International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 10, Issue 11 (November 2023), Pages: 1-13

----------------------------------------------

Original Research Paper

The influence of board of directors’ characteristics on corporate social responsibility disclosures in Jordanian Islamic banks

Author(s):

Affiliation(s):

1Faculty of Economics and Muamalat (FEM), Universiti Sains Islam Malaysia (USIM), Nilai, Negeri Sembilan, Malaysia

2Business School, German Jordanian University, Amman, Jordan

3Faculty of Business, Amman Arab University, Amman, Jordan

4Faculty of Business, Yarmouk University, Irbid, Jordan

Full text

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0746-912X

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0746-912X

Digital Object Identifier (DOI)

https://doi.org/10.21833/ijaas.2023.11.001

Abstract

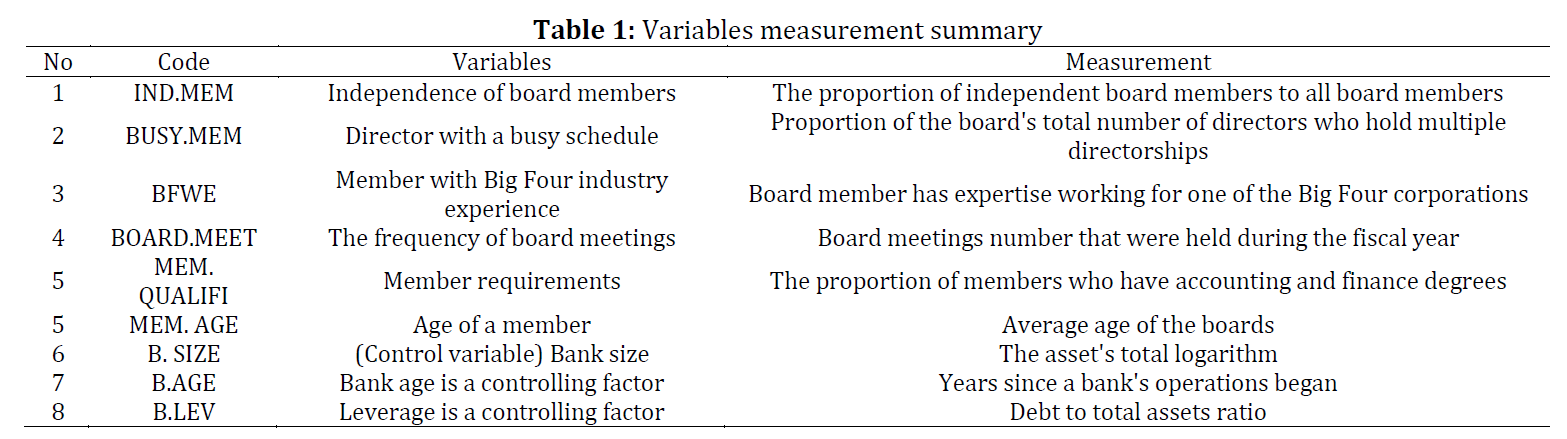

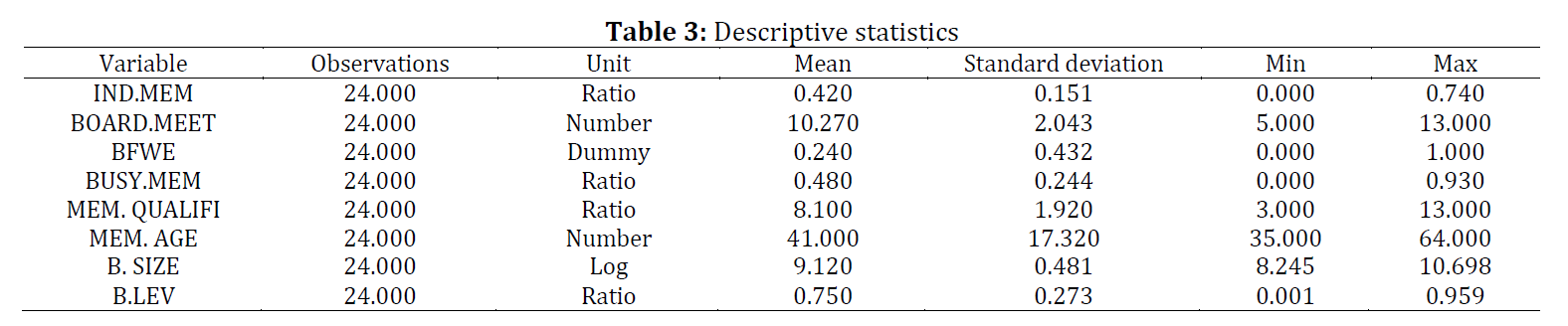

In an era where organizations are increasingly recognizing the paramount importance of addressing societal and environmental concerns, corporate social responsibility (CSR) has emerged as a pivotal facet of contemporary business practices. Within the banking sector, Islamic banks assume a significant role in advocating ethical and socially responsible conduct. This study delves into the impact of the board of directors' characteristics on corporate social responsibility disclosures (CSRD) within Jordanian Islamic banks. Data were meticulously gathered from three Jordanian Islamic banks, all of which are listed on the Amman Stock Exchange (ASE), over the span of the years 2010 to 2022. Our findings illuminate that Jordanian Islamic banks, on average, disclose 47 percent of their CSR endeavors, marking a commendable level of transparency, particularly when contrasted with less developed economies. Notably, independent directors comprise 42% of the board composition, with the average age of board members standing at 41 years. Moreover, 8.10% of board members hold degrees in finance and accounting, while 0.24% possess professional experience within the Big Four accounting firms. On average, Jordanian Islamic banks convene 10.27 board meetings annually, and 48% of directors maintain multiple directorships. Significantly, our analysis underscores that all examined characteristics of board members have a favorable influence on CSR disclosure within Jordanian Islamic banks. This paper constitutes a substantial contribution to the extant literature by providing empirical