International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 6 (June 2023), Pages: 187-194

----------------------------------------------

Original Research Paper

Zakat compliance behavior in formal zakat institutions: An integration model of religiosity, trust, credibility, and accountability

Author(s):

Nur Rizqi Febriandika *, Dilla Gading Kusuma, Yayuli

Affiliation(s):

Islamic Economic Law, Universitas Muhammadiyah Surakarta, Surakarta, Indonesia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-9063-6990

Corresponding author's ORCID profile: https://orcid.org/0000-0001-9063-6990

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2023.06.022

Abstract:

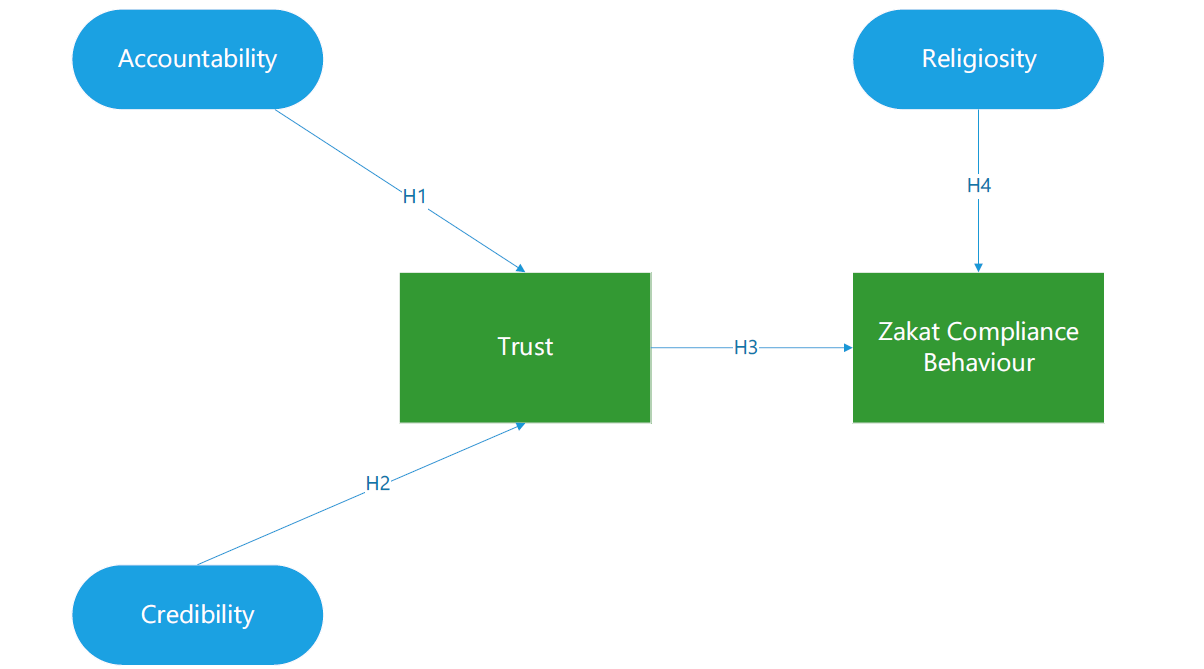

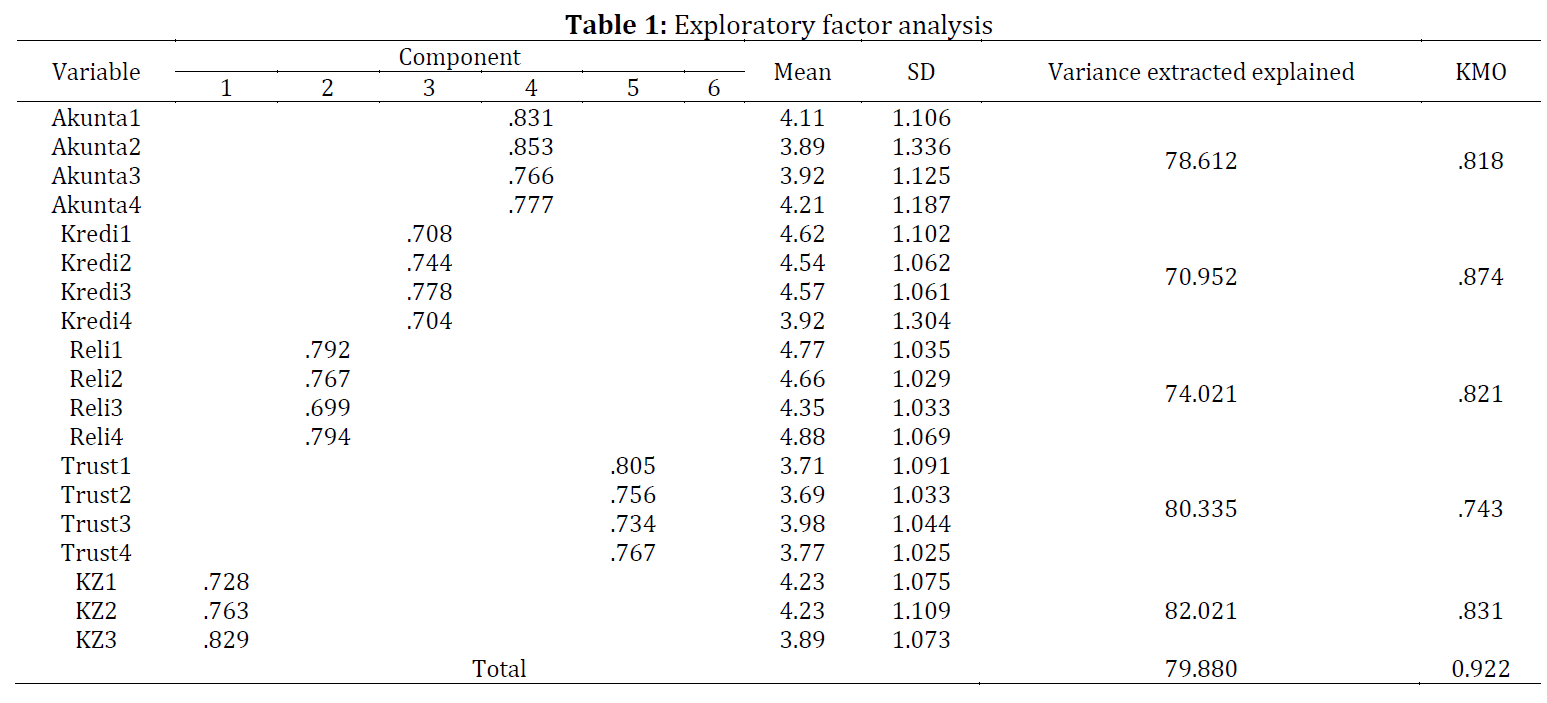

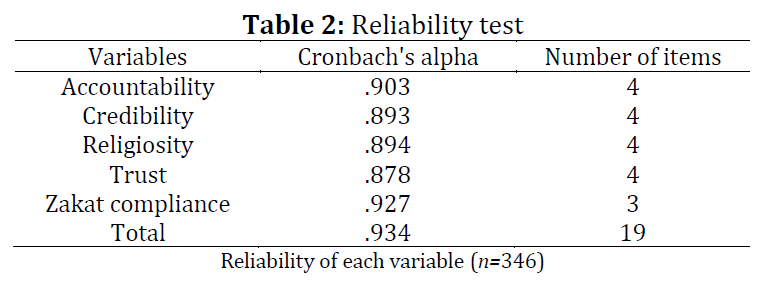

Indonesia boasts the largest Muslim population worldwide; however, the allocation of zakat funds remains relatively low. This is primarily due to the fact that numerous Muslim communities have yet to channel their zakat contributions through formal institutions. Many individuals are still unaware of their obligation to pay zakat. Previous research has predominantly employed theoretical frameworks in consumer behavior, with limited emphasis on formal zakat institutions. Consequently, there is a scarcity of socialization and counseling initiatives pertaining to formal zakat institutions within the community. Therefore, the objective of this study is to develop a model for understanding zakat compliance behavior within formal zakat institutions, with a focus on the variables of religiosity, trust, credibility, and accountability. This investigation seeks to provide a comprehensive and in-depth comprehension of the