International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 8 (August 2022), Pages: 55-64

----------------------------------------------

Original Research Paper

The influence of female leadership on the cash holdings of listed companies in Vietnam

Author(s): Tan Nghiem Le 1, *, Long Hau Le 2, Bich Tuyen Duong 3, Anh Tran Thi Hoang 4, Viet Thanh Truc Tran 2, Thi Thanh Tam Nguyen 3

Affiliation(s):

1Department of Business Administration, School of Economics, Can Tho University, Can Tho, Vietnam

2Department of Finance and Banking, School of Economics, Can Tho University, Can Tho, Vietnam

3School of Economics, Nam Can Tho University, Can Tho, Vietnam

4State Bank of Vietnam, Kien Giang Branch, Hanoi, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-8332-6388

Corresponding author's ORCID profile: https://orcid.org/0000-0001-8332-6388

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.08.007

Abstract:

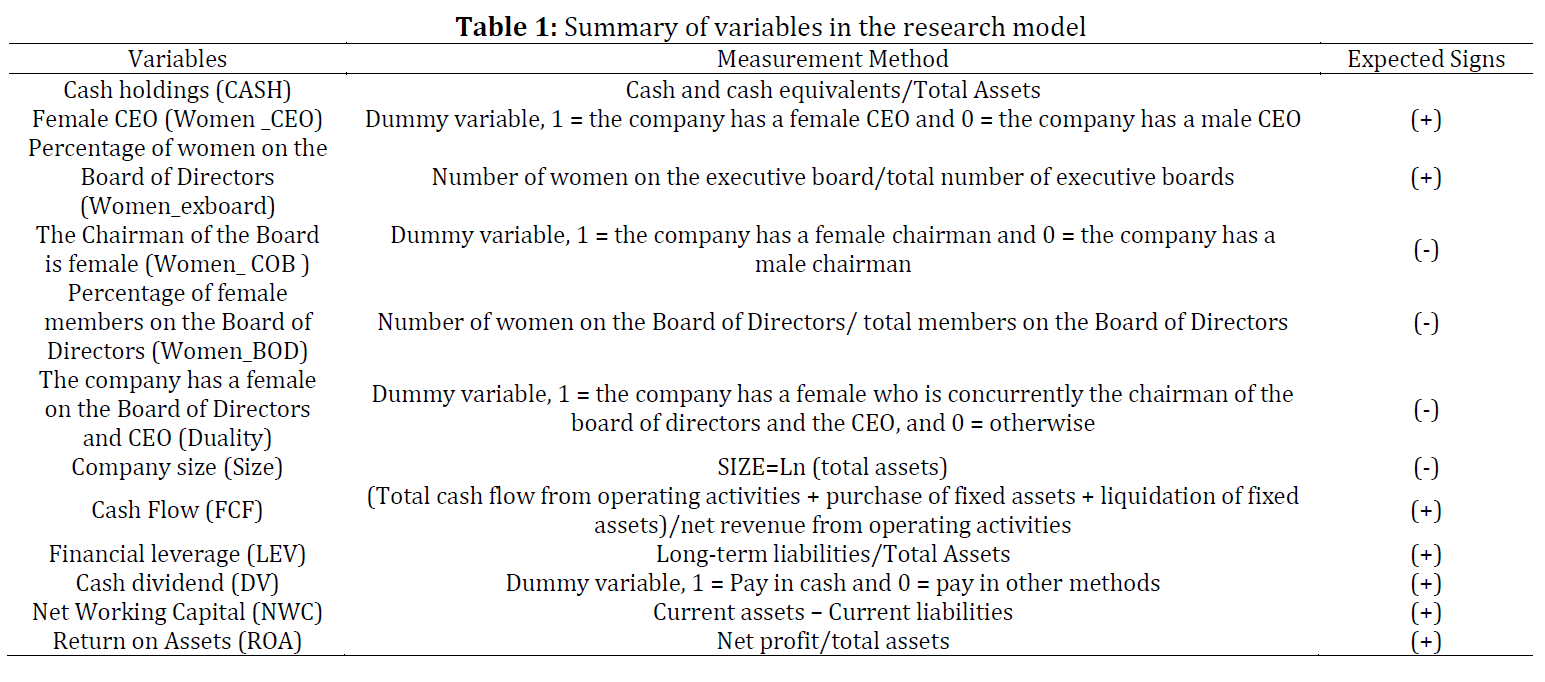

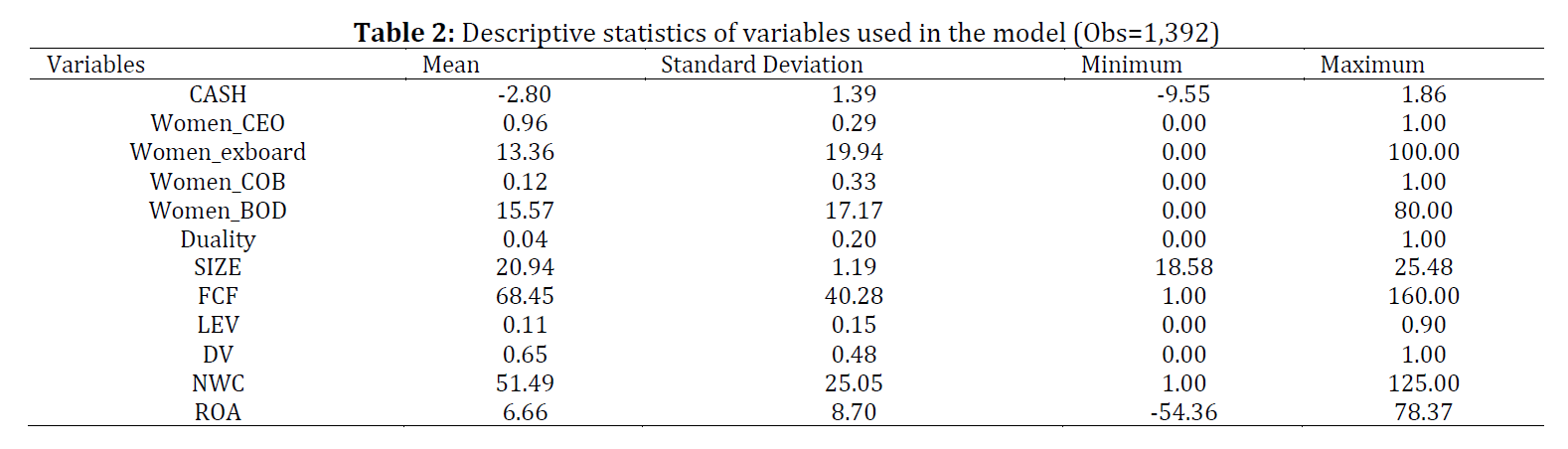

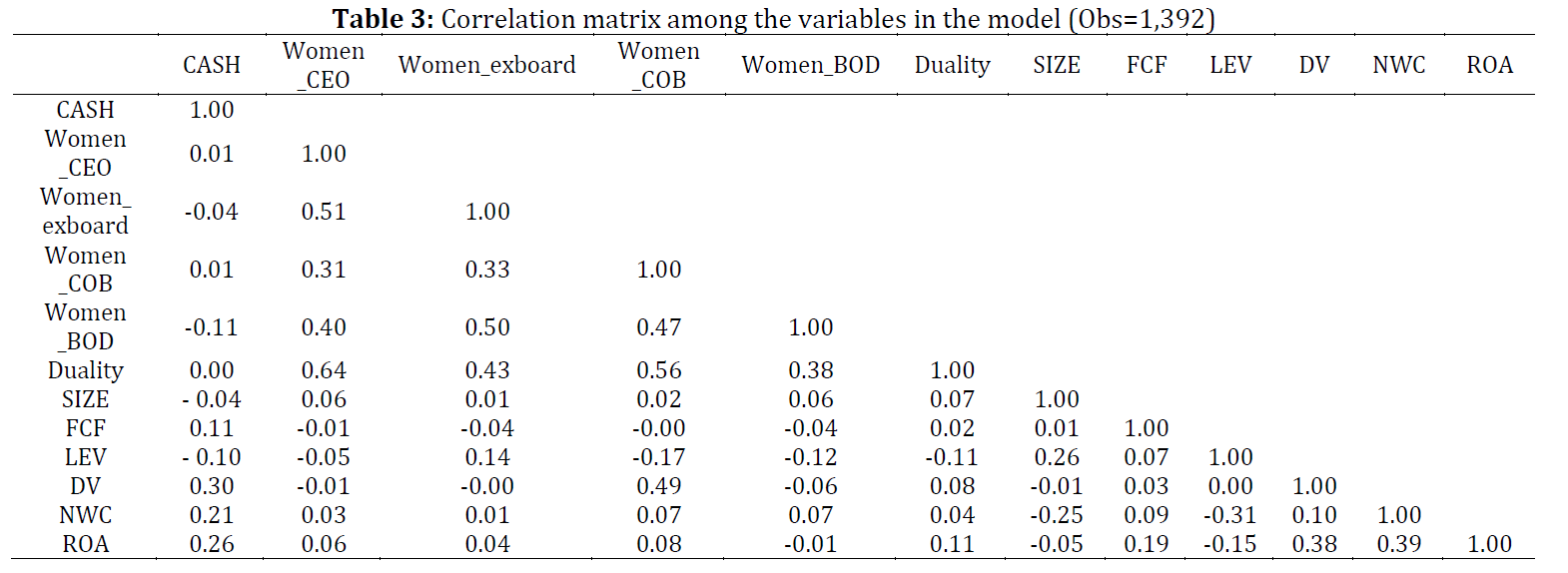

This study examines the relationship between female leadership factors and the cash holdings of Vietnamese companies. The random effects regression model (REM) is used with panel data from the financial statements of 174 companies listed on the Ho Chi Minh Stock Exchange in the period 2013-2020. Besides control variables, factors