International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 9 (September 2022), Pages: 85-95

----------------------------------------------

Review Paper

Accounting systems, performance, and market orientation in Saudi Arabia SMEs

Author(s): Rim Zouaoui 1, *, Mohamed Ali Brahim Omri 2, Rabeb Hamdi 1

Affiliation(s):

1Marketing Department, Northern Border University, Arar, Saudi Arabia

2Accounting Department, Northern Border University, Arar, Saudi Arabia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-0554-6147

Corresponding author's ORCID profile: https://orcid.org/0000-0002-0554-6147

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.09.011

Abstract:

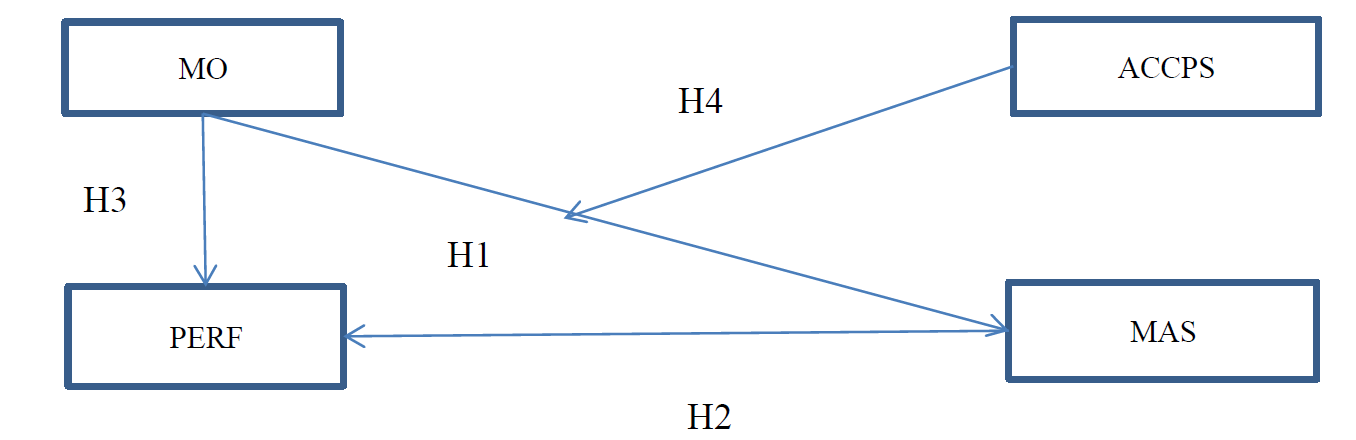

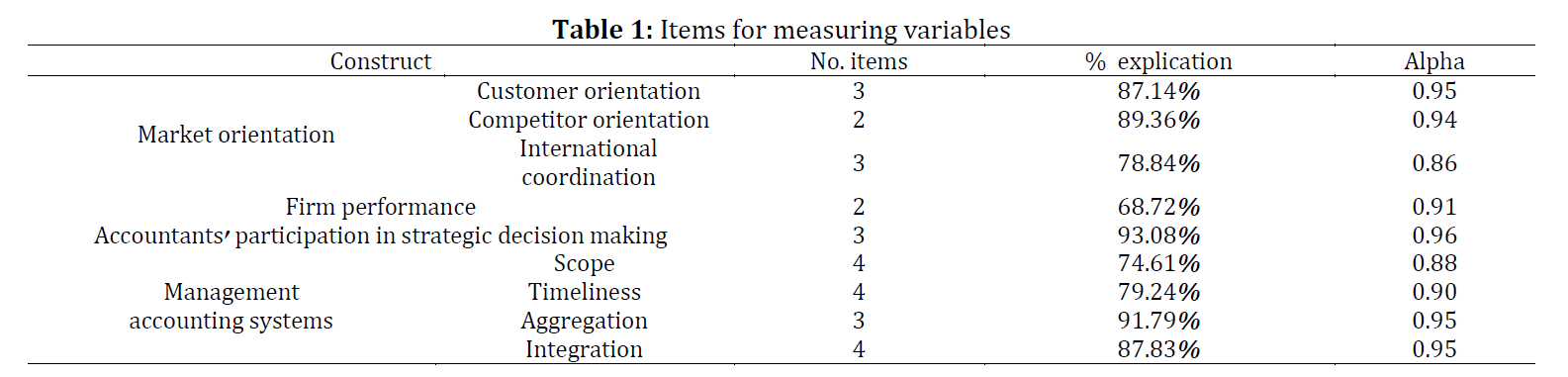

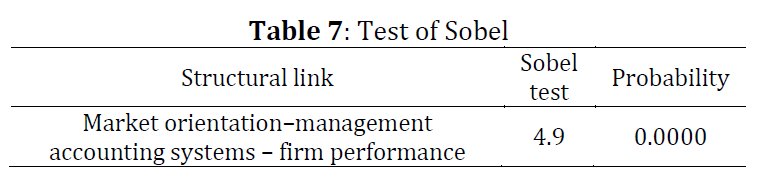

The main purpose of this paper is to test the impact of Market Orientations (MO) on the performance of Small and Medium Enterprises (SMEs) in Saudi Arabia. More specifically, first, we examine the relationship between MO and Management Accounting Systems (MAS) use. The use of MAS is known to affect performance. Second, we study the role of Accountants’ Participation in Strategic decision-making (ACCPS) applied in the relation between MO and MAS use. The data was collected via an electronic questionnaire distributed among a sample of managers operating in Saudi Arabia SMEs. The hypotheses were tested using structural equation modelling with data collected from 251 randomly selected SMEs. The results reveal that the MAS mediates the effect of market orientation on firm performance. They also indicate that the interaction among Market Orientations (MO) and Management Accounting Systems (MAS) use is increased by raising the Accountants' Participation in Strategic decision-making (ACCPS), which confirms a positive effect of the moderating variable. The implication of this research is to help Saudi companies achieve higher performance from MO (marketing variable) through the usage of accounting business processes (accounting variables).

© 2022 The Authors. Published by IASE.

This is an

Keywords: Accountants' participation, Management accounting systems, Market orientation, Performance, Saudi Arabia

Article History: Received 20 March 2022, Received in revised form 12 June 2022, Accepted 13 June 2022

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Zouaoui R, Omri MAB, and Hamdi R (2022). Accounting systems, performance, and market orientation in Saudi Arabia SMEs. International Journal of Advanced and Applied Sciences, 9(9): 85-95

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (71)