topic. The study employs a quantitative research design, utilizing the Structural Equating Modeling (SEM) method. A total of 346 respondents, categorized as Muslim citizens obligated to pay zakat, were included in the sample. The study findings indicate that accountability and credibility significantly influence trust, whereas trust and religiosity impact zakat compliance behavior. Notably, trust emerges as the most influential variable regarding compliance with zakat payments within formal zakat institutions. Conversely, the variable of religiosity exerts the weakest impact on compliance with zakat payments in formal institutions. These findings suggest that zakat institutions should prioritize the credibility variable to enhance the trust of zakat payers, thereby increasing compliance with zakat payments.

© 2023 The Authors. Published by IASE.

This is an

Keywords: Zakat compliance behavior, Formal zakat institutions, Trust, Credibility, Religiosity

Article History: Received 27 December 2022, Received in revised form 27 April 2023, Accepted 3 May 2023

Acknowledgment

This research was funded by RISETMU batch VI Majelis Diktilitbang.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Febriandika NR, Kusuma DG, and Yayuli (2023). Zakat compliance behavior in formal zakat institutions: An integration model of religiosity, trust, credibility, and accountability. International Journal of Advanced and Applied Sciences, 10(6): 187-194

Figures

{kind=link}

Tables

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (50)

- Abdullah M and Sapiei NS (2018). Do religiosity, gender and educational background influence zakat compliance? The case of Malaysia. International Journal of Social Economics, 45(8): 1250-1264. https://doi.org/10.1108/IJSE-03-2017-0091 [Google Scholar]

