the Middle East and Malaysia

Author(s):

Affiliation(s):

1Department of Customs and Tax Sciences, Jadara University, Irbid, Jordan

2Faculty of Economics and Muamalat (FEM), Universiti Sains Islam Malaysia (USIM), Nilai, Malaysia

3Graduate School of Business, Universiti Kebangsaan Malaysia, Bangi, Malaysia

4Faculty of Business, Amman Arab University, Amman, Jordan

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0746-912X

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0746-912X

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2024.01.007

Abstract

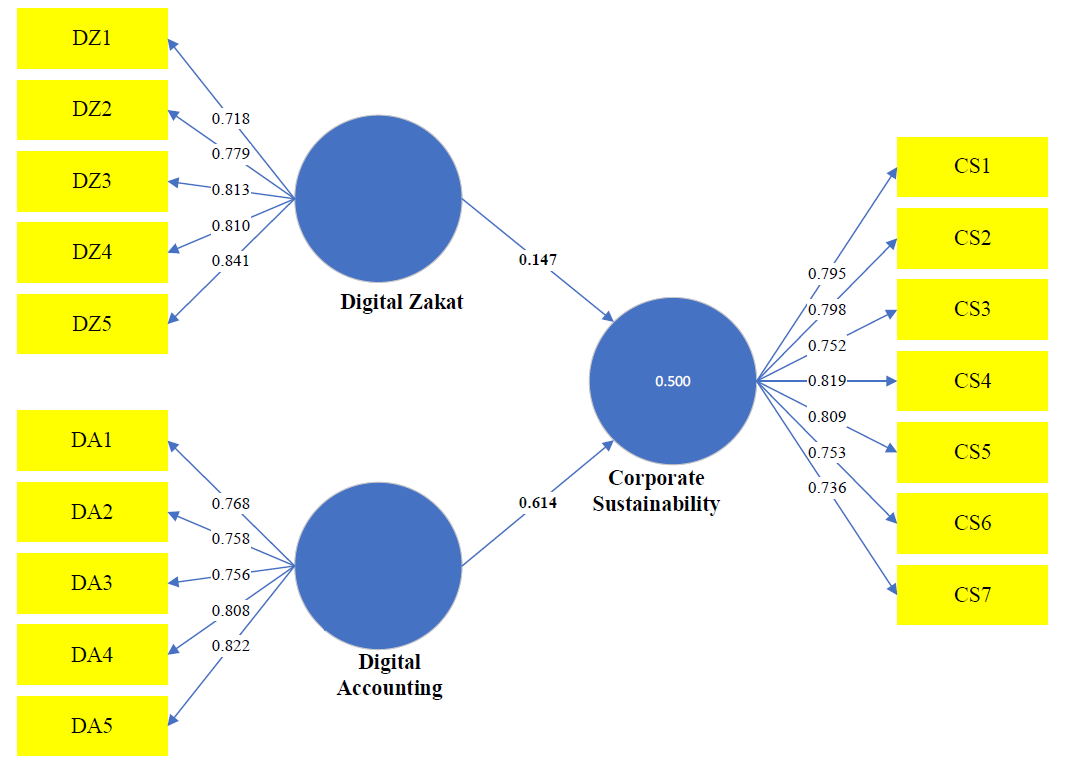

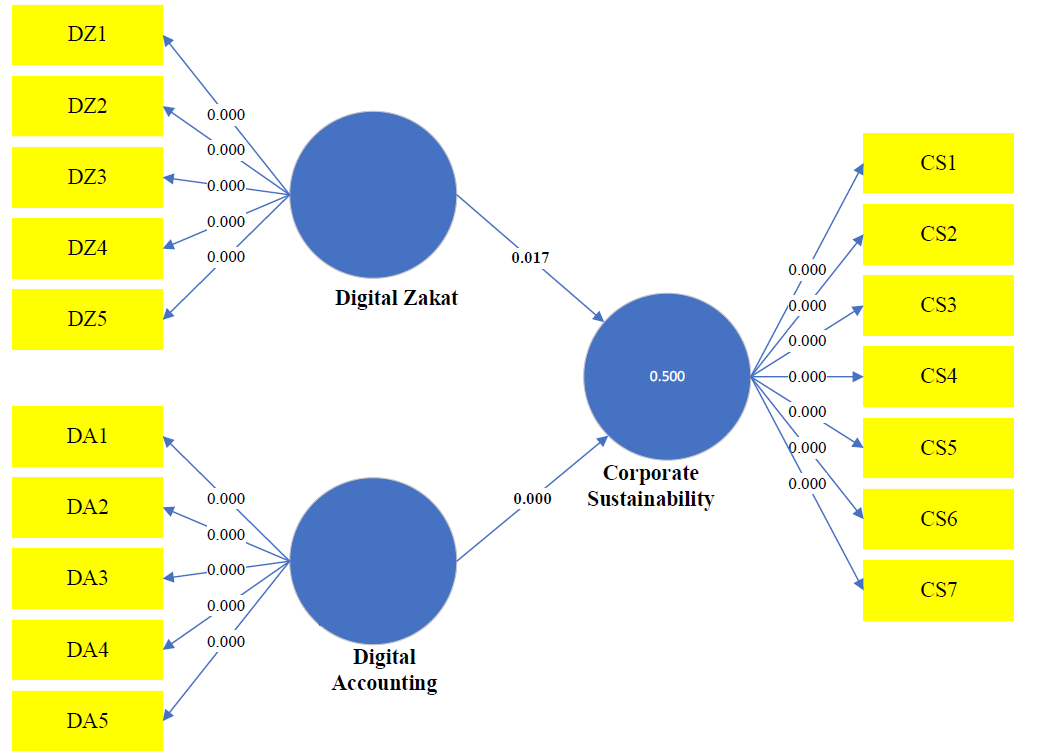

This paper seeks to explore the potential of digital accounting and digital zakat in enhancing corporate sustainability. It primarily examines the role of these digital modalities in enhancing philanthropic contributions, improving financial transparency, and achieving sustainability goals. The study explores the synergistic effects of combining digital accounting and digital zakat, and aims to fill the knowledge gap regarding their collective impact on sustainable business practices. The results confirm the primary hypothesis and show a positive correlation with corporate sustainability. Consistent with previous research, digital zakat is identified as a catalyst for stakeholder engagement and a facilitator of sustainable development initiatives. Similarly, digital accounting is associated with increased financial transparency, thereby strengthening corporate sustainability efforts. These findings underscore the need for further exploration and integration into corporate strategies and highlight the prospects of digital technology in strengthening corporate sustainability. The study provides strategic recommendations for businesses, policymakers, and academics to promote sustainable practices and align financial