- Abdel-Kader M and Luther R (2008). The impact of firm characteristics on management accounting practices: A UK-based empirical analysis. The British Accounting Review, 40(1): 2-27. https://doi.org/10.1016/j.bar.2007.11.003 [Google Scholar]

- Abernethy MA and Bouwens J (2005). Determinants of accounting innovation implementation. Abacus, 41(3): 217-240. https://doi.org/10.1111/j.1467-6281.2005.00180.x [Google Scholar]

- Agbejule A (2005). The relationship between management accounting systems and perceived environmental uncertainty on managerial performance: A research note. Accounting and Business Research, 35(4): 295-305. https://doi.org/10.1080/00014788.2005.9729996 [Google Scholar]

- Ahmad K and Zabri SM (2015). Factors explaining the use of management accounting practices in Malaysian medium-sized firms. Journal of Small Business and Enterprise Development, 22(4): 762-781. https://doi.org/10.1108/JSBED-04-2012-0057 [Google Scholar]

- Ahmed I and Manab NA (2016). Moderating effects of board equity ownership on the relationship between enterprise risk management, regulatory compliance and firm performance: Evidence from Nigeria. International Journal of Economics, Management and Accounting, 24(2): 163-187. [Google Scholar]

- Akrout F (2018). Les méthodes des équations structurelles. 2nd Edition, Laboratoire de recherche Marketing, Sfax, Tunisia. [Google Scholar]

- Amran YA, Amran YM, Alyousef R, and Alabduljabbar H (2020). Renewable and sustainable energy production in Saudi Arabia according to Saudi Vision 2030; Current status and future prospects. Journal of Cleaner Production, 247: 119602. https://doi.org/10.1016/j.jclepro.2019.119602 [Google Scholar]

- Appelbaum D, Kogan A, Vasarhelyi M, and Yan Z (2017). Impact of business analytics and enterprise systems on managerial accounting. International Journal of Accounting Information Systems, 25: 29-44. https://doi.org/10.1016/j.accinf.2017.03.003 [Google Scholar]

- Attia STM (2013). Market orientation in an emerging economy–Egypt. Journal of Strategic Marketing, 21(3): 277-291. https://doi.org/10.1080/0965254X.2013.768690 [Google Scholar]

- Balodi KC (2014). Strategic orientation and organizational forms: An integrative framework. European Business Review, 26(2): 188-203. https://doi.org/10.1108/EBR-08-2013-0106 [Google Scholar]

- Bamfo BA and Kraa JJ (2019). Market orientation and performance of small and medium enterprises in Ghana: The mediating role of innovation. Cogent Business and Management, 6(1): 1605703. https://doi.org/10.1080/23311975.2019.1605703 [Google Scholar]

