International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 8 (August 2023), Pages: 209-214

----------------------------------------------

Original Research Paper

Assessing the impact of the COVID-19 pandemic on the performance of the Vietnam stock exchange: An empirical analysis

Author(s):

Pham Thanh Dat 1, Pham Dan Khanh 2, *, Vu Duy Minh 1, Nguyen Thanh Trung 1

Affiliation(s):

1School of Banking and Finance, National Economics University, Hanoi, Vietnam

2School of Advanced Educational Program, National Economics University, Hanoi, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0170-8636

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0170-8636

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2023.08.024

Abstract:

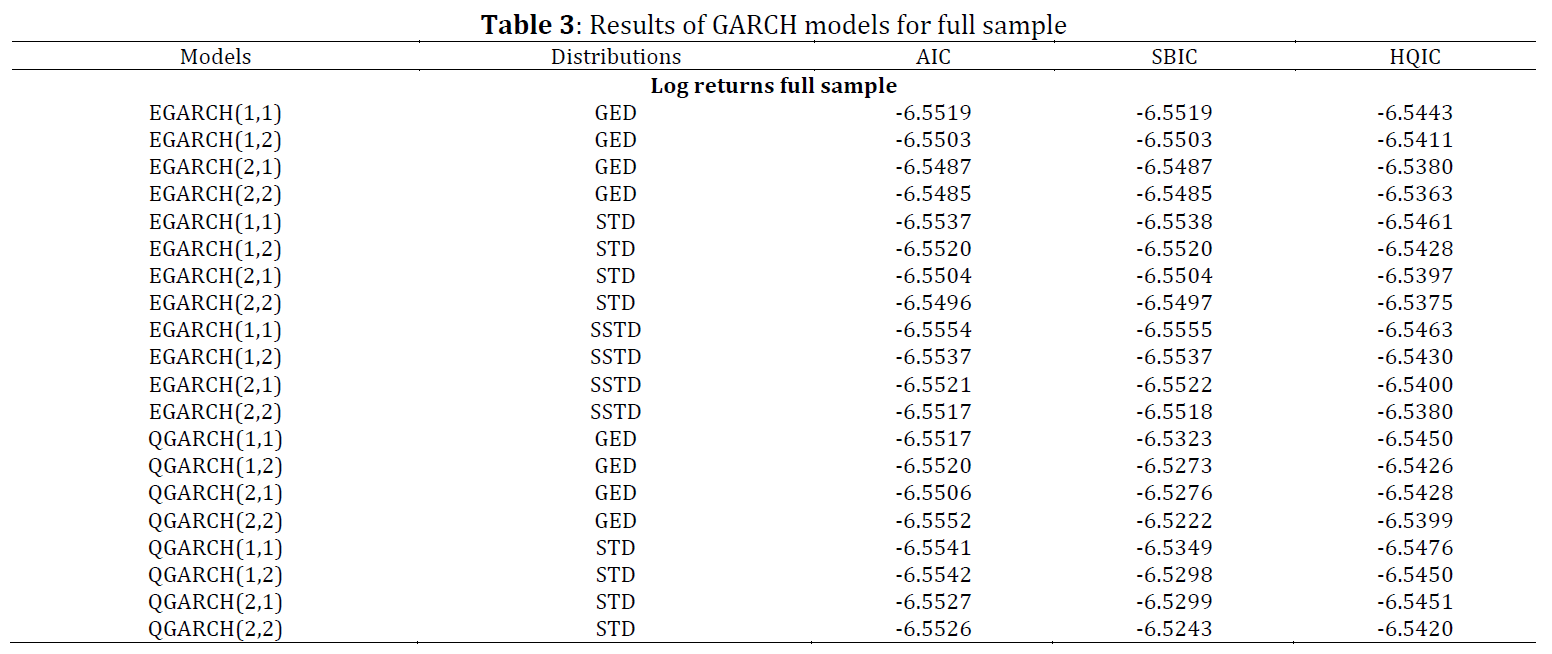

The emergence of COVID-19 in Wuhan, China, in December 2019 led to a global crisis with profound implications for public health and the global economy. This study investigates the ramifications of the pandemic on the Vietnam Stock Exchange, recognizing its interconnectedness with global financial markets. Despite the considerable speculation surrounding the pandemic's influence on economic and financial systems worldwide, limited empirical research has been conducted on its specific impact on the Vietnam Stock Exchange. Employing historical data spanning from January 30, 2020, to April 27, 2022, sourced from a secondary dataset, this research empirically explores the performance of the Vietnam Stock Exchange during the COVID-19 pandemic period compared to a normal period. The findings reveal a significant decline in stock returns and heightened volatility during the pandemic, signaling adverse effects on the exchange's performance. Furthermore, the study applies Quadratic GARCH (QGARCH) and Exponential GARCH (EGARCH) models, incorporating a dummy variable, to scrutinize stock returns. The results corroborate the pandemic's negative impact on stock returns in Vietnam. This research underscores the importance of implementing strategic political and economic policies, including maintaining a stable political environment, promoting indigenous enterprises, diversifying the economy, and adopting a flexible exchange rate regime. These measures are recommended to enhance the resilience of the financial market and attract new investors to the Ho Chi Minh Stock Exchange.

© 2023 The Authors. Published by IASE.

This is an