substantiation of the nexus between the board of directors' characteristics and CSRD in Jordanian Islamic banks, with a specific emphasis on the unique domain of Islamic banking, which has hitherto received limited scholarly attention. Further avenues of research are recommended to explore additional variables and delve deeper into the intricate interplay between board characteristics, external contextual factors, and the disclosure of CSR activities.

© 2023 The Authors. Published by IASE.

This is an

Keywords

Corporate social responsibility disclosures, Islamic banks, Board of directors, Jordanian banking sector, Ethical practices, Transparency

Article history

Received 12 June 2023, Received in revised form 1 October 2023, Accepted 11 October 2023

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Al-Zaqeba MAA, Shubailat OM, Abdul Hamid S, Jarah BAF, Ababneh FAT, and Almatarneh Z (2023). The influence of board of directors’ characteristics on corporate social responsibility disclosures in Jordanian Islamic banks. International Journal of Advanced and Applied Sciences, 10(11): 1-13

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (79)

- Akdoğan N, Gülhan O, and Aktaş M (2017). The relationship between corporate social responsibility reporting and corporate governance: Evidence from Turkish banking sector. Journal of Modern Accounting and Auditing, 13(5): 181-195. https://doi.org/10.17265/1548-6583/2017.05.001 [Google Scholar]

- Aksenov G, Li R, Abbas Q, Fambo H, Popkov S, Ponkratov V, Kosov M, Elyakova I, and Vasiljeva M (2023). Development of trade and financial-economical relationships between China and Russia: A study based on the trade gravity model. Sustainability, 15(7): 6099. https://doi.org/10.3390/su15076099 [Google Scholar]

- Alawaqleh QA, Almasria NA, and Alsawalhah JM (2021). The effect of board of directors and CEO on audit quality: Evidence from listed manufacturing firms in Jordan. The Journal of Asian Finance, Economics and Business, 8(2): 243-253. [Google Scholar]

- Alfraih MM and Almutawa AM (2017). Voluntary disclosure and corporate governance: Empirical evidence from Kuwait. International Journal of Law and Management, 59(2): 217-236. https://doi.org/10.1108/IJLMA-10-2015-0052 [Google Scholar]

- AlQudah AM, Azzam MJ, Haija AAA, and AlSmadi SA (2020). The role of ownership map in constraining discretionary loan loss-provisions decisions in Jordanian banks. Cogent Business and Management, 7(1): 1752604. https://doi.org/10.1080/23311975.2020.1752604 [Google Scholar]