systems with broader sustainability goals. This research is central to deepening the understanding of digital technologies' ability to enhance sustainability in business contexts, and future studies should extend these findings to examine the complex dynamics of how digital solutions can optimize sustainability in different sectors and settings.

© 2023 The Authors. Published by IASE.

This is an

Keywords

Digital accounting, Digital zakat, Corporate sustainability, SmartPLS 4

Article history

Received 11 September 2023, Received in revised form 20 December 2023, Accepted 23 December 2023

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Al-Taani AHM, Al-Zaqeba MAA, Maabreh HMA, and Jarah BAF (2024). Exploring the impact of digital accounting and digital zakat on improving business sustainability in the Middle East and Malaysia. International Journal of Advanced and Applied Sciences, 11(1): 56-67

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

{kind=link}

----------------------------------------------

References (59)

- Ababneh A, Almarashdah M, Jebril I, Al-Zaqeba M, and Assaf N (2023). Driving sustainable supply chains: Blockchain-enabled eco-efficiency for resilient customs ports. Uncertain Supply Chain Management, 11(4): 1719-1734. https://doi.org/10.5267/j.uscm.2023.6.018 [Google Scholar]

- Abdalla AAM, Aljheme ED, and Abdulhadi FAG (2022). The impact of using visual materials in enhancing learning English vocabulary at Libyan preparatory schools. Al-Zaytoonah University of Jordan Journal for Human and Social Studies, 3(1): 217-229. [Google Scholar]

- Adomako S and Tran MD (2023). Beyond profits: The linkages between local embeddedness, social legitimacy, and corporate philanthropy in the mining industry. Corporate Social Responsibility and Environmental Management, 31(1): 555-565. https://doi.org/10.1002/csr.2585 [Google Scholar]