- Barney J (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1): 99-120. https://doi.org/10.1177/014920639101700108 [Google Scholar]

- Baron RM and Kenny DA (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6): 1173-1182. https://doi.org/10.1037/0022-3514.51.6.1173 [Google Scholar] PMid:3806354

- Bontis N (1998). Intellectual capital: An exploratory study that develops measures and models. Management Decision, 36(2): 6376. https://doi.org/10.1108/00251749810204142 [Google Scholar]

- Cadez S and Guilding C (2008). An exploratory investigation of an integrated contingency model of strategic management accounting. Accounting, Organizations and Society, 33(7-8): 836-863. https://doi.org/10.1016/j.aos.2008.01.003 [Google Scholar]

- Cadez S and Guilding C (2012). Strategy, strategic management accounting and performance: A configurational analysis. Industrial Management and Data Systems, 112 (3): 484-501. https://doi.org/10.1108/02635571211210086 [Google Scholar]

- Calantone RJ, Cavusgil ST, and Zhao Y (2002). Learning orientation, firm innovation capability, and firm performance. Industrial Marketing Management, 31(6): 515-524. https://doi.org/10.1016/S0019-8501(01)00203-6 [Google Scholar]

- Chenhall RH and Morris D (1986). The impact of structure, environment, and interdependence on the perceived usefulness of management accounting systems. Accounting Review, 61: 16-35. [Google Scholar]

- Chia YM (1995). Decentralization, management accounting system (MAS) information characteristics and their interaction effects on managerial performance: A Singapore study. Journal of Business Finance and Accounting, 22(6): 811-830. https://doi.org/10.1111/j.1468-5957.1995.tb00390.x [Google Scholar]

- Day GS and Wensley R (1988). Assessing advantage: A framework for diagnosing competitive superiority. Journal of Marketing, 52(2): 1-20. https://doi.org/10.1177/002224298805200201 [Google Scholar]

- Dess GG and Robinson Jr RB (1984). Measuring organizational performance in the absence of objective measures: The case of the privately‐held firm and conglomerate business unit. Strategic Management Journal, 5(3): 265-273. https://doi.org/10.1002/smj.4250050306 [Google Scholar]

- Dyer JH and Singh H (1998). The relational view: Cooperative strategy and sources of interorganizational competitive advantage. Academy of Management Review, 23(4): 660-679. https://doi.org/10.5465/amr.1998.1255632 [Google Scholar]

- Escandón-Barbosa D, Hernandez-Espallardo M, and Rodriguez A (2016). International market orientation and international outcomes. Global Economy Journal, 16(4): 669-696. https://doi.org/10.1515/gej-2015-0037 [Google Scholar]

- Fornell C and Larcker DF (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1): 39-50. https://doi.org/10.1177/002224378101800104 [Google Scholar]

- Fry TD, Steele DC, and Saladin BA (1995). The role of management accounting in the development of a manufacturing strategy. International Journal of Operations and Production Management, 15(12): 21-31. https://doi.org/10.1108/01443579510104475 [Google Scholar]

- Getz D and Carlsen J (2000). Characteristics and goals of family and owner-operated businesses in the rural tourism and hospitality sectors. Tourism Management, 21(6): 547-560. https://doi.org/10.1016/S0261-5177(00)00004-2 [Google Scholar]

- Giannelloni JL and Vernette É (2012). Études de marché. 5th Edition, Vuibert, Paris, France. [Google Scholar]

- Gotteland D, Haon C, and Gauthier C (2007). Market orientation: Synthesis and new theoretical directions. Recherche et Applications en Marketing, 22(1): 45-59. https://doi.org/10.1177/205157070702200103 [Google Scholar]

- Greenley GE (1995). Market orientation and company performance: Empirical evidence from UK companies. British Journal of Management, 6(1): 1-13. https://doi.org/10.1111/j.1467-8551.1995.tb00082.x [Google Scholar]

- Guilding C and McManus L (2002). The incidence, perceived merit and antecedents of customer accounting: An exploratory note. Accounting, Organizations and Society, 27(1-2): 45-59. https://doi.org/10.1016/S0361-3682(01)00030-7 [Google Scholar]

- Hagen B, Zucchella A, Larimo J, and Dimitratos P (2017). A taxonomy of strategic postures of international SMEs. European Management Review, 14(3): 265-285. https://doi.org/10.1111/emre.12109 [Google Scholar]

- Harris LC (2001). Market orientation and performance: Objective and subjective empirical evidence from UK companies. Journal of Management Studies, 38(1): 17-43. https://doi.org/10.1111/1467-6486.00226 [Google Scholar]

