International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 9 (September 2022), Pages: 17-24

----------------------------------------------

Original Research Paper

Zero capital depreciation point for Ukrainian commercial organizations

Author(s): Illia Morhachov 1, *, Olena Kuzmenko 2, Daria Zablodska 3

Affiliation(s):

1Volodymyr Dahl East Ukrainian National University, Luhansk, Ukraine

2Vadym Hetman Kyiv National Economic University, Kyiv, Ukraine

3State Organization V. Mamutov Institute of Economic and Legal Research of NAS of Ukraine, Kyiv, Ukraine

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-4347-3153

Corresponding author's ORCID profile: https://orcid.org/0000-0002-4347-3153

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.09.003

Abstract:

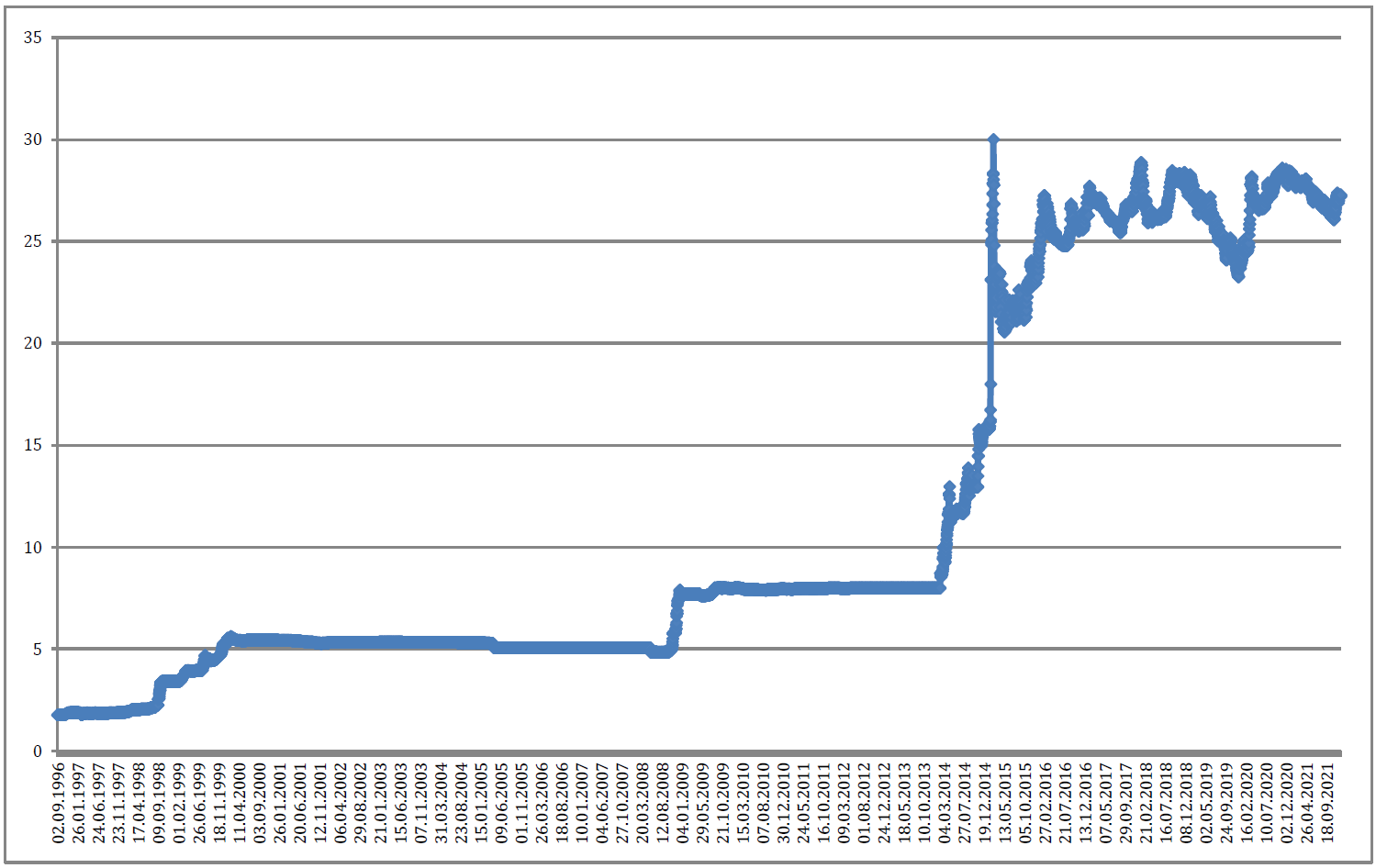

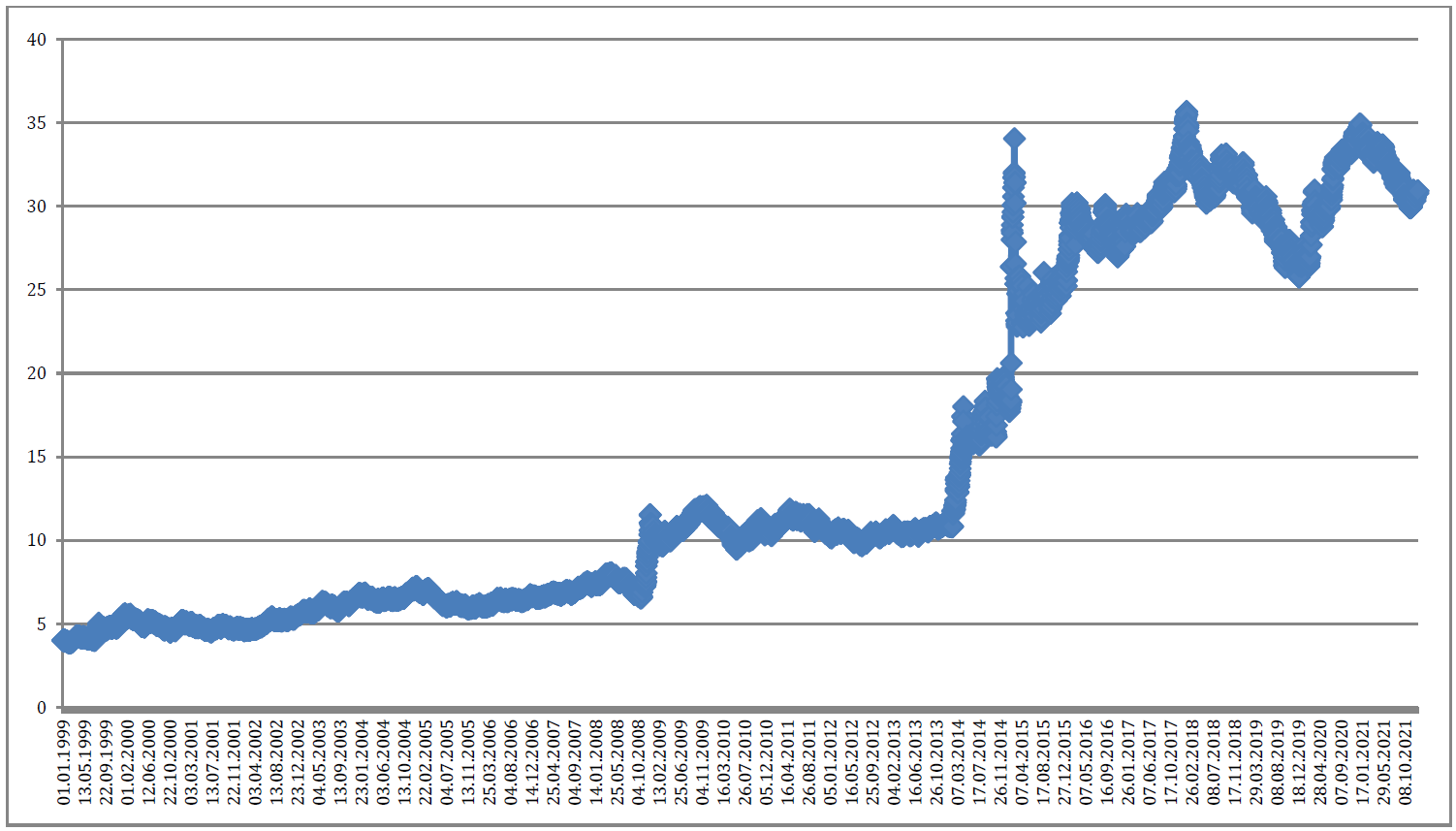

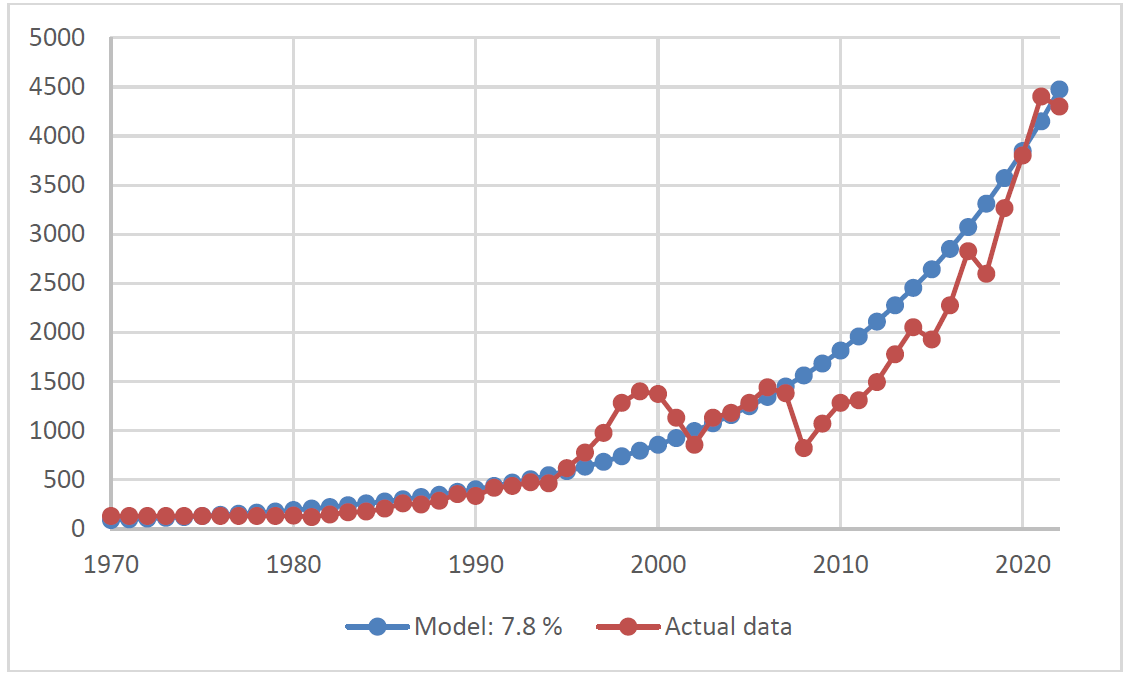

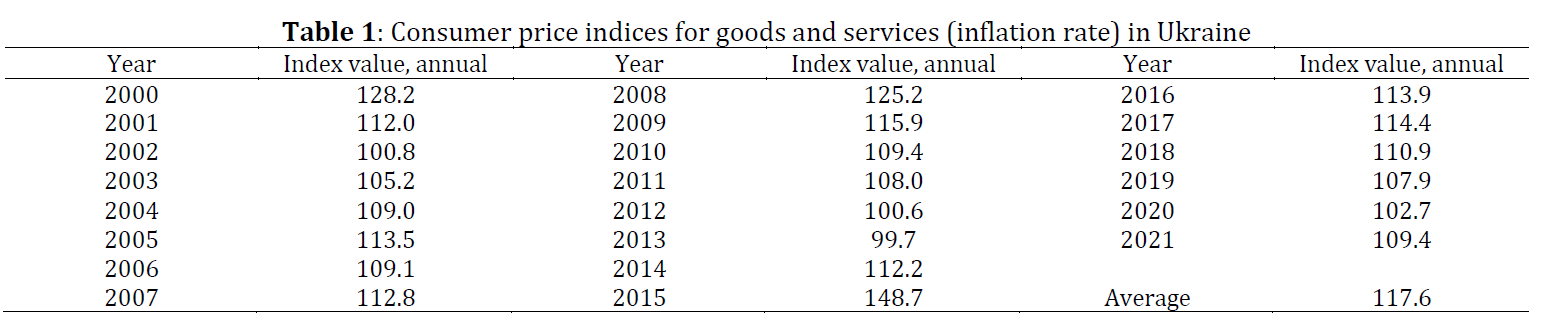

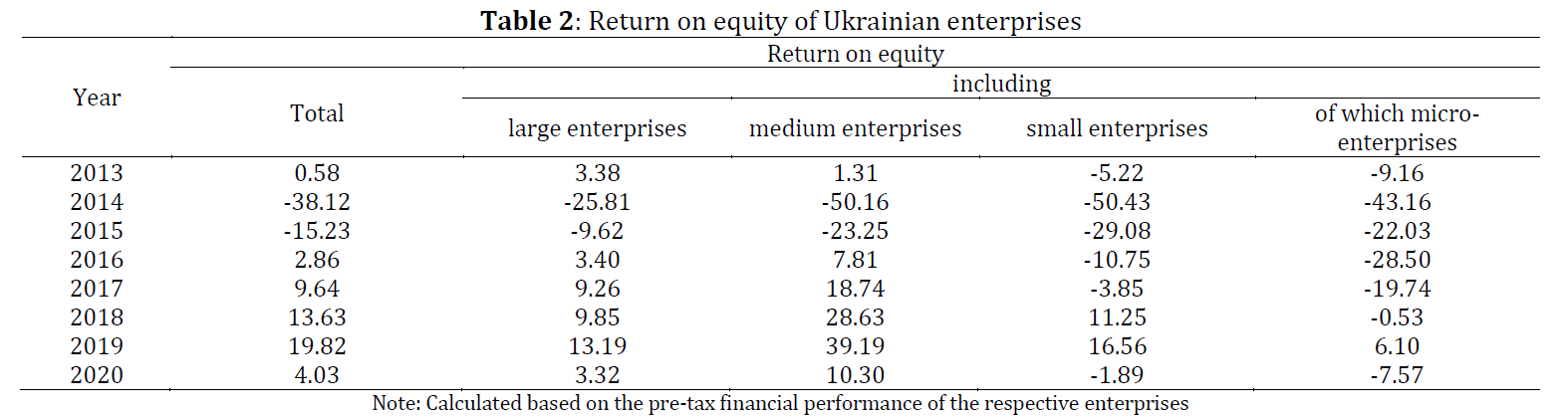

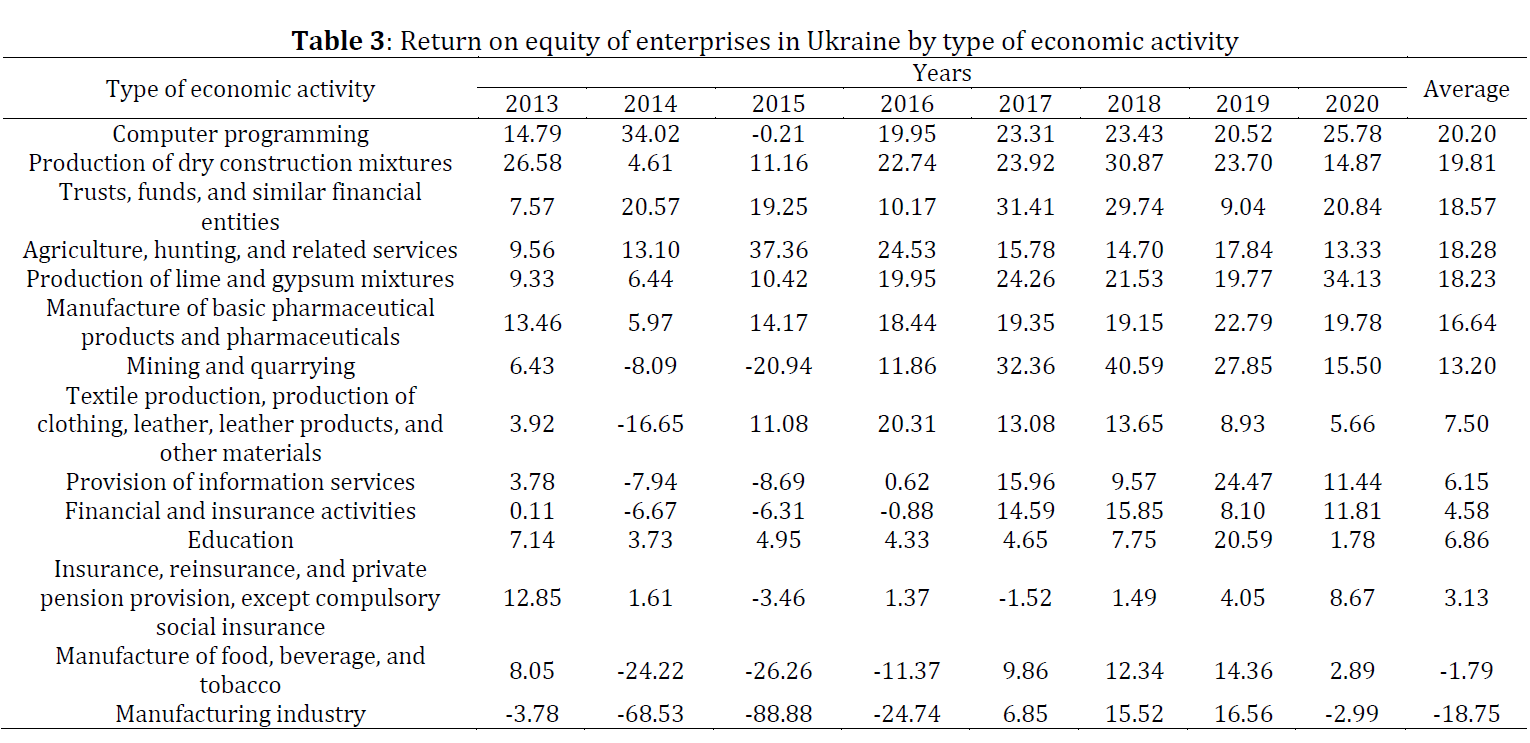

The problem of capital shortage for Ukrainian commercial organizations has been clarified, which makes the theoretical and methodological provisions of its increase and preservation relevant. Insufficient capital for investment processes is a significant obstacle to the development of most business entities in Ukraine. The