International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 5 (May 2023), Pages: 20-27

----------------------------------------------

Original Research Paper

Audit committee characteristics and firm performance: Evidence from the insurance sector in Oman

Author(s):

Abdulqawi A. Hezabr 1, Mohammed H. M. Qeshta 1, Faiza Mohmmed Al-Msni 2, 3, Omar Jawabreh 4, *, Basel J. A. Ali 1

Affiliation(s):

1Accounting and Finance Department, Applied Science University, Manama, Bahrain

2Accounting Department, Sana’a University, Sanaa, Yemen

3Accounting Department, Ar-Rasheed Smart University, Sanaa, Yemen

4Department of Hotel Management, Faculty of Tourism and Hospitality, The University of Jordan, Aqaba, Jordan

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-5647-895X

Corresponding author's ORCID profile: https://orcid.org/0000-0001-5647-895X

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2023.05.003

Abstract:

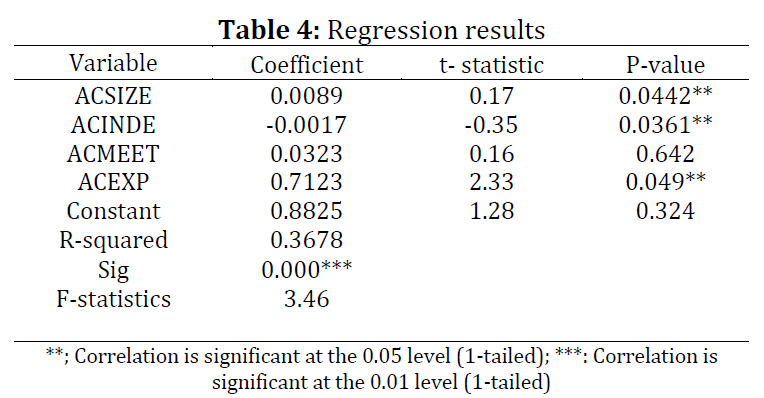

This study aims to determine the effect of audit committee characteristics on the performance of the eleven insurance companies listed in Oman between 2015 and 2019. This study focuses on the audit committee meetings and their frequency, the size of the committee, their independence, and the knowledge or expertise they possess. After conducting data analysis on the specified dataset, the regression results revealed that audit committee size is statistically significant at a p-value less than .05. This indicates that the size of an audit committee has a significant impact on an insurance company's performance. In addition, the audit committee independence was statistically significant at p=.05, demonstrating that the independence of an audit committee plays a significant role in determining the performance of a company. Moreover, the Audit committee expertise variable had a p-value of less than 0.05, indicating that it is statistically significant. This can be interpreted as meaning that the frequency of meetings has a statistically significant impact on the performance of a company. The statistical significance of only three of the four variables was determined. The variable was excluded from the regression model because its p-value was greater than .05. Therefore, the three characteristics of audit committees in the Omani market have a significant impact on the performance of an insurance company, and senior management should ensure that audit committees have approximately four members, are fully independent to limit control by the firm's management, and have extensive financial experience in order to function effectively. This study will be very useful to financial practitioners and policymakers since it contains practical ideas and recommendations. The research results may also contribute to the creation and implementation of strategic policies for improving corporate governance practices with the goal of maximizing profit and wealth.

© 2023 The Authors. Published by IASE.

This is an

Keywords: Firm performance, Committee size, Independence, Experience, Meeting, Oman

Article History: Received 1 October 2022, Received in revised form 23 January 2023, Accepted 8 February 2023

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Hezabr AA, Qeshta MHM, Al-Msni FM, Jawabreh O, and Ali BJA (2023). Audit committee characteristics and firm performance: Evidence from the insurance sector in Oman. International Journal of Advanced and Applied Sciences, 10(5): 20-27

Figures

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (48)

- Abdelbadie RA and Salama A (2019). Corporate governance and financial stability in US banks: Do indirect interlocks matter? Journal of Business Research, 104: 85-105. https://doi.org/10.1016/j.jbusres.2019.06.047 [Google Scholar]

- Abdou HA, Ellelly NN, Elamer AA, Hussainey K, and Yazdifar H (2021). Corporate governance and earnings management nexus: Evidence from the UK and Egypt using neural networks. International Journal of Finance and Economics, 26(4): 6281-6311. https://doi.org/10.1002/ijfe.2120 [Google Scholar]