related to female leadership including the female CEO, the percentage of women on the board of executives, the female chairman, the percentage of women on the board of directors, and duality are included in the research model with the expectation of having a positive effect on cash holdings. The estimation results show that companies with female executives hold more cash and maintain lower levels of financial leverage than companies with male executives. Female executives will increase profitability and reduce the risk to the company. The influence level of the female on the Board of Directors on the company's cash holdings depends on the characteristics of each company. Besides, the results also show that net working capital, cash flow, ROA, and dividend payment have a positive correlation with the cash holdings of the company. Listed companies should pay attention to two factors: the proportion of women on the Board of Directors and female executives in order to diversify gender in the leadership and improve the ability to decide on financial strategies.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Gender diversity, Board of directors, Female executives, Cash holdings, Listed companies

Article History: Received 22 February 2022, Received in revised form 14 May 2022, Accepted 18 May 2022

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Le TN, Le LH, and Duong BT et al. (2022). The influence of female leadership on the cash holdings of listed companies in Vietnam. International Journal of Advanced and Applied Sciences, 9(8): 55-64

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (42)

- Adhikari B (2012). Gender differences in corporate financial decisions and performance. https://doi.org/10.2139/ssrn.2011088 [Google Scholar]

- Adhikari BK (2018). Female executives and corporate cash holdings. Applied Economics Letters, 25(13): 958-963. https://doi.org/10.1080/13504851.2017.1388904 [Google Scholar]

- Afrifa GA and Padachi K (2016). Working capital level influence on SME profitability. Journal of Small Business and Enterprise Development, 23(1): 44-63. https://doi.org/10.1108/JSBED-01-2014-0014 [Google Scholar]

- Almeida H, Campello M, and Weisbach MS (2004). The cash flow sensitivity of cash. The Journal of Finance, 59(4): 1777-1804. https://doi.org/10.1111/j.1540-6261.2004.00679.x [Google Scholar]

- Atif M, Liu B, and Huang A (2019). Does board gender diversity affect corporate cash holdings? Journal of Business Finance and Accounting, 46(7-8): 1003-1029. https://doi.org/10.1111/jbfa.12397 [Google Scholar]

- Bao D, Chan KC, and Zhang W (2012). Asymmetric cash flow sensitivity of cash holdings. Journal of Corporate Finance, 18(4): 690-700. https://doi.org/10.1016/j.jcorpfin.2012.05.003 [Google Scholar]