analysis of recent research and publications on the topic of the work showed that the issues of tools for estimating the point of zero depreciation of equity for Ukrainian commercial organizations still have room for improvement. The aim of the work is to substantiate the tools for estimating the point of zero depreciation of equity for Ukrainian commercial organizations. The main source of compensation for the depreciation of equity due to inflation and devaluation of the national currency is the profit of the organization. The return on equity is a relative indicator that characterizes the degree of appropriate compensation. The tools for estimating the point of zero depreciation of equity should be considered as such a value of return on equity, which compensates for its depreciation due to various factors. Due to the need to divide the factors of impairment of equity into two groups, the use of two types of zero depreciation points is justified: Cash and alternative. As a widely used alternative to the use of equity for the average investor, investing in shares of ETFs is justified, completely repeating the US stock index S and P-500 with a long-term efficiency of 9.5% per annum in US dollars. Approbation of the presented valuation tools allowed us to determine that for Ukrainian commercial organizations the alternative point of zero depreciation of equity is 26.9% and cash-17.6%. It is specified that the average enterprise in the country does not reach the level of even a cash point. There are a limited number of economic activities in the country where the cash point of zero depreciation of equity is exceeded. Reducing inflation to 6-7% per year along with the stabilization of the national currency will bring a significant number of economic activities in the country to the level of reaching the cash point of depreciation of equity.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Return on equity, Inflation, Devaluation of the national currency, Opportunity losses, Stock index S and P-500

