International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 8 (August 2022), Pages: 136-143

----------------------------------------------

Original Research Paper

Technology valuation for intellectual property commercialization

Author(s): Heung Su Kim *

Affiliation(s):

Division of Convergence Business, Korea University, Seoul, South Korea

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7085-3269

Corresponding author's ORCID profile: https://orcid.org/0000-0001-7085-3269

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.08.017

Abstract:

This study was conducted to evaluate the technical value of 19 intellectual property rights held by the Korea Research Institute of Bioscience and Biotechnology, and the purpose of this valuation is to promote commercialization by acquiring the technology transfer or exclusive license for the intellectual property rights. This study examines the theoretical and practical aspects of the valuation methods and procedures of the income approach that are useful for valuing intellectual property. Assuming that bioscience and biotechnology firms receive license transfer of intellectual property held by a foreign company, the valuation analysis of intellectual property based on the profit approach is based on business plans and financial statements of domestic companies. After calculating the operating profit from the gross profit of the company in detail, the corporation tax and the capital cost are taken into account and the depreciation cost is increased or decreased to calculate the excess profit and multiply the present value by the present value. We propose an income approach model and a case analysis to obtain the ultimate value of intellectual property by multiplying the contribution by this factor. It is not easy to predict future cash flows and estimate various financial statements, and there is a limit to the possibility that the evaluator will be subject to the estimation of the appropriate discount rate. More detailed and partial complementary research classified by the industry size is to be left as a future study.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Income approach, Transfer and commercialization, License transfer, Intellectual property rights, Valuation

Article History: Received 27 December 2021, Received in revised form 15 May 2022, Accepted 23 May 2022

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Kim HS (2022). Technology valuation for intellectual property commercialization. International Journal of Advanced and Applied Sciences, 9(8): 136-143