- Ajina AS, Roy S, Nguyen B, Japutra A, and Al-Hajla AH (2020). Enhancing brand value using corporate social responsibility initiatives: Evidence from financial services brands in Saudi Arabia. Qualitative Market Research: An International Journal, 23(4): 575-602. https://doi.org/10.1108/QMR-11-2017-0145 [Google Scholar]

- Ajmal S, Muzammil MB, Shoaib M, and Mehmood MH (2023). Empowering donors: How blockchain technology can help ensure their contributions reach the right recipients. In the International Conference on Business Analytics for Technology and Security, IEEE, Dubai, UAE: 1-6. https://doi.org/10.1109/ICBATS57792.2023.10111126 [Google Scholar]

- Akinlabi HA and Habeebullah AA (2022). Implementation of zakat collection and distribution system in Ibadan metropolis using WordPress core architecture and architectonics. Fountain Journal of Natural and Applied Sciences, 11(1): 22-28. https://doi.org/10.53704/fujnas.v11i1.444 [Google Scholar]

- Alam A, Ratnasari RT, Ryandono MN, Prasetyo A, Santosa IW, and Bafana FA (2023). Systematic literature review on Malaysia zakat studies (2011-2023). Multidisciplinary Reviews, 6(4): 2023044. https://doi.org/10.31893/multirev.2023044 [Google Scholar]

- Alattass MI (2023). The impact of digital evolution and FinTech on banking performance: A cross-country analysis. International Journal of Advanced and Applied Sciences, 10(8): 71-77. https://doi.org/10.21833/ijaas.2023.08.008 [Google Scholar]

- Alflaieh M (2022). Electronic Fraud in the context of e-commerce under Jordanian legislation. Al-Zaytoonah University of Jordan Journal for Legal Studies, 3(3): 67-82. https://doi.org/10.15849/ZUJJLS.221130.04 [Google Scholar]

- Ali IM, Jusoh YY, Abdullah R, and Ahmed YA (2023). Exploring the performance measures of big data analytics systems. International Journal of Advanced and Applied Sciences, 10(1): 92-104. https://doi.org/10.21833/ijaas.2023.01.013 [Google Scholar]

- Allah Pitchay A (2022). Factors influence intention of management of Shariah-compliant companies to participate in Islamic voluntary charity. International Journal of Islamic and Middle Eastern Finance and Management, 15(5): 967-985. https://doi.org/10.1108/IMEFM-11-2019-0466 [Google Scholar]

- Al-Malkawi HAN and Javaid S (2018). Corporate social responsibility and financial performance in Saudi Arabia: Evidence from zakat contribution. Managerial Finance, 44(6): 648-664. https://doi.org/10.1108/MF-12-2016-0366 [Google Scholar]

- Almatarneh Z, Ineizeh N, Jarah B, and Al-Zaqeba M (2022). The relationship between corporate social responsibility accounting and supply chain management. Uncertain Supply Chain Management, 10(4): 1421-1426. https://doi.org/10.5267/j.uscm.2022.6.014 [Google Scholar]

- Al-Okaily M, Alsmadi AA, Alrawashdeh N, Al-Okaily A, Oroud Y, and Al-Gasaymeh AS (2023). The role of digital accounting transformation in the banking industry sector: An integrated model. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-04-2023-0214 [Google Scholar]

- Alsaqri SH, Albaqawi HM, and Alkwiese MJ (2018). Strategies for improving patient fulfilment with quality of nursing care in northwestern hospitals of Saudi Arabia. International Journal of Advanced and Applied Sciences, 5(7): 123-130. https://doi.org/10.21833/ijaas.2018.07.015 [Google Scholar]

- Alsharari NM and Ikem F (2023). Digital accounting systems and information technology in the public sector: Mutual interaction. Journal of Systems and Information Technology, 25(1): 53-73. https://doi.org/10.1108/JSIT-09-2021-0190 [Google Scholar]

- Al-Zaqeba MAA and Al-Rashdan MT (2020). Extension of the TPB in tax compliance behavior: The role of moral intensity and customs tax. International Journal of Scientific and Technology Research, 9(4): 227-232. [Google Scholar]