- Ahmad ZA and Rusdianto R (2018). The analysis of amil zakat institution/Lembaga amil zakat (LAZ) Accountability toward public satisfaction and trust. Muqtasid: Jurnal Ekonomi dan Perbankan Syariah, 9(2): 109-119. https://doi.org/10.18326/muqtasid.v9i2.109-119 [Google Scholar]

- Ajzen I (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2): 179-211. https://doi.org/10.1016/0749-5978(91)90020-T [Google Scholar]

- Al Jaffri RS and Haniffa R (2014). Determinants of zakah (Islamic tax) compliance behavior. Journal of Islamic Accounting and Business Research, 5(2): 182-193. https://doi.org/10.1108/JIABR-10-2012-0068 [Google Scholar]

- Ali MAM, Khamar Tazilah MDAB, Shamsudin AIB, Faisal Shukri FRB, Nik Adelin NMFAB, and Zainol Zaman WMSB (2017). Factors that influence the zakat collection funds: A case in Kuantan. South East Asia Journal of Contemporary Business, Economics and Law, 13(1): 30-37. [Google Scholar]

- Amalia E (2019). Good governance for zakat institutions in Indonesia: A confirmatory factor analysis. Pertanika Journal of Social Sciences and Humanities, 27(3): 1-13. https://doi.org/10.18502/kss.v3i8.2511 [Google Scholar]

- Ammeter AP, Douglas C, Ferris GR, and Goka H (2004). A social relationship conceptualization of trust and accountability in organizations. Human Resource Management Review, 14(1): 47-65. https://doi.org/10.1016/j.hrmr.2004.02.003 [Google Scholar]

- Andam AC and Osman AZ (2019). Determinants of intention to give zakat on employment income: Experience from Marawi City, Philippines. Journal of Islamic Accounting and Business Research, 10(4): 528-545. https://doi.org/10.1108/JIABR-08-2016-0097 [Google Scholar]