- Alrabba HM, Haija AAA, AlQudah AM, and Azzam MJ (2018). The mediating role of foreign ownership in the relationship between board characteristics and voluntary disclosures of Jordanian banks. Academy of Accounting and Financial Studies Journal, 22(6): 1-16. [Google Scholar]

- Al-Zaqeba MA, Hamid SA, and Muhammad I (2018). Tax compliance of individual taxpayers: A systematic literature review. International Journal of Management and Applied Science, 4(6): 47-57. [Google Scholar]

- Al-Zaqeba MAA and Al-Rashdan MT (2020). Extension of the TPB in tax compliance behavior: The role of moral intensity and customs tax. International Journal of Scientific and Technology Research, 9(4): 227-232. [Google Scholar]

- Al-Zaqeba MAA, Jarah BAF, Ineizeh NI, Almatarneh Z, and Jarrah MAL (2022). The effect of management accounting and blockchain technology characteristics on supply chains efficiency. Uncertain Supply Chain Management, 10(3): 973-982. https://doi.org/10.5267/j.uscm.2022.2.016 [Google Scholar]

- Alzaqebah M, Jawarneh S, Mohammad RM, Alsmadi MK, Al-Marashdeh I, Ahmed EA, Alrefai N, and Alghamdi FA (2021). Hybrid feature selection method based on particle swarm optimization and adaptive local search method. International Journal of Electrical and Computer Engineering, 11(3): 2414.-2422. https://doi.org/10.11591/ijece.v11i3.pp2414-2422 [Google Scholar]

- Ananzeh H, Al Shbail MO, Al Amosh H, Khatib SF, and Abualoush SH (2023). Political connection, ownership concentration, and corporate social responsibility disclosure quality (CSRD): Empirical evidence from Jordan. International Journal of Disclosure and Governance, 20(1): 83-98. https://doi.org/10.1057/s41310-022-00167-z [Google Scholar] PMCid:PMC9769480

- Aramburu IA and Pescador IG (2019). The effects of corporate social responsibility on customer loyalty: The mediating effect of reputation in cooperative banks versus commercial banks in the Basque country. Journal of Business Ethics, 154: 701-719. https://doi.org/10.1007/s10551-017-3438-1 [Google Scholar]

- Benvolio J and Ironkwe UI (2022). Board composition and firm performance of quoted commercial banks in Nigeria. GPH-International Journal of Business Management, 5(1): 19-40. [Google Scholar]

- Binford LR (2019). Constructing frames of reference: An analytical method for archaeological theory building using ethnographic and environmental data sets. University of California Press, Berkeley, USA. [Google Scholar]

- Bukair AA and Rahman AA (2015). The effect of the board of directors' characteristics on corporate social responsibility disclosure by Islamic banks. Journal of Management Research, 7(2): 506-519. https://doi.org/10.5296/jmr.v7i2.6989 [Google Scholar]

- Carnini Pulino S, Ciaburri M, Magnanelli BS, and Nasta L (2022). Does ESG disclosure influence firm performance? Sustainability, 14(13): 7595. https://doi.org/10.3390/su14137595 [Google Scholar]

- Carroll AB, and Brown J (2022). Business and society: Ethics, sustainability and stakeholder management. Cengage Learning, Boston, USA. [Google Scholar]

- Chintrakarn P, Jiraporn P, Kim JC, and Kim YS (2016). The effect of corporate governance on corporate social responsibility. Asia‐Pacific Journal of Financial Studies, 45(1): 102-123. https://doi.org/10.1111/ajfs.12121 [Google Scholar]

- Dwekat A, Seguí-Mas E, Zaid MA, and Tormo-Carbó G (2022). Corporate governance and corporate social responsibility: Mapping the most critical drivers in the board academic literature. Meditari Accountancy Research, 30(6): 1705-1739. https://doi.org/10.1108/MEDAR-01-2021-1155 [Google Scholar]