- Al-Zaqeba MAA, Abdul Hamid S, Ineizeh NI, Hussein OJ, and Albawwat AH (2022). The effect of corporate governance mechanisms on earnings management in Malaysian manufacturing companies. Asian Economic and Financial Review, 12(5): 354–367. https://doi.org/10.55493/5002.v12i5.4490 [Google Scholar]

- Al-Zaqeba MAA, Shubailat OM, Abdul Hamid S, Jarah BAF, Ababneh FAT, and Almatarneh Z (2023). The influence of board of directors’ characteristics on corporate social responsibility disclosures in Jordanian Islamic banks. International Journal of Advanced and Applied Sciences, 10(11): 1-13. https://doi.org/10.21833/ijaas.2023.11.001 [Google Scholar]

- Alzaqebah M and Abdullah S (2015). Hybrid bee colony optimization for examination timetabling problems. Computers and Operations Research, 54: 142-154. https://doi.org/10.1016/j.cor.2014.09.005 [Google Scholar]

- Alzaqebah M, Alrefai N, Ahmed EA, Jawarneh S, and Alsmadi MK (2020). Neighborhood search methods with moth optimization algorithm as a wrapper method for feature selection problems. International Journal of Electrical and Computer Engineering (2088-8708), 10(4): 3672-3684. https://doi.org/10.11591/ijece.v10i4.pp3672-3684 [Google Scholar]

- Alzaqebah M, Jawarneh S, Mohammad RMA, Alsmadi MK, Al-Marashdeh I, Ahmed EA, and Alghamdi FA (2021). Hybrid feature selection method based on particle swarm optimization and adaptive local search method. International Journal of Electrical and Computer Engineering, 11(3): 2414- 2422. https://doi.org/10.11591/ijece.v11i3.pp2414-2422 [Google Scholar]

- Arens AA, Elder RJ, and Beasley MS (2012). Auditing and assurance services: An integrated approach. Prentice-Hall, Hoboken, USA. [Google Scholar]

- Bakarich KM, Burke JA, and Polimeni RS (2021). Modifying the collegiate accounting curriculum to prepare for the CPA evolution project: Incorporating advances in technology into accounting programs. The CPA Journal, 91(8/9): 32-39. [Google Scholar]

- Bose S, Dey SK, and Bhattacharjee S (2023). Big data, data analytics and artificial intelligence in accounting: An overview. In: Akter S and Wamba SF (Eds.), Handbook of big data research methods: 32-51. Edward Elgar Publishing, Cheltenham, UK. https://doi.org/10.4337/9781800888555.00007 [Google Scholar]

- Čater T, Čater B, Milić P, and Žabkar V (2023). Drivers of corporate environmental and social responsibility practices: A comparison of two moderated mediation models. Journal of Business Research, 159: 113652. https://doi.org/10.1016/j.jbusres.2023.113652 [Google Scholar]

- Cherrafi A, Elfezazi S, Govindan K, Garza-Reyes JA, Benhida K, and Mokhlis A (2017). A framework for the integration of Green and Lean Six Sigma for superior sustainability performance. International Journal of Production Research, 55(15): 4481-4515. https://doi.org/10.1080/00207543.2016.1266406 [Google Scholar]

- Chilufya A, Hughes E, and Scheyvens R (2019). Tourists and community development: Corporate social responsibility or tourist social responsibility? Journal of Sustainable Tourism, 27(10): 1513-1529. https://doi.org/10.1080/09669582.2019.1643871 [Google Scholar]

- Gunarathne N, Wijayasundara M, Senaratne S, Kanchana PK, and Cooray T (2021). Uncovering corporate disclosure for a circular economy: An analysis of sustainability and integrated reporting by Sri Lankan companies. Sustainable Production and Consumption, 27: 787-801. https://doi.org/10.1016/j.spc.2021.02.003 [Google Scholar]

- Hamour H, ALensou J, Abuzaid A, Alheet A, Madadha S, and Al-Zaqeba M (2023). The effect of strategic intelligence, effective decision-making and strategic flexibility on logistics performance. Uncertain Supply Chain Management, 11(2): 657-664. https://doi.org/10.5267/j.uscm.2023.1.015 [Google Scholar]