- Ayuniyyah Q, Hafidhuddin D, and Hambari H (2020). The strategies in strengthening the role of zakat boards and institutions in Indonesia. International Journal of Zakat, 5(3): 73-87. https://doi.org/10.37706/ijaz.v5i3.244 [Google Scholar]

- Aziz MRA and Anim NAHM (2020). Trust towards zakat institutions among Muslims business owners. Jurnal Ekonomi and Keuangan Islam, 6(1): 1-9. https://doi.org/10.20885/jeki.vol6.iss1.art1 [Google Scholar]

- Azman FMN and Bidin Z (2015). Zakat compliance intention behavior on saving. International Journal of Business and Social Research, 5(1): 118-128. [Google Scholar]

- Bin Khamis MR, Salleh AM, and Nawi AS (2011). Compliance behavior of business zakat payment in Malaysia: A theoretical economic exposition. In the 8th International Conference on Islamic Economics and Finance, Doha, Qatar: 1-17. [Google Scholar]

- Bin-Nashwan SA, Abdul-Jabbar H, Aziz SA, and Haladu A (2020). Zakah compliance behavior among entrepreneurs: Economic factors approach. International Journal of Ethics and Systems, 36(2): 285-302. https://doi.org/10.1108/IJOES-09-2019-0145 [Google Scholar]

- Bovens M, Goodin R, and Schillemans T (2014). The Oxford handbook of public accountability. Oxford University Press, Oxford, UK. https://doi.org/10.1093/oxfordhb/9780199641253.001.0001 [Google Scholar]

- Castro-Gonzalez S, Bande B, and Fernandez-Ferrin P (2021). Influence of companies credibility and trust in corporate social responsibility aspects of consumer food products: The moderating intervention of consumer integrity. Sustainable Production and Consumption, 28: 129-141. https://doi.org/10.1016/j.spc.2021.03.032 [Google Scholar]

- Dumont GE (2013). Nonprofit virtual accountability: An index and its application. Nonprofit and Voluntary Sector Quarterly, 42(5): 1049-1067. https://doi.org/10.1177/0899764013481285 [Google Scholar]

- Farah JMS, Shafiai MHBM, and Ismail AGB (2019). Compliance behaviour on Zakat donation: A qualitative approach. In IOP Conference Series: Materials Science and Engineering, IOP Publishing, 572(1): 012040. https://doi.org/10.1088/1757-899X/572/1/012040 [Google Scholar]

- Farouk AU, Md Idris K, and Saad RAJB (2018). Moderating role of religiosity on zakat compliance behavior in Nigeria. International Journal of Islamic and Middle Eastern Finance and Management, 11(3): 357-373. https://doi.org/10.1108/IMEFM-05-2017-0122 [Google Scholar]

- Febriandika NR, Millatina AN, and Herianingrum S (2020). Customer e-loyalty of Muslim millennials in Indonesia: Integrated model of trust, user experience and branding in e-commerce webstore. In the 11th International Conference on E-Education, E-Business, E-Management, and E-Learning, Association for Computing Machinery, Osaka, Japan: 369-376. https://doi.org/10.1145/3377571.3377638 [Google Scholar]

- Hakimi F, Widiastuti T, Al-Mustofa MU, and Al Husanaa R (2021). Positive effect of attitude, peer influence, and knowledge zakat on zakat compliance behavior: Update in COVID-19. Journal of Islamic Economic Laws, 4: 2. https://doi.org/10.23917/jisel.v4i2.13859 [Google Scholar]

- Heikal M, Khadafi M, and Falahuddin F (2014). The intention to pay zakat commercial: An application of revised theory of planned behavior. Journal of Economics and Behavioral Studies, 6(9): 727-734. https://doi.org/10.22610/jebs.v6i9.532 [Google Scholar]

- Hupcey JE, Penrod J, Morse JM, and Mitcham C (2001). An exploration and advancement of the concept of trust. Journal of Advanced Nursing, 36(2): 282-293. https://doi.org/10.1046/j.1365-2648.2001.01970.x [Google Scholar] PMid:11580804