- Elsakit OM and Worthington AC (2014). The impact of corporate characteristics and corporate governance on corporate social and environmental disclosure: A literature review. International Journal of Business and Management, 9(9): 1-15. https://doi.org/10.5539/ijbm.v9n9p1 [Google Scholar]

- Fernández‐Gago R, Cabeza‐García L, and Nieto M (2018). Independent directors' background and CSR disclosure. Corporate Social Responsibility and Environmental Management, 25(5): 991-1001. https://doi.org/10.1002/csr.1515 [Google Scholar]

- Ferrell OC, Harrison DE, Ferrell L, and Hair JF (2019). Business ethics, corporate social responsibility, and brand attitudes: An exploratory study. Journal of Business Research, 95: 491-501. https://doi.org/10.1016/j.jbusres.2018.07.039 [Google Scholar]

- Flammer C (2018). Competing for government procurement contracts: The role of corporate social responsibility. Strategic Management Journal, 39(5): 1299-1324. https://doi.org/10.1002/smj.2767 [Google Scholar]

- Fuente JA, García-Sanchez IM, and Lozano MB (2017). The role of the board of directors in the adoption of GRI guidelines for the disclosure of CSR information. Journal of Cleaner Production, 141: 737-750. https://doi.org/10.1016/j.jclepro.2016.09.155 [Google Scholar]

- Galant A and Cadez S (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research-Ekonomska Istraživanja, 30(1): 676-693. https://doi.org/10.1080/1331677X.2017.1313122 [Google Scholar]

- Gangi F, Daniele LM, D'Angelo E, Varrone N, and Coscia M (2023). The impact of board gender diversity on banks' environmental policy: The moderating role of gender inequality in national culture. Corporate Social Responsibility and Environmental Management, 30(3): 1273-1291. https://doi.org/10.1002/csr.2418 [Google Scholar]

- García Martín CJ and Herrero B (2020). Do board characteristics affect environmental performance? A study of EU firms. Corporate Social Responsibility and Environmental Management, 27(1): 74-94. https://doi.org/10.1002/csr.1775 [Google Scholar]

- Georgiadou E and Nickerson C (2022). Marketing strategies in communicating CSR in the Muslim market of the United Arab Emirates: Insights from the banking sector. Journal of Islamic Marketing, 13(7): 1417-1435. https://doi.org/10.1108/JIMA-09-2020-0274 [Google Scholar]

- Godos-Díez JL, Cabeza-Garcia L, Alonso-Martínez D, and Fernández-Gago R (2018). Factors influencing board of directors’ decision-making process as determinants of CSR engagement. Review of Managerial Science, 12: 229-253. https://doi.org/10.1007/s11846-016-0220-1 [Google Scholar]

- Gul FA, Lin B, Yang Z, Zhang M, and Zhu H (2024). Accounting personnel quality, audit risk, and auditor responses. Auditing: A Journal of Practice and Theory. https://doi.org/10.2308/AJPT-2020-119 [Google Scholar]

- Gulzar S, Mujtaba Kayani G, Xiaofen H, Ayub U, and Rafique A (2019). Financial cointegration and spillover effect of global financial crisis: A study of emerging Asian financial markets. Economic Research-Ekonomska Istraživanja, 32(1): 187-218. https://doi.org/10.1080/1331677X.2018.1550001 [Google Scholar]

- Hair JF, Black WC, and Babin BB (2006). Multivariate data analysis with readings. Pearson Education, Upper Saddle River, USA. [Google Scholar]

- Hamour H, ALensou J, Abuzaid A, Alheet A, Madadha S, and Al-Zaqeba M (2023). The effect of strategic intelligence, effective decision-making and strategic flexibility on logistics performance. Uncertain Supply Chain Management, 11(2): 657-664. https://doi.org/10.5267/j.uscm.2023.1.015 [Google Scholar]

- Haniffa RM and Cooke TE (2002). Culture, corporate governance and disclosure in Malaysian corporations. ABACUS, 38(3): 317-349. https://doi.org/10.1111/1467-6281.00112 [Google Scholar]

- Harris IC and Shimizu K (2004). Too busy to serve? An examination of the influence of overboarded directors. Journal of Management Studies, 41(5): 775-798. https://doi.org/10.1111/j.1467-6486.2004.00453.x [Google Scholar]