- Hasan Z (2020). Distribution of zakat funds to achieve SDGs through poverty alleviation in Baznas republic of Indonesia. AZKA International Journal of Zakat and Social Finance, 1(1): 25-43. https://doi.org/10.51377/azjaf.vol1no01.7 [Google Scholar]

- Jarah B, Jarrah MAAL, and Al-Zaqeba M (2022). The role of internal audit in improving supply chain management in shipping companies. Uncertain Supply Chain Management, 10(3): 1023-1028. https://doi.org/10.5267/j.uscm.2022.2.011 [Google Scholar]

- Kan E and Serin ZV (2022). Analysis of cointegration and causality relations between gold prices and selected financial indicators: Empirical evidence from Turkey. International Journal of Advanced and Applied Sciences, 9(3): 1-9. https://doi.org/10.21833/ijaas.2022.03.001 [Google Scholar]

- Listiana L and Edriyanti R (2023). Digitalisation and sustainable finance in Indonesian Islamic banks. In: Almunawar MN, Pablos PO, and Anshari M (Eds.), Digital transformation for business and society: 179-195. Routledge, London, UK. https://doi.org/10.4324/9781003441298-9 [Google Scholar]

- Lutfi A, Alkelani SN, Al-Khasawneh MA, Alshira’h AF, Alshirah MH, Almaiah MA, and Ibrahim N (2022). Influence of digital accounting system usage on SMEs performance: The moderating effect of COVID-19. Sustainability, 14(22): 15048. https://doi.org/10.3390/su142215048 [Google Scholar]

- Malkawi R, Alzaqebah M, Al-Yousef A, and Abul-Huda B (2019). The impact of the digital storytelling rubrics on the social media engagements. International Journal of Computer Applications in Technology, 59(3): 269-275. https://doi.org/10.1504/IJCAT.2019.10020111 [Google Scholar]

- Mamo YA, Sisay AM, Dessalegn B, and Angaw KW (2023). The Socio-economic effect of corporate social responsibility on local community development in Southern Ethiopia. Cogent Business and Management, 10(1): 2159749. https://doi.org/10.1080/23311975.2022.2159749 [Google Scholar]

- Manita R, Elommal N, Baudier P, and Hikkerova L (2020). The digital transformation of external audit and its impact on corporate governance. Technological Forecasting and Social Change, 150: 119751. https://doi.org/10.1016/j.techfore.2019.119751 [Google Scholar]

- Masum A, Hanan H, Awang H, Aziz A, and Ahmad MH (2020). Corporate social responsibility and its effect on community development: An overview. Journal of Accounting Science, 22(1): 35-40. [Google Scholar]

- McManus T (2008). The business strategy/corporate social responsibility “mash‐up.” Journal of Management Development, 27(10): 1066-1085. https://doi.org/10.1108/02621710810916312 [Google Scholar]

- Menne F, Surya B, Yusuf M, Suriani S, Ruslan M, and Iskandar I (2022). Optimizing the financial performance of SMEs based on Sharia economy: Perspective of economic business sustainability and open innovation. Journal of Open Innovation: Technology, Market, and Complexity, 8(1): 18. https://doi.org/10.3390/joitmc8010018 [Google Scholar]

- Mikai A and Onagun AI (2020). Qitmeer network enhances zakat tracebility in Nigeria. AZKA International Journal of Zakat and Social Finance, 1(1): 164-179. https://doi.org/10.51377/azjaf.vol1no01.18 [Google Scholar]

- Mosteanu NR and Faccia A (2020). Digital systems and new challenges of financial management–FinTech, XBRL, blockchain and cryptocurrencies. Quality–Access to Success, 21(174): 159-166. [Google Scholar]

- Nabi MG, Islama MA, Waheduzzaman M, and Sarderb MMR (2021). Estimation of zakat and its use as an effective tool for socio-economic development in Bangladesh. Thoughts on Economics, 31(1): 33-56. [Google Scholar]

- Narulitasari D, Mulya ASM, and Subagyo T (2023). Zakat accounting and public accountability: Evidence from Indonesia. Journal of Islamic Finance and Accounting, 6(1): 45-59. https://doi.org/10.22515/jifa.v6i1.6805 [Google Scholar]