- Bates TW, Kahle KM, and Stulz RM (2009). Why do US firms hold so much more cash than they used to? The Journal of Finance, 64(5): 1985-2021. https://doi.org/10.1111/j.1540-6261.2009.01492.x [Google Scholar]

- Chang Y, Benson K, and Faff R (2017). Are excess cash holdings more valuable to firms in times of crisis? Financial constraints and governance matters. Pacific-Basin Finance Journal, 45: 157-173. https://doi.org/10.1016/j.pacfin.2016.05.007 [Google Scholar]

- Denis DJ and Sibilkov V (2010). Financial constraints, investment, and the value of cash holdings. The Review of Financial Studies, 23(1): 247-269. https://doi.org/10.1093/rfs/hhp031 [Google Scholar]

- Dittmar A and Mahrt-Smith J (2007). Corporate governance and the value of cash holdings. Journal of Financial Economics, 83(3): 599-634. https://doi.org/10.1016/j.jfineco.2005.12.006 [Google Scholar]

- Drobetz W and Grüninger MC (2007). Corporate cash holdings: Evidence from Switzerland. Financial Markets and Portfolio Management, 21(3): 293-324. https://doi.org/10.1007/s11408-007-0052-8 [Google Scholar]

- Faccio M, Marchica MT, and Mura R (2016). CEO gender, corporate risk-taking, and the efficiency of capital allocation. Journal of Corporate Finance, 39: 193-209. https://doi.org/10.1016/j.jcorpfin.2016.02.008 [Google Scholar]

- Fairlie RW and Robb AM (2009). Gender differences in business performance: Evidence from the characteristics of business owners survey. Small Business Economics, 33(4): 375-395. https://doi.org/10.1007/s11187-009-9207-5 [Google Scholar]

- Farrar DE and Glauber RR (1967). Multicollinearity in regression analysis: The problem revisited. The Review of Economic and Statistics, 49(1): 92-107. https://doi.org/10.2307/1937887 [Google Scholar]

- Faulkender M and Wang R (2006). Corporate financial policy and the value of cash. The Journal of Finance, 61(4): 1957-1990. https://doi.org/10.1111/j.1540-6261.2006.00894.x [Google Scholar]

- Frésard L and Salva C (2010). The value of excess cash and corporate governance: Evidence from US cross-listings. Journal of Financial Economics, 98(2): 359-384. https://doi.org/10.1016/j.jfineco.2010.04.004 [Google Scholar]

- Gill A and Shah C (2012). Determinants of corporate cash holdings: Evidence from Canada. International Journal of Economics and Finance, 4(1): 70-79. https://doi.org/10.5539/ijef.v4n1p70 [Google Scholar]

- Gill AS and Biger N (2013). The impact of corporate governance on working capital management efficiency of American manufacturing firms. Managerial Finance, 39(2): 116-132. https://doi.org/10.1108/03074351311293981 [Google Scholar]

- Gul FA, Srinidhi B, and Tsui JS (2008). Board diversity and the demand for higher audit effort. https://doi.org/10.2139/ssrn.1359450 [Google Scholar]

- Hampel R (1998). Committee on corporate governance: Final report. Gee Publishing, London, UK. [Google Scholar]

- Haushalter D, Klasa S, and Maxwell WF (2007). The influence of product market dynamics on a firm's cash holdings and hedging behavior. Journal of Financial Economics, 84(3): 797-825. https://doi.org/10.1016/j.jfineco.2006.05.007 [Google Scholar]

- Hsu CS, Kuo L, and Chang BG (2013). Gender difference in profit performance-evidence from the owners of small public accounting practices in Taiwan. Asian Journal of Finance and Accounting, 5(1): 140-159. https://doi.org/10.5296/ajfa.v5i1.3174 [Google Scholar]

- Inmyxai S and Takahashi Y (2010). Performance contrast and its determinants between male and female headed firms in Lao MSMEs. International Journal of Business and Management, 5(4), 37-52. https://doi.org/10.5539/ijbm.v5n4p37 [Google Scholar]