Figures

No Figure

Tables

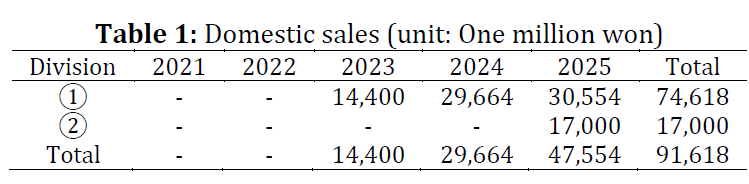

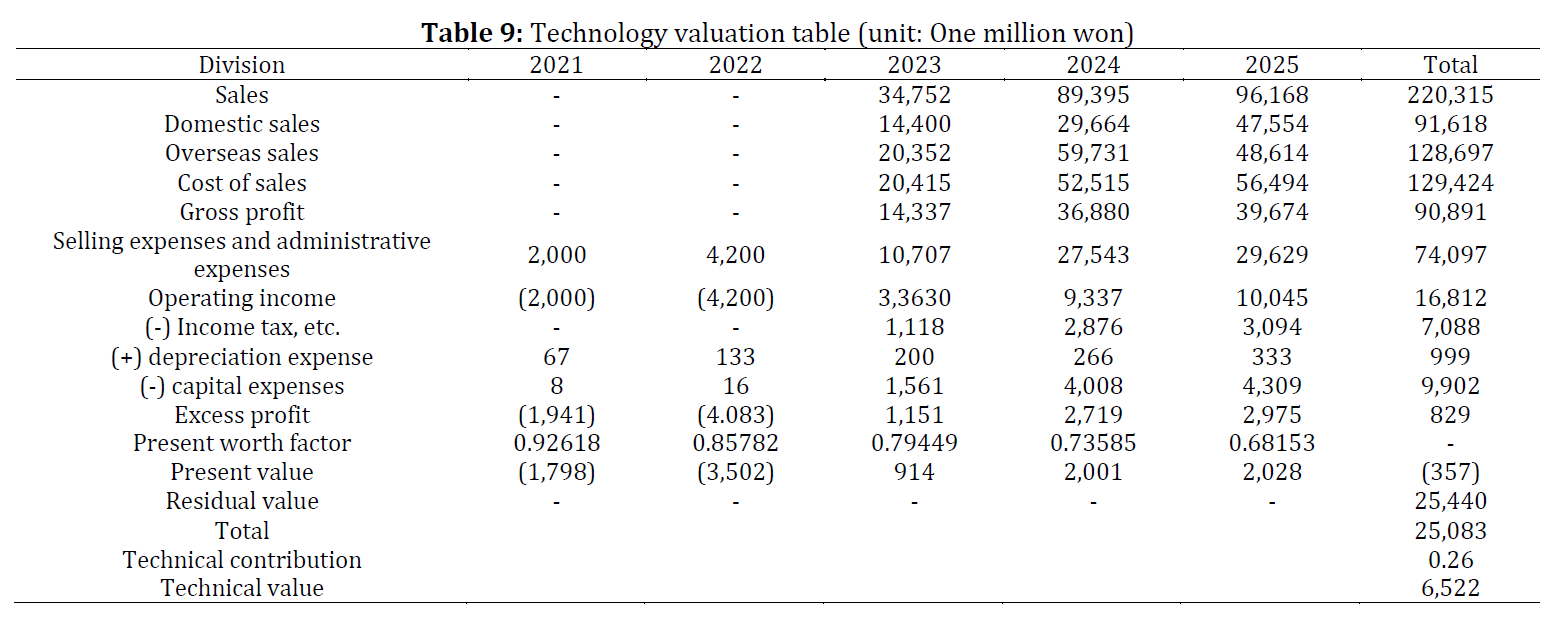

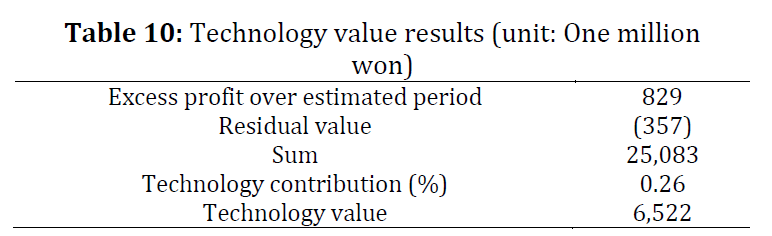

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9 Table 10

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (14)

- Baek DH, Sul W, Hong KP, and Kim H (2007). A technology valuation model to support technology transfer negotiations. R&D Management, 37(2): 123-138. https://doi.org/10.1111/j.1467-9310.2007.00462.x [Google Scholar]

- Bardhan I, Bagchi S, and Sougstad R (2004). A real options approach for prioritization of a portfolio of information technology projects: A case study of a utility company. In the 37th Annual Hawaii International Conference on System Sciences, IEEE, Big Island, USA: 1-11. https://doi.org/10.1109/HICSS.2004.1265499 [Google Scholar]

- Bodie Z, Merton RC, and Cleeton DL (2012). Financial economics. 2nd Edition, Pearson Learning Solutions, Boston, USA. [Google Scholar]

- Chiesa V, Frattini F, Gilardoni E, Manzini R, and Pizzurno E (2007). Searching for factors influencing technological asset value. European Journal of Innovation Management, 10(4): 467-488. https://doi.org/10.1108/14601060710828781 [Google Scholar]

- Lee DH (2010). Technology valuation factors for the commercialization of national R&D. Ph.D. Dissertation, Konkuk University, Seoul, South Korea. Available online at: https://scienceon.kisti.re.kr/srch/selectPORSrchArticle.do?cn=DIKO0011947419&dbt=DIKO#

- Lee M and Khoe KI (2015). Development method of digital content finance-focused on by technical value evaluation. Journal of the Korea Convergence Society, 6(6): 111-117. https://doi.org/10.15207/JKCS.2015.6.6.111 [Google Scholar]

- Mohammed S (2019). Research on financial risk prevention and control methods based on big data. International Journal of Smart Business and Technology, 7(2): 1-14. [Google Scholar]

- Oh HT (2015). A study on the effect of fair value hierarchy upon cost of capital through the convergence of market risk management and audit quality. Journal of the Korea Convergence Society, 6(5): 1-8. https://doi.org/10.15207/JKCS.2015.6.5.001 [Google Scholar]

- Park HW, Nah DB, and Park JK (2009). Proposition of a practical hybrid model for the valuation of technology. Management and Information Systems Review, 28(4): 27-44. https://doi.org/10.29214/damis.2009.28.4.002 [Google Scholar]

- Park Y and Park G (2004). A new method for technology valuation in monetary value: Procedure and application. Technovation, 24(5): 387-394. https://doi.org/10.1016/S0166-4972(02)00099-8 [Google Scholar]

- Reilly RF and Schweihs RP (1998). Valuing intangible assets. McGraw-Hill, New York, USA. [Google Scholar]

- Singh S (2019). Research on application of precision marketing based on big data. International Journal of Smart Business and Technology, 7(1): 17-26. https://doi.org/10.21742/IJSBT.2019.7.1.02 [Google Scholar]

- Xitiz U, Prashant B, and Ashish J (2017). Wine quality evaluation using machine learning algorithms. Asia-Pacific Journal of Convergent Research Interchange, 3(4): 1-9. https://doi.org/10.14257/apjcri.2017.12.07 [Google Scholar]

- Yoon D and Kim J (2019). A study on the changes in the appraisal industry in the era of the 4th industrial revolution-focus on the factors affecting intention to adopt big data in the appraisal field. International Journal of Smart Business and Technology, 7(1): 65-72. https://doi.org/10.21742/IJSBT.2019.7.1.07 [Google Scholar]