- Patel R, Migliavacca M, and Oriani ME (2022). Blockchain in banking and finance: A bibliometric review. Research in International Business and Finance, 62: 101718. https://doi.org/10.1016/j.ribaf.2022.101718 [Google Scholar]

- Pham QM and Thu Ho TT (2022). Impacts of factors affecting the business efficiency of seafood companies listed on the stock market of Vietnam. International Journal of Advanced and Applied Sciences, 9(3): 165-171. https://doi.org/10.21833/ijaas.2022.03.019 [Google Scholar]

- Rabbani MR, Bashar A, Nawaz N, Karim S, Ali MAM, Rahiman HU, and Alam MS (2021). Exploring the role of Islamic Fintech in combating the aftershocks of COVID-19: The open social innovation of the Islamic financial system. Journal of Open Innovation: Technology, Market, and Complexity, 7(2): 136. https://doi.org/10.3390/joitmc7020136 [Google Scholar] PMCid:PMC9906483

- Salehi M, Ammar Ajel R, and Zimon G (2022). The relationship between corporate governance and financial reporting transparency. Journal of Financial Reporting and Accounting, 21(5): 1049-1072. https://doi.org/10.1108/JFRA-04-2021-0102 [Google Scholar]

- Sari DF, Beik IS, and Rindayati W (2019). Investigating the impact of zakat on poverty alleviation: A case from West Sumatra, Indonesia. International Journal of Zakat, 4(2): 1-12. https://doi.org/10.37706/ijaz.v4i2.180 [Google Scholar]

- Shubailat OM, Al-Zaqeba MA, Madi A, and Khairi KF (2024). Investigation the effect of digital taxation and digital accounting on customs efficiency and port sustainability. International Journal of Data and Network Science. International Journal of Data and Network Science, 8(1): 61-68. https://doi.org/10.5267/j.ijdns.2023.10.017 [Google Scholar]

- Spilnyk I, Brukhanskyi R, Struk N, Kolesnikova O, and Sokolenko L (2022). Digital accounting: Innovative technologies cause a new paradigm. Independent Journal of Management and Production, 13(3): s215-s224. https://doi.org/10.14807/ijmp.v13i3.1991 [Google Scholar]

- Thakker P and Japee G (2023). Emerging technologies in accountancy and finance: A comprehensive review. European Economic Letters, 13(3): 993-1011. [Google Scholar]

- Wachira MM, Berndt T, and Romero CM (2020). The adoption of international sustainability and integrated reporting guidelines within a mandatory reporting framework: Lessons from South Africa. Social Responsibility Journal, 16(5): 613-629. https://doi.org/10.1108/SRJ-12-2018-0322 [Google Scholar]

- Yáñez-Valdés C and Guerrero M (2023). Equity crowdfunding platforms and sustainable impacts: Encountering investors and technological initiatives for tackling social and environmental challenges. European Journal of Innovation Management. https://doi.org/10.1108/EJIM-03-2022-0127 [Google Scholar]

- Yeo WJ, van der Heever W, Mao R, Cambria E, Satapathy R, and Mengaldo G (2023). A comprehensive review on financial explainable AI. ArXiv Preprint ArXiv: 2309.11960. https://doi.org/10.48550/arXiv.2309.11960 [Google Scholar]

- Yusuf SSN, Sanawi NH, Ghani EK, Muhammad R, Daud D, and Kasim ES (2022). Examining technology improvement, procedural application and governance on the effectiveness zakat distribution. International Journal of Ethics and Systems, 40(1): 103-126. https://doi.org/10.1108/IJOES-02-2022-0031 [Google Scholar]

- Zhou N and Wang H (2020). Foreign subsidiary CSR as a buffer against parent firm reputation risk. Journal of International Business Studies, 51: 1256-1282. https://doi.org/10.1057/s41267-020-00345-7 [Google Scholar]

- Zobi M, Al-Zaqeba M, and Jarah B (2023). Taxation and customs strategies in Jordanian supply chain management: Shaping sustainable design and driving environmental responsibility. Uncertain Supply Chain Management, 11(4): 1859-1876. https://doi.org/10.5267/j.uscm.2023.6.005 [Google Scholar]