- Al Fahmawee EAD and Jawabreh OA (2022). A study architectural and intangible environment affecting occupancy rate of five stars business hotel in Amman. Journal of Environmental Management and Tourism, 13(2): 530-545. https://doi.org/10.14505/jemt.v13.2(58).22 [Google Scholar]

- Al Lawati H, Hussainey K, and Sagitova R (2021). Disclosure quality vis-à-vis disclosure quantity: Does audit committee matter in Omani financial institutions? Review of Quantitative Finance and Accounting, 57(2): 557-594. https://doi.org/10.1007/s11156-020-00955-0 [Google Scholar]

- Al-Absy MSM, Ismail KNIK, and Chandren S (2019). Audit committee chairman characteristics and earnings management: The influence of family chairman. Asia-Pacific Journal of Business Administration, 11(4): 339-370. https://doi.org/10.1108/APJBA-10-2018-0188 [Google Scholar]

- Alawamleh HA, ALShibly MHAA, Tommalieh AFA, Al-Qaryouti MQH, and Ali BJ (2021). The challenges, barriers and advantages of management information system development: Comprehensive review. Academy of Strategic Management Journal, 20(5): 1-8. [Google Scholar]

- Al-Faryan MAS and Dockery E (2021). Testing for efficiency in the Saudi stock market: Does corporate governance change matter? Review of Quantitative Finance and Accounting, 57(1): 61-90. https://doi.org/10.1007/s11156-020-00939-0 [Google Scholar]

- Ali BJ and Oudat MS (2021a). Accounting information system and financial sustainability of commercial and Islamic banks: A review of the literature. Journal of Management Information and Decision Sciences, 24(5): 1-17. [Google Scholar]

- Ali BJ and Oudat MS (2021b). Board characteristics and intellectual capital performance: Empirical evidence of Bahrain commercial banks. Academy of Accounting and Financial Studies Journal, 25(4): 1-10. [Google Scholar]

- Ali BJ, Alawamleh HA, Allahham MIO, Alsaraireh JM, AL-Zyadat A, and Badadwa A (2022). Integration of supply chains and operational performance: The moderating effects of knowledge. Information Sciences Letters, 11(4): 1069-1076. https://doi.org/10.18576/isl/110407 [Google Scholar]

- Ali MR, Mahmud MS, and Lima RP (2016). Analyzing Tobin’s Q ratio of banking industry of Bangladesh: A comprehensive guideline for investors. Asian Business Review, 6(2): 85-90. https://doi.org/10.18034/abr.v6i2.31 [Google Scholar]

- Alkhodary D, Abu-AlSondos IA, Ali BJ, Shehadeh M, and Salhab HA (2022). Visitor management system design and implementation during the COVID-19 pandemic. Information Sciences Letters, 11(4): 1059-1067. https://doi.org/10.18576/isl/110406 [Google Scholar]

- Al-Mamun A, Yasser QR, Rahman MA, Wickramasinghe A, and Nathan TM (2014). Relationship between audit committee characteristics, external auditors and economic value added (EVA) of public listed firms in Malaysia. Corporate Ownership and Control, 12(1): 899-910. https://doi.org/10.22495/cocv12i1c9p12 [Google Scholar]

- Al-Matari EM, Al-Swidi AK, and Fadzil FHB (2014). Audit committee characteristics and executive committee characteristics and firm performance in Oman: Empirical study. Asian Social Science, 10(12): 98-113. https://doi.org/10.5539/ass.v10n12p98 [Google Scholar]

- Al-Matari YA, Al-Swidi AK, Fadzil FHBH, and Al-Matari EM (2012). Board of directors, audit committee characteristics and the performance of Saudi Arabia listed companies. International Review of Management and Marketing, 2(4): 241-251. https://doi.org/10.5296/ijafr.v2i2.2384 [Google Scholar]

- AlNawaiseh KH, Hamzeh AA, Al Shibly M, Almari MO, AbuOrabi T, Jerisat R, Basel A, and Badadwa A (2022). The relationship between the enterprise resource planning system and maintenance planning system: An empirical study. Information Sciences Letters, 11(5): 1335-1343. https://doi.org/10.18576/isl/110502 [Google Scholar]

- Alqaraleh MH, Almari MOS, Ali BJ, and Oudat MS (2022). The mediating role of organizational culture on the relationship between information technology and internal audit effectiveness. Corporate Governance and Organizational Behavior Review, 6(1): 8-18. https://doi.org/10.22495/cgobrv6i1p1 [Google Scholar]