Article History: Received 15 February 2022, Received in revised form 15 May 2022, Accepted 30 May 2022

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Morhachov I, Kuzmenko O, and Zablodska D (2022). Zero capital depreciation point for Ukrainian commercial organizations. International Journal of Advanced and Applied Sciences, 9(9): 17-24

Figures

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (12)

- Ahmed F, Awais I, and Kashif M (2018). Financial leverage and firms’ performance: Empirical evidence from KSE-100 index. Etikonomi, 17(1): 45-56. https://doi.org/10.15408/etk.v17i1.6102 [Google Scholar]

- Bernier L (2014). Public enterprises as policy instruments: The importance of public entrepreneurship. Journal of Economic Policy Reform, 17(3): 253-266. https://doi.org/10.1080/17487870.2014.909312 [Google Scholar]

- Cheng H, Lu YC, and Sheu C (2009). An ontology-based business intelligence application in a financial knowledge management system. Expert Systems with Applications, 36(2): 3614-3622. https://doi.org/10.1016/j.eswa.2008.02.047 [Google Scholar]

- Fareed Z, Aziz S, Naz S, Shahzad F, Arshad M, and Amen U (2014). Testing the relationship between profitability and capital structure of textile industry of Pakistan. World Applied Sciences Journal, 29(5): 605-609. [Google Scholar]

- Graff Zivin J and Neidell M (2013). Environment, health, and human capital. Journal of Economic Literature, 51(3): 689-730. https://doi.org/10.3386/w18935 [Google Scholar]

- Klimek D (2020). Sustainable enterprise capital management. Economies, 8(1): 12. https://doi.org/10.3390/economies8010012 [Google Scholar]

- MacCarthaigh M (2011). Managing state-owned enterprises in an age of crisis: An analysis of Irish experience. Policy Studies, 32(3): 215-230. https://doi.org/10.1080/01442872.2011.561688 [Google Scholar]

- Purnamasari D (2015). The effect of changes in return on assets, return on equity, and economic value added to the stock price changes and its impact on earnings per share. Research Journal of Finance and Accounting, 6(6): 80-90. [Google Scholar]

- Rajan RG and Zingales L (1995). What do we know about capital structure? Some evidence from international data. The Journal of Finance, 50(5): 1421-1460. https://doi.org/10.1111/j.1540-6261.1995.tb05184.x [Google Scholar]

- Riepina IM, Vostriakova VY, Chukhraieva NM, and Bril MS (2018). M&A financial levers in management of business value. Financial and Credit Activity: Problems of Theory and Practice, 4(27): 222-230. https://doi.org/10.18371/fcaptp.v4i27.154197 [Google Scholar]

- Saluy AB, Abidin Z, Djamil M, Kemalasari N, Hutabarat L, Pramudena SM, and Endri E (2021). Employee productivity evaluation with human capital management strategy: The case of COVID-19 in Indonesia. Academy of Entrepreneurship Journal, 27(5): 1-9. [Google Scholar]

- Shubita MF and Alsawalhah JM (2012). The relationship between capital structure and profitability. International Journal of Business and Social Science, 3(16): 104-112. [Google Scholar]