- Hyndman N and McConville D (2018). Trust and accountability in UK charities: Exploring the virtuous circle. The British Accounting Review, 50(2): 227-237. https://doi.org/10.1016/j.bar.2017.09.004 [Google Scholar]

- Idris KM, Bidin Z, and Saad RAJ (2012). Islamic religiosity measurement and its relationship with business income zakat compliance behavior. Jurnal Pengurusan, 34: 3-10. https://doi.org/10.17576/pengurusan-2012-34-01 [Google Scholar]

- Jijelava D and Vanclay F (2017). Legitimacy, credibility and trust as the key components of a social licence to operate: An analysis of BP's projects in Georgia. Journal of Cleaner Production, 140: 1077-1086. https://doi.org/10.1016/j.jclepro.2016.10.070 [Google Scholar]

- Jinni N and Amin H (2020). Explaining the effects of Shariah compliance, financial freedom and religiosity on Islamic home financing acceptance in Kota Kinabalu, Sabah. Labuan Bulletin of International Business and Finance, 18(1): 62–74. https://doi.org/10.51200/lbibf.v18i1.2688 [Google Scholar]

- Jo S (2005). The effect of online media credibility on trust relationships. Journal of Website Promotion, 1(2): 57-78. https://doi.org/10.1300/J238v01n02_04 [Google Scholar]

- Khasandy EA and Badrudin R (2019). The influence of zakat on economic growth and welfare society in Indonesia. Integrated Journal of Business and Economics, 3(1): 65-79. https://doi.org/10.33019/ijbe.v3i1.89 [Google Scholar]

- LoBiondo-Wood G and Haber J (2014). Nursing research: Methods and critical appraisal for evidence-based practice. 8th Edition, Mosby Elsevier, St. Louis, USA. https://doi.org/10.1016/S2155-8256(15)30102-2 [Google Scholar]

- Love PE, Eldabi T, Irani Z, and Paul R (2002). Quantitive and qualitive decision making methods in simulation modelling. Management Decision, 40(1): 64-73. https://doi.org/10.1108/00251740210413370 [Google Scholar]

- Manurung S (2013). Islamic religiosity and development of zakat institution. Qudus International Journal of Islamic Studies, 1(2): 197-220. [Google Scholar]

- Masrek MN, Halim MSA, Khan A, and Ramli I (2018). The impact of perceived credibility and perceived quality on trust and satisfaction in mobile banking context. Asian Economic and Financial Review, 8(7): 1013-1025. https://doi.org/10.18488/journal.aefr.2018.87.1013.1025 [Google Scholar]

- Mustika FN, Setyowati E, and Alam A (2019). Analysis of effect of ZIS (Zakat, Infaq, and Shadaqah), regional domestic products of Bruto, regional minimum wage and inflation on levels poverty in Indonesia 2012–2016. Journal of Islamic Economic Laws, 2(2): 193-211. https://doi.org/10.23917/jisel.v2i2.8679 [Google Scholar]

- Najiyah F and Febriandika NR (2018). The role of government in the zakat management: The implementation of a centralized and decentralized approach (comparative study in Indonesia and Malaysia). In the 1st International Conference on Islamic Economics and Business, Atlantis Press, Malang, Indonesia: 290-292. [Google Scholar]

- Nasri R, Aeni N, and Haque-Fawzi MG (2019). Determination of professionalism and transparency and its implications for the financial performance of zakat institutions. Journal of Islamic Monetary Economics and Finance, 5(4): 785-806. https://doi.org/10.21098/jimf.v5i4.1158 [Google Scholar]

- Renn O and Levine D (1991). Credibility and trust in risk communication. In: Kasperson RE and Stallen PJM (Eds.), Communicating risks to the public: Technology, risk, and society: 175–217. Volume 4, Springer, Dordrecht, Netherlands. https://doi.org/10.1007/978-94-009-1952-5_10 [Google Scholar]