- Alrabei AM, Al-Othman LN, Al-Dalabih FA, Taber TA, and Ali BJ (2022). The impact of mobile payment on the financial inclusion rates. Information Sciences Letters, 11(4): 1033-1044. https://doi.org/10.18576/isl/110404 [Google Scholar]

- Alsarayreh MN, Jawabreh OA, Jaradat MM, and ALamro SA (2011). Technological impacts on effectiveness of accounting information systems (AIS) applied by Aqaba tourist hotels. European Journal of Scientific Research, 59(3): 361-369. [Google Scholar]

- Alshabibi B, Pria S, and Hussainey K (2021). Audit committees and COVID-19-related disclosure tone: Evidence from Oman. Journal of Risk and Financial Management, 14(12): 609. https://doi.org/10.3390/jrfm14120609 [Google Scholar]

- Alshirah M, Al-Dalabih F, Alshira’h A, Alsqour M, and Ali B (2022). The relationship between tax knowledge and compliance: An empirical study. Information Sciences Letters, 11(5): 1393-1401. https://doi.org/10.18576/isl/110508 [Google Scholar]

- Alyaarubi HJ, Alkindi DS, and Ahmed ER (2021). Internal auditing quality and earnings management: evidence from sultanate of Oman. Journal of Governance and Integrity, 4(2): 115-124. https://doi.org/10.15282/jgi.4.2.2021.6054 [Google Scholar]

- Arslan M, Zaman R, Malik RK, and Mehmood A (2014). Impact of CEO duality and audit committee on firm performance: A study of oil and gas listed firms of Pakistan. Research Journal of Finance and Accounting, 5(17): 151-156. https://doi.org/10.2139/ssrn.2515067 [Google Scholar]

- Badolato PG, Donelson DC, and Ege M (2014). Audit committee financial expertise and earnings management: The role of status. Journal of Accounting and Economics, 58(2-3): 208-230. https://doi.org/10.1016/j.jacceco.2014.08.006 [Google Scholar]

- Buallay A and Al-Ajmi J (2019). The role of audit committee attributes in corporate sustainability reporting: Evidence from banks in the Gulf cooperation council. Journal of Applied Accounting Research. 20(2): 249-264. https://doi.org/10.1108/JAAR-06-2018-0085 [Google Scholar]

- Ebrahim SAH, Ali BJA., and Oudat MS (2021). The effect of board characteristics on intellectual capital in the commercial banks sector listed on the Bahrain bourse: An empirical study. Information Sciences Letters, 10(4): 91-109. https://doi.org/10.18576/isl/10S106 [Google Scholar]

- Fu L, Singhal R, and Parkash M (2016). Tobin's q ratio and firm performance. International Research Journal of Applied Finance, 7(4): 1-10. [Google Scholar]

- Gharaibeh AT, Saleh MH, Jawabreh O, and Ali BJ (2022). An empirical study of the relationship between earnings per share, net income, and stock price. Journal of Applied Mathematics, 16(5): 673-679. https://doi.org/10.18576/amis/160502 [Google Scholar]

- Harban FJMJ, Ali BJ, and Oudat MS (2021). The effect of financial risks on the financial performance of banks listed on Bahrain bourse: An empirical study. Information Sciences Letters, 10(S1): 71-89. https://doi.org/10.18576/isl/10S105 [Google Scholar]

- Jaradat MM, Jawabreh OA, Saleh MMA, and Abu-Eker EFM (2011). The extent of applying the methods of management accounting in planning, controlling and pricing in Aqaba hotels. European Journal of Economics, Finance and Administrative Sciences, 36: 123-132. [Google Scholar]

- Jawabreh O (2020). Innovation management in hotels industry in Aqaba special economic zone authority; hotel classification and administration as a moderator. Geo Journal of Tourism and Geosites, 32(4): 1362-1369. https://doi.org/10.30892/gtg.32425-581 [Google Scholar]

- Jawabreh O, Abdelrazaq H, and Jahmani A (2021). Business sustainability practice and operational management in hotel industry in Aqaba special authority economic zone authority (ASEZA). Geo Journal of Tourism and Geosites, 38(4): 1089-1097. https://doi.org/10.30892/gtg.38414-748 [Google Scholar]

- Jawabreh O, Jahmani A, Shukri MB, and Ali BJA (2022a). Evaluation of the contents of the five stars hotel website and customer orientation. Information Sciences Letters, 11(4): 1077-1085. https://doi.org/10.18576/isl/110408 [Google Scholar]