Keywords: Vietnam stock exchange, Stock returns, Volatility, GARCH models, Financial market

Article History: Received 27 March 2023, Received in revised form 20 July 2023, Accepted 26 July 2023

Acknowledgment

This research is funded by the National Economics University, Hanoi, Vietnam.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Dat PT, Khanh PD, Minh VD, and Trung NT (2023). Assessing the impact of the COVID-19 pandemic on the performance of the Vietnam stock exchange: An empirical analysis. International Journal of Advanced and Applied Sciences, 10(8): 209-214

Figures

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (24)

- Ajami R (2020). Globalization, the challenge of COVID-19 and oil price uncertainty. Journal of Asia-Pacific Business, 21(2): 77-79. https://doi.org/10.1080/10599231.2020.1745046 [Google Scholar]

- Akanni LO and Gabriel SC (2020). The implication of COVID-19 on the Nigerian economy. Centre for the Study of the Economies of Africa (CSEA), Abuja, Nigeria. [Google Scholar]

- Al-Qaness MA, Ewees AA, Fan H, and Abd El Aziz M (2020). Optimization method for forecasting confirmed cases of COVID-19 in China. Journal of Clinical Medicine, 9(3): 674. https://doi.org/10.3390/jcm9030674 [Google Scholar] PMid:32131537 PMCid:PMC7141184

- Andresen T and Bollerslev T (1998). DM-Dollar volatility: Intraday activity patterns, macroeconomic announcements and longer run dependence. Journal of Finance, 53: 219-265. https://doi.org/10.1111/0022-1082.85732 [Google Scholar]

- Apergis N and Apergis E (2020). The role of COVID-19 for Chinese pengembalian sahams: Evidence from a GARCHX model. Asia-Pacific Journal of Accounting and Economics, 29(5): 1175-1183. https://doi.org/10.1080/16081625.2020.1816185 [Google Scholar]

- Baig AS, Butt HA, Haroon O, and Rizvi SAR (2021). Deaths, panic, lockdowns and US equity markets: The case of COVID-19 pandemic. Finance Research Letters, 38: 101701. https://doi.org/10.1016/j.frl.2020.101701 [Google Scholar] PMid:32837381 PMCid:PMC7381907

- Bou-Hamad I and Jamali I (2020). Forecasting financial time-series using data mining models: A simulation study. Research in International Business and Finance, 51: 101072. https://doi.org/10.1016/j.ribaf.2019.101072 [Google Scholar]

- Eleftheriou K and Patsoulis P (2020). COVID-19 lockdown intensity and stock market returns: A spatial econometrics approach. MPRA Paper No. 100662, Munich Personal RePEc Archive, Munich, Germany. [Google Scholar]