- Herremans D, Chuan CH, and Chew E (2017). A functional taxonomy of music generation systems. ACM Computing Surveys, 50(5): 69. https://doi.org/10.1145/3108242 [Google Scholar]

- Ishaq MI, Sarwar H, Franzoni S, and Palermo O (2023). The nexus of human resource management, corporate social responsibility and sustainable performance in upscale hotels: A mixed-method study. The International Journal of Emerging Markets, 32(11): 2493-2518. https://doi.org/10.1108/IJOEM-04-2022-0714 [Google Scholar]

- Jarah BAF, AL Jarrah MA, Al-Zaqeba MA, and Al-Jarrah MFM (2022). The role of internal audit to reduce the effects of creative accounting on the reliability of financial statements in the Jordanian Islamic banks. International Journal of Financial Studies, 10(3): 60. https://doi.org/10.3390/ijfs10030060 [Google Scholar]

- Jensen MC and Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3: 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [Google Scholar]

- Jizi MI, Salama A, Dixon R, and Stratling R (2014). Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. Journal of business ethics, 125: 601-615. https://doi.org/10.1007/s10551-013-1929-2 [Google Scholar]

- Johl SK, Kaur S, and Cooper BJ (2015). Board characteristics and firm performance: Evidence from Malaysian public listed firms. Journal of Economics, Business and Management, 3(2): 239-243. https://doi.org/10.7763/JOEBM.2015.V3.187 [Google Scholar]

- Junaidi J (2021). The awareness and attitude of Muslim consumer preference: The role of religiosity. Journal of Islamic Accounting and Business Research, 12(6): 919-938. https://doi.org/10.1108/JIABR-08-2020-0250 [Google Scholar]

- Katmon N, Mohamad ZZ, Norwani NM, and Farooque OA (2019). Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. Journal of Business Ethics, 157: 447-481. https://doi.org/10.1007/s10551-017-3672-6 [Google Scholar]

- Khan MT, Khan NA, Ahmed S, and Ali M (2012). Corporate social responsibility (CSR)–Definition, concepts and scope. Universal Journal of Management and Social Sciences, 2(7): 41-52. [Google Scholar]

- Kiliç M (2016). Online corporate social responsibility (CSR) disclosure in the banking industry: Evidence from Turkey. International Journal of Bank Marketing, 34(4): 550-569. https://doi.org/10.1108/IJBM-04-2015-0060 [Google Scholar]

- Kim JH (2019). Multicollinearity and misleading statistical results. Korean Journal of Anesthesiology, 72(6): 558-569. https://doi.org/10.4097/kja.19087 [Google Scholar] PMid:31304696 PMCid:PMC6900425

- Kravet T and Muslu V (2013). Textual risk disclosures and investors’ risk perceptions. Review of Accounting Studies, 18: 1088-1122. https://doi.org/10.1007/s11142-013-9228-9 [Google Scholar]

- Ma Y, Zhang Q, Yin Q, and Wang B (2019). The influence of top managers on environmental information disclosure: The moderating effect of company’s environmental performance. International Journal of Environmental Research and Public Health, 16(7): 1167. https://doi.org/10.3390/ijerph16071167 [Google Scholar] PMid:30939767 PMCid:PMC6479823

- Makki TW, O'Neal LJ, Cotten SR, and Rikard RV (2018). When first-order barriers are high: A comparison of second-and third-order barriers to classroom computing integration. Computers and Education, 120: 90-97. https://doi.org/10.1016/j.compedu.2018.01.005 [Google Scholar]

- Malkawi R, Alzaqebah M, Al-Yousef A, and Abul-Huda B (2019). The impact of the digital storytelling rubrics on the social media engagements. International Journal of Computer Applications in Technology, 59(3): 269-275. https://doi.org/10.1504/IJCAT.2019.10020111 [Google Scholar]

- Maswadi L and Amran A (2023). Does board capital enhance corporate social responsibility disclosure quality? The role of CEO power. Corporate Social Responsibility and Environmental Management, 30(1): 209-225. https://doi.org/10.1002/csr.2349 [Google Scholar]