- Isshaq Z and Bokpin GA (2009). Corporate liquidity management of listed firms in Ghana. Asia-Pacific Journal of Business Administration, 1(2): 189-198. https://doi.org/10.1108/17574320910989122 [Google Scholar]

- Jensen MC and Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [Google Scholar]

- Kaplan SN and Zingales L (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics, 112(1): 169-215. https://doi.org/10.1162/003355397555163 [Google Scholar]

- Kusnadi Y (2011). Do corporate governance mechanisms matter for cash holdings and firm value? Pacific-Basin Finance Journal, 19(5): 554-570. https://doi.org/10.1016/j.pacfin.2011.04.002 [Google Scholar]

- Lee E and Powell R (2011). Excess cash holdings and shareholder value. Accounting and Finance, 51(2): 549-574. https://doi.org/10.1111/j.1467-629X.2010.00359.x [Google Scholar]

- Mansour W, Ben Jedidia K, and Majdoub J (2015). How ethical is Islamic banking in the light of the objectives of Islamic law? Journal of Religious Ethics, 43(1): 51-77. https://doi.org/10.1111/jore.12086 [Google Scholar]

- Mishra RK and Jhunjhunwala S (2013). Diversity and the effective corporate board. Academic Press, Cambridge, USA. [Google Scholar]

- Opler T, Pinkowitz L, Stulz R, and Williamson R (1999). The determinants and implications of corporate cash holdings. Journal of Financial Economics, 52(1): 3-46. https://doi.org/10.1016/S0304-405X(99)00003-3 [Google Scholar]

- Ozkan A and Ozkan N (2004). Corporate cash holdings: An empirical investigation of UK companies. Journal of Banking and Finance, 28(9): 2103-2134. https://doi.org/10.1016/j.jbankfin.2003.08.003 [Google Scholar]

- Pinkowitz L, Stulz R, and Williamson R (2006). Does the contribution of corporate cash holdings and dividends to firm value depend on governance? A cross‐country analysis. The Journal of Finance, 61(6): 2725-2751. https://doi.org/10.1111/j.1540-6261.2006.01003.x [Google Scholar]

- Rozeff MS (1982). Growth, beta and agency costs as determinants of dividend payout ratios. Journal of Financial Research, 5(3): 249-259. https://doi.org/10.1111/j.1475-6803.1982.tb00299.x [Google Scholar]

- Sah NB (2021). Cash is queen: Female CEOs’ propensity to hoard cash. Journal of Behavioral and Experimental Finance, 29: 100412. https://doi.org/10.1016/j.jbef.2020.100412 [Google Scholar]

- Singh V and Vinnicombe S (2004). Why so few women directors in top UK boardrooms? Evidence and theoretical explanations. Corporate Governance: An International Review, 12(4): 479-488. https://doi.org/10.1111/j.1467-8683.2004.00388.x [Google Scholar]

- Smith N, Smith V, and Verner M (2006). Do women in top management affect firm performance? A panel study of 2,500 Danish firms. International Journal of Productivity and Performance Management, 55(7): 569-593. https://doi.org/10.1108/17410400610702160 [Google Scholar]

- Van Horne JC and Wachowicz JM (2001). Fundamentals of financial management. Pearson Educación, London, UK. [Google Scholar]

- Viechtbauer W (2010). Conducting meta-analyses in R with the metafor package. Journal of Statistical Software, 36(3): 1-48. https://doi.org/10.18637/jss.v036.i03 [Google Scholar]

- White H (1980). Using least squares to approximate unknown regression functions. International Economic Review, 21(1): 149-170. https://doi.org/10.2307/2526245 [Google Scholar]

- Whited TM and Riddick LA (2009). The corporate property to save. The Journal of Finance, 64(4): 1729–1766. https://doi.org/10.1111/j.1540-6261.2009.01478.x [Google Scholar]

- Zeng S and Wang L (2015). CEO gender and corporate cash holdings. Are female CEOs more conservative? Asia-Pacific Journal of Accounting and Economics, 22(4): 449-474. https://doi.org/10.1080/16081625.2014.1003568 [Google Scholar]