- Jawabreh O, Shniekat N, Saleh MMA, and Ali BJ (2022b). The strategic deployment of information systems attributes and financial performance in the hospitality industry. Information Sciences Letters, 11(5): 1419-1426. https://doi.org/10.18576/isl/110510 [Google Scholar]

- Jawabreh OA, Fahmawee EADA, Al-Rawashdeh OM, Alrowwad A, and Alrjoub AMS (2022c). Green energy products and the relationship of the customer's consideration for the environment and perceived risk involved with the mediating position of customer purchasing intentions: The point of view of foreign tourist in Jordan. International Journal of Energy Economics and Policy, 12(4): 334-341. https://doi.org/10.32479/ijeep.13265 [Google Scholar]

- Nawaiseh KHA, Abd-Alkareem MH, Alawamleh HA, Abbas KM, and Orabi TGA (2021). Dimensions of corporate governance and organizational learning: An empirical study. Journal of Management Information and Decision Sciences, 24(5): 1-11. [Google Scholar]

- Oudat MS, Ali B, and Qeshta MH (2021). Financial performance and audit committee characteristics: An empirical study on Bahrain services sector. Journal of Contemporary Issues in Business and Government, 27(2): 4278-4288. https://doi.org/10.47750/cibg.2021.27.02.453 [Google Scholar]

- Qeshta MH, Alsoud GFA, Hezabr AA, Ali BJ, and Oudat MS (2021). Audit committee characteristics and firm performance: Evidence from the insurance sector in Bahrain. Revista Geintec-Gestao Inovacao E Tecnologias, 11(2): 1666-1680. https://doi.org/10.47059/revistageintec.v11i2.1789 [Google Scholar]

- Rahman MM, Meah MR, and Chaudhory NU (2019). The impact of audit characteristics on firm performance: An empirical study from an emerging economy. The Journal of Asian Finance, Economics and Business, 6(1): 59-69. https://doi.org/10.13106/jafeb.2019.vol6.no1.59 [Google Scholar]

- Salameh A, AlSondos IA, Ali B, and Alsahali A (2020). From citizen’s overview: Which antecedents’ can assist to increase their satisfaction towards the ubiquity of mobile commerce applications? International Journal of Interactive Mobile Technologies, 14(17): 45-54. https://doi.org/10.3991/ijim.v14i17.16589 [Google Scholar]

- Saleh M, Shniekat N, Jawabreh O, and Al Omary R (2021c). Artificial intelligence (AI) and the impact of enhancing the consistency and interpretation of financial statement in the classified hotels in Aqaba, Jordan. Academy of Strategic Management Journal, 20(3): 1-18. [Google Scholar]

- Saleh MMA and Jawabreh OA (2020). Role of environmental awareness in the application of environmental accounting disclosure in tourism and hotel companies and its impact on investor’s decisions in Amman stock exchange. International Journal of Energy Economics and Policy, 10(2): 417-426. https://doi.org/10.32479/ijeep.8608 [Google Scholar]

- Saleh MMA, Jawabreh O, and Abu-Eker EFM (2021b). Factors of applying creative accounting and its impact on the quality of financial statements in Jordanian hotels, sustainable practices. Journal of Sustainable Finance and Investment, 13(1): 499-515. https://doi.org/10.1080/20430795.2021.1962662 [Google Scholar]

- Saleh MMA, Jawabreh OA, Al-Amro SAH, and Saleh HMI (2021a). Requirements for enhancing the standard of accounting education and its alignment with labor market requirements a case study hospitality and industrial sector in Jordan. Journal of Sustainable Finance and Investment, 13(1): 176-193. https://doi.org/10.1080/20430795.2021.1891781 [Google Scholar]

- Shibly M, Alawamleh HA, Nawaiseh KA, Ali BJ, Almasri A, and Alshibly E (2021). The relationship between administrative empowerment and continuous improvement: An empirical study. Revista Geintec-Gestao Inovacao E Tecnologias, 11(2): 1681-1699. [Google Scholar]

- Shniekat N, Jawabreh O, and Saleh MMA (2021). Efficiency and effect on the competitive advantage of management information systems (MIS) in classified hotels in the city of Petra; type of management as moderator. Academy of Strategic Management Journal, 20: 1-18. [Google Scholar]

- Tabachnick BG and Fidell LS (2013). Using multivariate statistics: International edition. Pearson Education, Boston, USA. [Google Scholar]

- Wakaba R (2014). Effect of audit committee characteristics on financial performance of companies listed at the Nairobi securities exchange. M.Sc. Thesis, University of Nairobi, Nairobi, Kenya. [Google Scholar]