- Helgesen Ø (2007). Customer accounting and customer profitability analysis for the order handling industry-A managerial accounting approach. Industrial Marketing Management, 36(6): 757-769. https://doi.org/10.1016/j.indmarman.2006.06.002 [Google Scholar]

- Hinson RE, Abdul-Hamid IK, and Osabutey EL (2017). Investigating market orientation and positioning in star-rated hotels in Ghana. International Journal of Contemporary Hospitality Management, 29: 2629-2646. https://doi.org/10.1108/IJCHM-02-2016-0075 [Google Scholar]

- Ho KLP, Nguyen CN, Adhikari R, Miles MP, and Bonney L (2018). Exploring market orientation, innovation, and financial performance in agricultural value chains in emerging economies. Journal of Innovation and Knowledge, 3(3): 154-163. https://doi.org/10.1016/j.jik.2017.03.008 [Google Scholar]

- Homburg C and Pflesser C (2000). A multiple-layer model of market-oriented organizational culture: Measurement issues and performance outcomes. Journal of Marketing Research, 37(4): 449-462. https://doi.org/10.1509/jmkr.37.4.449.18786 [Google Scholar]

- Ismail K, Isa CR, and Mia L (2018). Market competition, lean manufacturing practices and the role of management accounting systems (MAS) information. Jurnal Pengurusan, 52: 47-61. https://doi.org/10.17576/pengurusan-2018-52-04 [Google Scholar]

- Jaworski BJ and Kohli AK (1993). Market orientation: Antecedents and consequences. Journal of Marketing, 57(3): 53-70. https://doi.org/10.1177/002224299305700304 [Google Scholar]

- Kohli AK and Jaworski BJ (1990). Market orientation: The construct, research propositions, and managerial implications. Journal of Marketing, 54(2): 1-18. https://doi.org/10.1177/002224299005400201 [Google Scholar]

- Liao SH, Chang WJ, Wu CC, and Katrichis JM (2011). A survey of market orientation research (1995–2008). Industrial Marketing Management, 40(2): 301-310. https://doi.org/10.1016/j.indmarman.2010.09.003 [Google Scholar]

- Lord BR (1996). Strategic management accounting: The emperor's new clothes? Management Accounting Research, 7(3): 347-366. https://doi.org/10.1006/mare.1996.0020 [Google Scholar]

- Lumpkin GT and Dess GG (1996). Clarifying the entrepreneurial orientation construct and linking it to performance. Academy of Management Review, 21(1): 135-172. https://doi.org/10.5465/amr.1996.9602161568 [Google Scholar]

- Ma Y and Tayles M (2009). On the emergence of strategic management accounting: An institutional perspective. Accounting and Business Research, 39(5): 473-495. https://doi.org/10.1080/00014788.2009.9663379 [Google Scholar]

- Mahmoud MA, Hinson RE, and Duut DM (2019). Market orientation and customer satisfaction: The role of service quality and innovation. International Journal of Business and Emerging Markets, 11(2): 144-167. https://doi.org/10.1504/IJBEM.2019.10022489 [Google Scholar]

- Mohammed BAH, Maelah R, and Amir AM (2019). Strategic management accounting information and performance of private hospitals in Malaysia. International Journal of Economics, Management and Accounting, 27(2): 473-502. [Google Scholar]

- Naranjo-Gil D and Hartmann F (2007). Management accounting systems, top management team heterogeneity and strategic change. Accounting, Organizations and Society, 32(7-8): 735-756. https://doi.org/10.1016/j.aos.2006.08.003 [Google Scholar]

- Naranjo-Gil D and van Rinsum M (2006). The effect of management style and management accounting system design on performance. Journal of Applied Management Accounting Research, 4(1): 33-44. [Google Scholar]

- Narver JC and Slater SF (1990). The effect of a market orientation on business profitability. Journal of Marketing, 54(4): 20-35. https://doi.org/10.1177/002224299005400403 [Google Scholar]

- Nguyen NP (2018). Performance implication of market orientation and use of management accounting systems: The moderating role of accountants’ participation in strategic decision making. Journal of Asian Business and Economic Studies, 25(1): 33-49. https://doi.org/10.1108/JABES-04-2018-0005 [Google Scholar]

- O'Cass A and Voola R (2011). Explications of political market orientation and political brand orientation using the resource-based view of the political party. Journal of Marketing Management, 27(5-6): 627-645. https://doi.org/10.1080/0267257X.2010.489831 [Google Scholar]

- Oliver L (1991). Accountants as business partners. Strategic Finance, 72(12): 40-42. [Google Scholar]