- Roziq A, Sulistiyo AB, Shulthoni M, and Anugerah EG (2021). An escalation model of muzakki's trust and loyalty towards payment of zakat at baznas Indonesia. The Journal of Asian Finance, Economics and Business, 8(3): 551-559. [Google Scholar]

- Saad RAJ, Farouk AU, and Abdul Kadir D (2020). Business zakat compliance behavioral intention in a developing country. Journal of Islamic Accounting and Business Research, 11(2): 511-530. https://doi.org/10.1108/JIABR-03-2018-0036 [Google Scholar]

- Saad RAJ, Wahab MSA, and Samsudin MAM (2016). Factors influencing business zakah compliance behavior among Moslem businessmen in Malaysia: A research model. Procedia-Social and Behavioral Sciences, 219: 654-659. https://doi.org/10.1016/j.sbspro.2016.05.047 [Google Scholar]

- Sadallah M, Abdul-Jabbar H, and Aziz SA (2022). Promoting zakat compliance among business owners in Algeria: The mediation effect of compliance intention. Journal of Islamic Marketing, 14(6): 1603-1620. https://doi.org/10.1108/JIMA-11-2021-0366 [Google Scholar]

- Sapingi R, Ahmad N, and Mohamad M (2011). A study on zakah of employment income: Factors that influence academics’ intention to pay zakah. In the 2nd International Conference on Business and Economic Research, Langkawi, Malaysia: 2492-2507. [Google Scholar]

- Sawmar AA and Mohammed MO (2021). Enhancing zakat compliance through good governance: A conceptual framework. ISRA International Journal of Islamic Finance, 13(1): 136-154. https://doi.org/10.1108/IJIF-10-2018-0116 [Google Scholar]

- Sulaiman Y, Rahman MA, and Mat NKN (2019). The conceptual paper on service quality and business zakat compliance behaviour among SMEs in Kedah. Journal of Accounting, Business and Finance Research, 5(1): 23-28. https://doi.org/10.20448/2002.51.23.28 [Google Scholar]

- Swift T (2001). Trust, reputation and corporate accountability to stakeholders. Business Ethics: A European Review, 10(1): 16-26. https://doi.org/10.1111/1467-8608.00208 [Google Scholar]

- Syafira FN, Ratnasari RT, and Ismail S (2020). The effect of religiosity and trust on intention to pay in ziswaf collection through digital payments. Jurnal Ekonomi dan Bisnis Islam, 6(1): 98-115. https://doi.org/10.20473/jebis.v6i1.17293 [Google Scholar]

- Tamimah T (2020). Compliance determinant of paying zakat maal. AL-FALAH: Journal of Islamic Economics, 5(2): 213-230. https://doi.org/10.29240/alfalah.v5i2.1228 [Google Scholar]

- Tsalas NA, Mahri AJW, and Rosida R (2019). Zakat compliance behaviour: Good corporate governance with muzakki’s trust approach (survey on muzakki of the national board of zakat (BAZNAS) in Garut). In the 2nd International Conference on Islamic Economics, Business, and Philanthropy, KnE Social Sciences, Surabaya, Indonesia: 796–808. https://doi.org/10.18502/kss.v3i13.4248 [Google Scholar]

- Ullman JB and Bentler PM (2013). Structural equation modeling. In: Schinka JA, Velicer WF, and Weiner IB (Eds.), Handbook of psychology: Research methods in psychology: 661–690. John Wiley and Sons, Hoboken, USA. [Google Scholar]

- Ummulkhayr A, Owoyemi MY, and Cusairi RBM (2017). Determinants of zakat compliance behavior among Muslims living under non-Islamic governments. International Journal of Zakat, 2(1): 95-108. https://doi.org/10.37706/ijaz.v2i1.18 [Google Scholar]

- Wahab NA and Rahman ARA (2011). A framework to analyses the efficiency and governance of zakat institutions. Journal of Islamic Accounting and Business Research, 2(1): 43-62. https://doi.org/10.1108/17590811111129508 [Google Scholar]