- Matuszak Ł, Różańska E, and Macuda M (2019). The impact of corporate governance characteristics on banks’ corporate social responsibility disclosure: Evidence from Poland. Journal of Accounting in Emerging Economies, 9(1): 75-102. https://doi.org/10.1108/JAEE-04-2017-0040 [Google Scholar]

- Naciti V (2019). Corporate governance and board of directors: The effect of a board composition on firm sustainability performance. Journal of Cleaner Production, 237: 117727. https://doi.org/10.1016/j.jclepro.2019.117727 [Google Scholar]

- Nour AI, Sharabati AAA, and Hammad KM (2020). Corporate governance and corporate social responsibility disclosure. International Journal of Sustainable Entrepreneurship and Corporate Social Responsibility (IJSECSR), 5(1): 20-41. https://doi.org/10.4018/IJSECSR.2020010102 [Google Scholar]

- Orazalin N (2019). Corporate governance and corporate social responsibility (CSR) disclosure in an emerging economy: evidence from commercial banks of Kazakhstan. Corporate Governance: The International Journal of Business in Society, 19(3): 490-507. https://doi.org/10.1108/CG-09-2018-0290 [Google Scholar]

- Post C, Rahman N, and Rubow E (2011). Green governance: Boards of directors’ composition and environmental corporate social responsibility. Business and Society, 50(1): 189-223. https://doi.org/10.1177/0007650310394642 [Google Scholar]

- Qa’dan MBA, and Suwaidan MS (2018). Board composition, ownership structure and corporate social responsibility disclosure: The case of Jordan. Social Responsibility Journal, 15(1): 28-46. https://doi.org/10.1108/SRJ-11-2017-0225 [Google Scholar]

- Qasim YR, Ibrahim N, Sapian SM, and Al-Zaqeba MA (2017). Measurement the performance levels of Islamic banks in Jordan. Journal of Public Administration and Governance, 7(3): 75-87. https://doi.org/10.5296/jpag.v7i3.11451 [Google Scholar]

- Ramdhony D (2017). The influence of corporate governance practices on corporate social responsibility (CSR) reporting-Evidence from Mauritius. Ph.D. Dissertation, University of Southern Queensland, Toowoomba, Australia. [Google Scholar]

- Rettab B and Mellahi K (2019). CSR and corporate performance with special reference to the Middle East. In: Rettab B and Mellahi K (Eds.), Practising CSR in the Middle East: 101-118. Palgrave Macmillan, Cham, Switzerland. https://doi.org/10.1007/978-3-030-02044-6_6 [Google Scholar]

- Saha A, Morris RD, and Kang H (2019). Disclosure overload? An empirical analysis of international financial reporting standards disclosure requirements. ABACUS, 55(1): 205-236. https://doi.org/10.1111/abac.12148 [Google Scholar]

- Sahoo M, Srivastava KB, Gupta N, Mittal SK, Bakhshi P, and Agarwal T (2023). Board meeting, promoter CEO and firm performance: Evidence from India. Cogent Economics and Finance, 11(1): 2175465. https://doi.org/10.1080/23322039.2023.2175465 [Google Scholar]

- Said R, Hj Zainuddin Y, and Haron H (2009). The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Social Responsibility Journal, 5(2): 212-226. https://doi.org/10.1108/17471110910964496 [Google Scholar]

- Saleh MW, Zaid MA, Shurafa R, Maigoshi ZS, Mansour M, and Zaid A (2021). Does board gender enhance Palestinian firm performance? The moderating role of corporate social responsibility. Corporate Governance: The International Journal of Business in Society, 21(4): 685-701. https://doi.org/10.1108/CG-08-2020-0325 [Google Scholar]

- Sharif M and Rashid K (2014). Corporate governance and corporate social responsibility (CSR) reporting: An empirical evidence from commercial banks (CB) of Pakistan. Quality and Quantity, 48: 2501-2521. https://doi.org/10.1007/s11135-013-9903-8 [Google Scholar]