- Emenogu NG, Adenomon MO, and Nweze NO (2020). On the volatility of daily stock returns of total Nigeria Plc: Evidence from GARCH models, value-at-risk and backtesting. Financial Innovation, 6: 18. https://doi.org/10.1186/s40854-020-00178-1 [Google Scholar]

- Feinstein Z (2020). Reanimating a dead economy: Financial and economic analysis of a zombie outbreak. ArXiv Preprint ArXiv:2003.09943. https://doi.org/10.48550/arXiv.2003.09943 [Google Scholar]

- Ghosh S (2022). COVID-19, clean energy stock market, interest rate, oil prices, volatility index, geopolitical risk nexus: Evidence from quantile regression. Journal of Economics and Development, 24(4): 329-344. https://doi.org/10.1108/JED-04-2022-0073 [Google Scholar]

- Gralinski LE and Menachery VD (2020). Return of the coronavirus: 2019-nCoV. Viruses, 12(2): 135. https://doi.org/10.3390/v12020135 [Google Scholar] PMid:31991541 PMCid:PMC7077245

- Hatmanu M and Cautisanu C (2021). The impact of COVID-19 pandemic on stock market: Evidence from Romania. International Journal of Environmental Research and Public Health, 18(17): 9315. https://doi.org/10.3390/ijerph18179315 [Google Scholar] PMid:34501902 PMCid:PMC8430890

- Holý V and Tomanová P (2023). Streaming approach to quadratic covariation estimation using financial ultra-high-frequency data. Computational Economics, 62: 463-485. https://doi.org/10.1007/s10614-021-10210-w [Google Scholar]

- Hung DV, Hue NTM, and Duong VT (2021). The impact of COVID-19 on stock market returns in Vietnam. Journal of Risk and Financial Management, 14(9): 441. https://doi.org/10.3390/jrfm14090441 [Google Scholar]

- Igwe PA (2020). Coronavirus with looming global health and economic doom. African Development Institute of Research Methodology, 1(1): 1-6. [Google Scholar]

- Li Q, Guan X, Wu P, Wang X, Zhou L, Tong Y, and Feng Z (2020). Early transmission dynamics in Wuhan, China, of novel coronavirus–infected pneumonia. New England Journal of Medicine, 382: 1199-1207. https://doi.org/10.1056/NEJMoa2001316 [Google Scholar] PMid:31995857 PMCid:PMC7121484

- Malini H (2020). Behaviour of stock returns during COVID-19 pandemic: Evidence from six selected stock market in the world. Jurnal Ekonomi Indonesia, 9(3): 247-263. https://doi.org/10.52813/jei.v9i3.70 [Google Scholar]

- Nelson DB (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society, 59(2): 347-370. https://doi.org/10.2307/2938260 [Google Scholar]

- Nhuong BH, Khanh PD, and Dat PT (2020). Calendar effects: Empirical evidence from the Vietnam stock markets. International Journal of Advanced and Applied Sciences, 7(12): 48-55. https://doi.org/10.21833/ijaas.2020.12.005 [Google Scholar]

- Ozili P and Arun T (2020). Spillover of COVID-19: Impact on the global economy. MPRA Paper 99317, University Library of Munich, Munich, Germany. https://doi.org/10.2139/ssrn.3562570 [Google Scholar]

- Sentana E (1995). Quadratic ARCH models. The Review of Economic Studies, 62(4): 639-661. https://doi.org/10.2307/2298081 [Google Scholar]

- WHO (2020). Novel coronavirus (2019-nCoV). Situation Report-7, World Health Organization, Geneva, Switzerland. [Google Scholar]

- Yaya OS and Shittu OI (2010). On the impact of inflation and exchange rate on conditional stock market volatility: A re-assessment. American Journal of Scientific and Industrial Research, 1(2): 115-117. https://doi.org/10.5251/ajsir.2010.1.2.115.117 [Google Scholar]