- Osuagwu L (2006). Market orientation in Nigerian companies. Marketing Intelligence and Planning, 24(6): 608-631. https://doi.org/10.1108/02634500610701681 [Google Scholar]

- Parker RJ and Kyj L (2006). Vertical information sharing in the budgeting process. Accounting, Organizations and Society, 31(1): 27-45. https://doi.org/10.1016/j.aos.2004.07.005 [Google Scholar]

- Pelham AM (2000). Market orientation and other potential influences on performance in small and medium-sized manufacturing firms. Journal of Small Business Management, 38(1): 48-67. [Google Scholar]

- Perrien J, Chéron EJ, and Zins M (1983). Recherche en marketing: Méthodes et décisions. G. Morin, Boucherville, Canada. [Google Scholar]

- Pierce B and O'Dea T (2003). Management accounting information and the needs of managers: Perceptions of managers and accountants compared. The British Accounting Review, 35(3): 257-290. https://doi.org/10.1016/S0890-8389(03)00029-5 [Google Scholar]

- Rahman R and Al-Borie HM (2021). Strengthening the Saudi Arabian healthcare system: Role of vision 2030. International Journal of Healthcare Management, 14(4): 1483-1491. https://doi.org/10.1080/20479700.2020.1788334 [Google Scholar]

- Rosenberg M (1968). The logic of survey analysis. Basic Books Inc., New York, USA. [Google Scholar]

- Roussel P and Wacheux F (2005). Management des ressources humaines: Méthodes de recherche en sciences humaines et sociales. De Boeck Supérieur, Brussels, Belgium. https://doi.org/10.3917/dbu.rouss.2005.01 [Google Scholar]

- Roussel P, Durrieu F, Campoy E, and El Akremi A (2002). Méthodes d'équations structurelles: Recherche et applications en gestion. Economica, Paris, France. [Google Scholar]

- Salindal NA, Ahmad MI, Abdullah K, and Ahmad BP (2018). A structural equation model of the halal certification and its business performance impact on food companies. International Journal of Economics, Management and Accounting, 26(1): 185-206. [Google Scholar]

- Sheikh AA, Shahzad A, and Ku Ishak A (2017). The impact of market orientation, top management support, use of e-marketing and technological opportunism on the firm performance: A mediated-moderation and moderated-mediation analysis. Abasyn Journal of Social Sciences, 10(2): 212-234. [Google Scholar]

- Smith KA, Vasudevan SP, and Tanniru MR (1996). Organizational learning and resource‐based theory: An integrative model. Journal of Organizational Change Management, 9(6): 41-53. https://doi.org/10.1108/09534819610150512 [Google Scholar]

- Solovida GT and Latan H (2017). Linking environmental strategy to environmental performance: Mediation role of environmental management accounting. Sustainability Accounting, Management and Policy Journal, 8(5): 595-619. https://doi.org/10.1108/SAMPJ-08-2016-0046 [Google Scholar]

- Tagliapietra S (2019). The impact of the global energy transition on MENA oil and gas producers. Energy Strategy Reviews, 26: 100397. https://doi.org/10.1016/j.esr.2019.100397 [Google Scholar]

- Toms S (2010). Value, profit and risk: Accounting and the resource‐based view of the firm. Accounting, Auditing and Accountability Journal, 23 (5): 647-670. https://doi.org/10.1108/09513571011054927 [Google Scholar]

- van Gils A (2005). Management and governance in Dutch SMEs. European Management Journal, 23(5): 583-589. https://doi.org/10.1016/j.emj.2005.09.013 [Google Scholar]

- Venkatraman N (1989). Strategic orientation of business enterprises: The construct, dimensionality, and measurement. Management Science, 35(8): 942-962. https://doi.org/10.1287/mnsc.35.8.942 [Google Scholar]

- Verhoef PC, Leeflang PS, Reiner J, Natter M, Baker W, Grinstein A, and Saunders J (2011). A cross-national investigation into the marketing department's influence within the firm: Toward initial empirical generalizations. Journal of International Marketing, 19(3): 59-86. https://doi.org/10.1509/jimk.19.3.59 [Google Scholar]

- Wesson T and De Figueiredo JN (2001). The importance of focus to market entrants: A study of microbrewery performance. Journal of Business Venturing, 16(4): 377-403. https://doi.org/10.1016/S0883-9026(99)00049-X [Google Scholar]

- Woodridge B and Floyd SW (1990). The strategy process, middle management involvement, and organisational performance. Strategic Management Journal, 11(3): 231-241. https://doi.org/10.1002/smj.4250110305 [Google Scholar]