- Simmons C, Rayson D, Joy AA, Henning JW, Lemieux J, McArthur H, Card PB, Dent R, and Brezden-Masley C (2022). Current and future landscape of targeted therapy in HER2-positive advanced breast cancer: Redrawing the lines. Therapeutic Advances in Medical Oncology, 14: 17588359211066677. https://doi.org/10.1177/17588359211066677 [Google Scholar] PMid:35035535 PMCid:PMC8753087

- Solikhah B, Wahyudin A, Al-Faryan MAS, Iranda NN, Hajawiyah A, and Sun CM (2022). Corporate governance mechanisms and earnings quality: Is firm size a moderation variable? Journal of Governance and Regulation, 11(1): 200-210. https://doi.org/10.22495/jgrv11i1siart1 [Google Scholar]

- Tiwari M, Tiwari T, Sam Santhose S, Mishra L, Mr R, and Sundararaj V (2023). Corporate social responsibility and supply chain: A study for evaluating corporate hypocrisy with special focus on stakeholders. International Journal of Finance and Economics, 28(2): 1391-1403. https://doi.org/10.1002/ijfe.2483 [Google Scholar]

- Tylka TL, Rodgers RF, Calogero RM, Thompson JK, and Harriger JA (2023). Integrating social media variables as predictors, mediators, and moderators within body image frameworks: Potential mechanisms of action to consider in future research. Body Image, 44: 197-221. https://doi.org/10.1016/j.bodyim.2023.01.004 [Google Scholar] PMid:36709634

- Vatcheva KP, Lee M, McCormick JB, and Rahbar MH (2016). Multicollinearity in regression analyses conducted in epidemiologic studies. Epidemiology (Sunnyvale, Calif.), 6(2): 227. https://doi.org/10.4172/2161-1165.1000227 [Google Scholar] PMid:27274911 PMCid:PMC4888898

- Venter ER and Van Eck L (2021). Research on extended external reporting assurance: Trends, themes, and opportunities. Journal of International Financial Management and Accounting, 32(1): 63-103. https://doi.org/10.1111/jifm.12125 [Google Scholar]

- Wang Q, Sun M, and Wang K (2023). Do reputation incentives matter? Busy directors and corporate social responsibility in China. Sustainability, 15(6): 4857. https://doi.org/10.3390/su15064857 [Google Scholar]

- Wang Q, Wu C, and Sun Y (2015). Evaluating corporate social responsibility of airlines using entropy weight and grey relation analysis. Journal of Air Transport Management, 42: 55-62. https://doi.org/10.1016/j.jairtraman.2014.08.003 [Google Scholar]

- Weisbach MS (1988). Outside directors and CEO turnover. Journal of Financial Economics, 20: 431-460. https://doi.org/10.1016/0304-405X(88)90053-0 [Google Scholar]

- Yu L, Wang D, and Wang Q (2018). The effect of independent director reputation incentives on corporate social responsibility: Evidence from China. Sustainability, 10(9): 3302. https://doi.org/10.3390/su10093302 [Google Scholar]

- Zahid RA, Taran A, Khan MK, and Chersan IC (2023). ESG, dividend payout policy and the moderating role of audit quality: Empirical evidence from Western Europe. Borsa Istanbul Review, 23(2): 350-367. https://doi.org/10.1016/j.bir.2022.10.012 [Google Scholar]

- Zhang FJ (2023). Political endorsement by Nature and trust in scientific expertise during COVID-19. Nature Human Behaviour, 7(5): 696-706. https://doi.org/10.1038/s41562-023-01537-5 [Google Scholar] PMid:36941467 PMCid:PMC10202798

- Zhang Z, Zhang H, Feng J, Wang Y, and Liu K (2021). Evaluation of social values for ecosystem services in urban riverfront space based on the solves model: A case study of the Feng He River, Xi’an, China. International Journal of Environmental Research and Public Health, 18(5): 2765. https://doi.org/10.3390/ijerph18052765 [Google Scholar] PMid:33803264 PMCid:PMC7967293

- Zobi M, Al-Zaqeba M, and Jarah B (2023). Taxation and customs strategies in Jordanian supply chain management: Shaping sustainable design and driving environmental responsibility. Uncertain Supply Chain Management, 11(4): 1859-1876. https://doi.org/10.5267/j.uscm.2023.6.005 [Google Scholar]