International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 6 (June 2022), Pages: 145-153

----------------------------------------------

Original Research Paper

Factors affecting the social insurance compliance of enterprises in Vietnam

Author(s): Tan Nghiem Le 1, *, Long Hau Le 2, Bich Tuyen Duong 3, Tran Huynh Nguyen 4, Viet Thanh Truc Tran 2, Thi Thanh Tam Nguyen 5

Affiliation(s):

1Department of Business Administration, School of Economics, Can Tho University, Can Tho, Vietnam

2Department of Finance and Banking, School of Economics, Can Tho University, Can Tho, Vietnam

3School of Economics, Nam Can Tho University, Can Tho, Vietnam

4Vietnam Social Security, An Giang Branch, An Giang, Vietnam

5School of Economics, Can Tho University, Can Tho, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-8332-6388

Corresponding author's ORCID profile: https://orcid.org/0000-0001-8332-6388

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.06.019

Abstract:

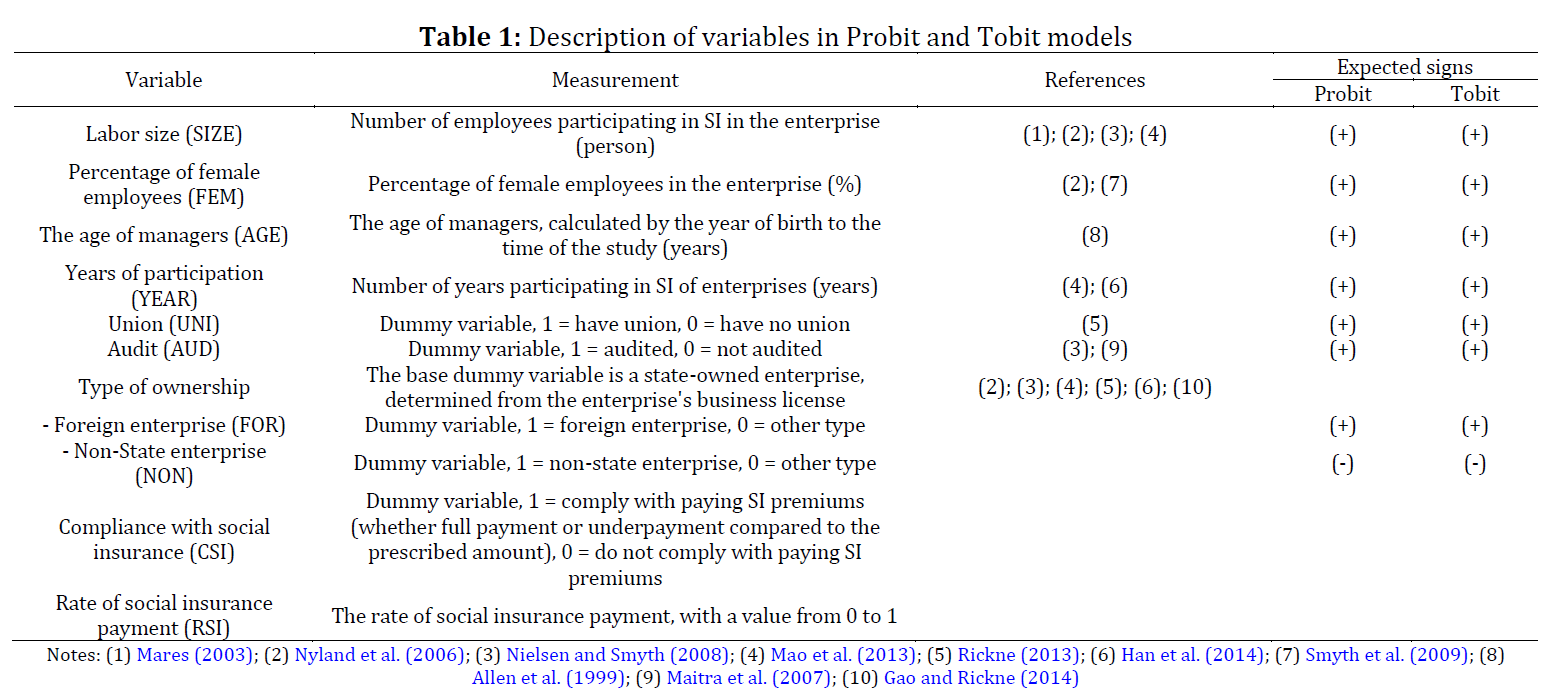

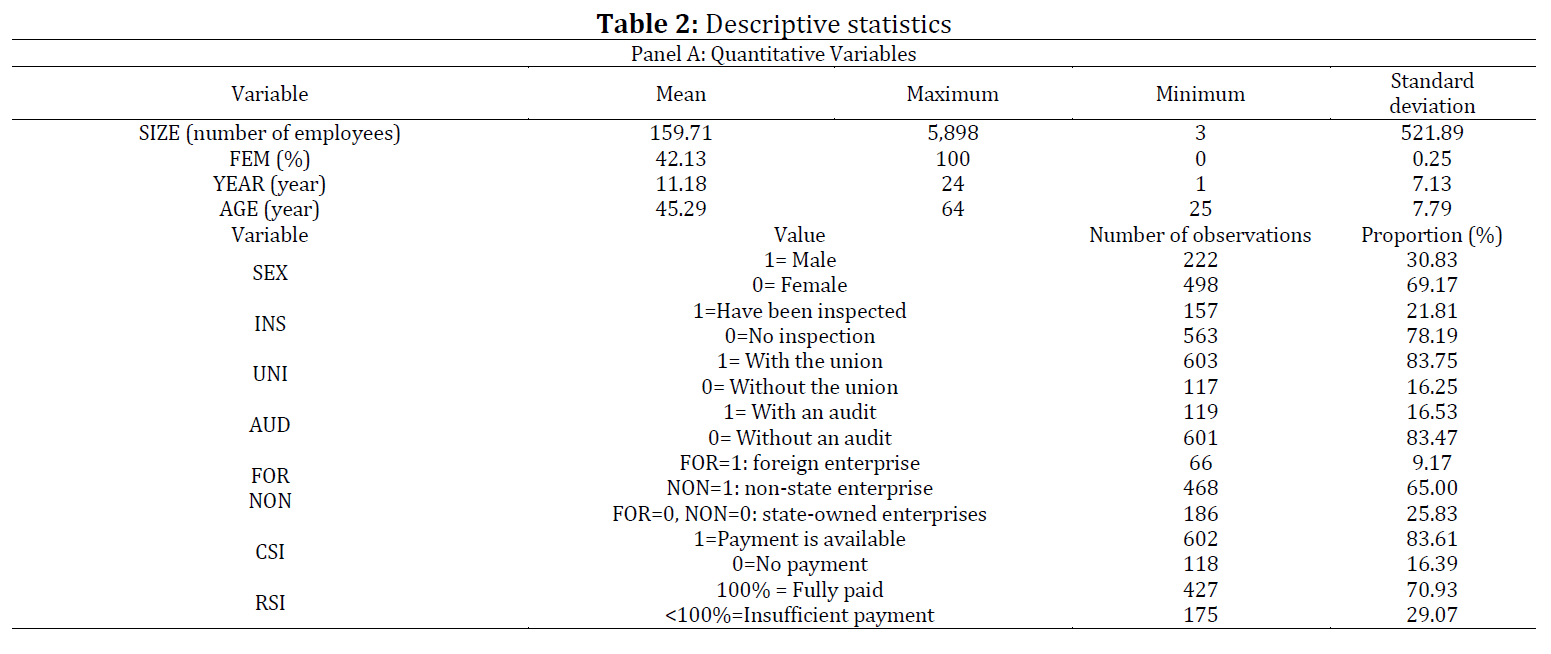

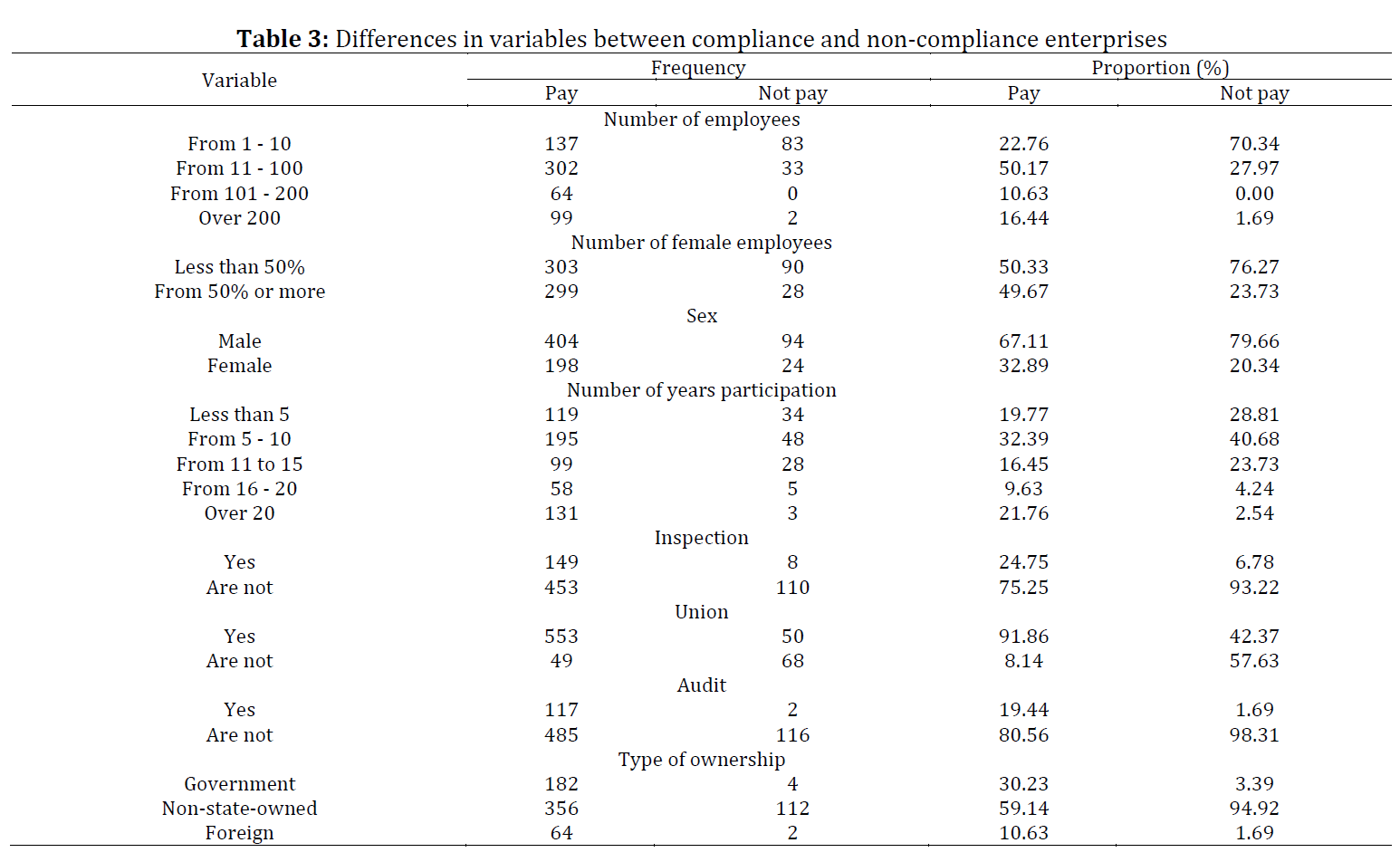

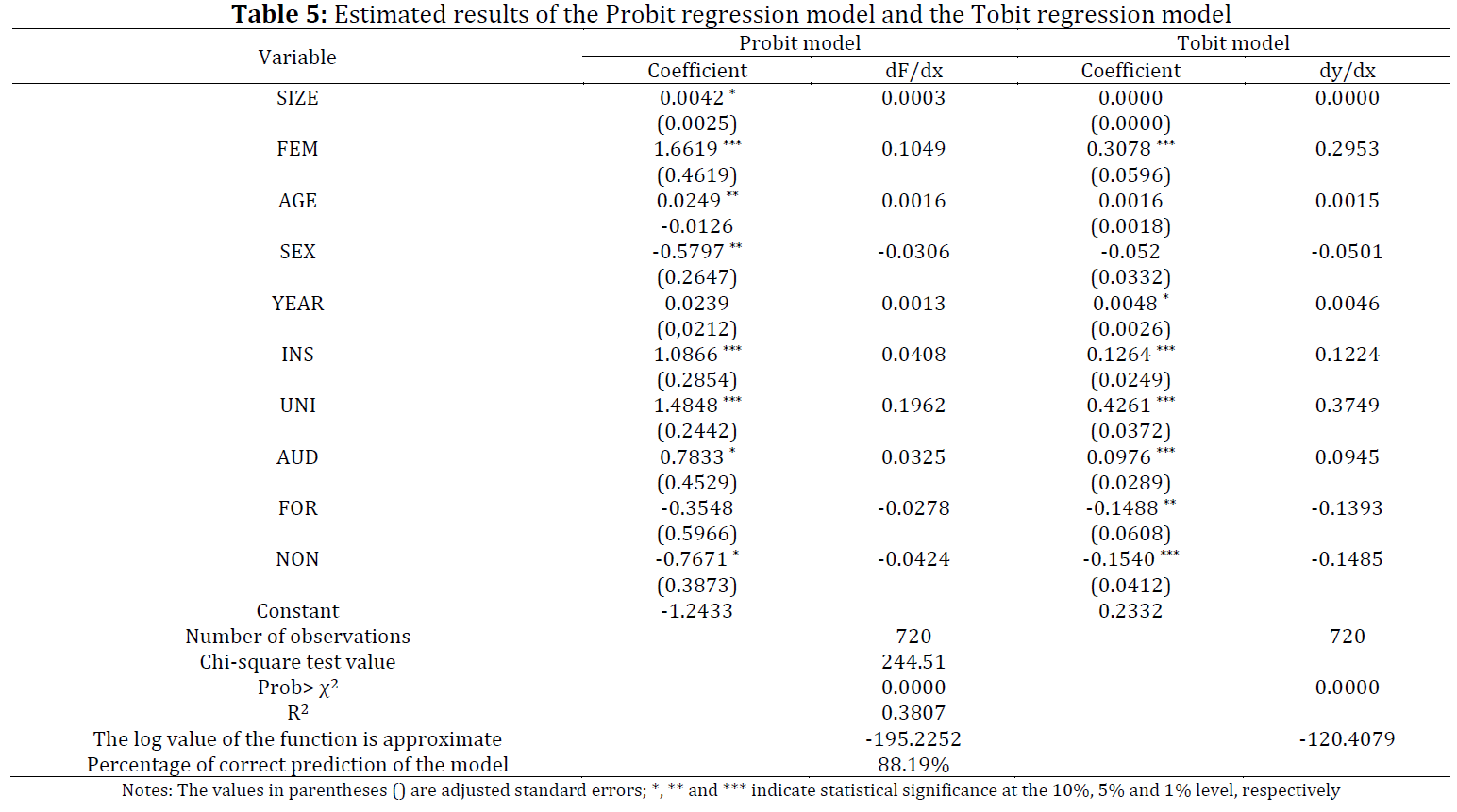

This article aims to determine the factors affecting the social insurance compliance of enterprises in Vietnam. Based on the economic and behavioral approach, hypotheses on the determinants of insurance compliance are proposed. A sample of 240 enterprises with data on paying insurance premiums for employees in Vietnam from 2016 to 2018 is collected to carry out this research. According to the Probit regression model results, the enterprises' decision to comply with social insurance is significantly positively impacted by the number of employees, the proportion of female employees, the age of the managers, inspectors, and unions. On the contrary, the gender of managers, and non-state enterprises have a negative and statistically significant influence on compliance with social insurance regulations. Besides, the results in Tobit regression models reveal the proportion of female employees, seniority of participation, inspections, unions, and auditors have a positive impact on the level of social insurance compliance of Vietnamese enterprises, while foreign and non-state enterprises have a negative effect on the contribution rate of these enterprises. Most of the previous studies focused on the decision to participate in social insurance without considering the actual payment ratio compared to the regulations, and empirical studies on this topic are still limited in Vietnam. This study can be an empirical basis for managers to minimize the debt of social insurance of enterprises, and increase the responsibility of employers for government regulations related to the protection of workers' rights.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Social insurance, Compliance, Social policies, Enterprises, Logistic regression

Article History: Received 12 January 2022, Received in revised form ,7 April 2022, Accepted 11 April 2022

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Le TN, Le LH, and Duong BT et al. (2022). Factors affecting the social insurance compliance of enterprises in Vietnam. International Journal of Advanced and Applied Sciences, 9(6): 145-153

Figures

No Figure

Tables

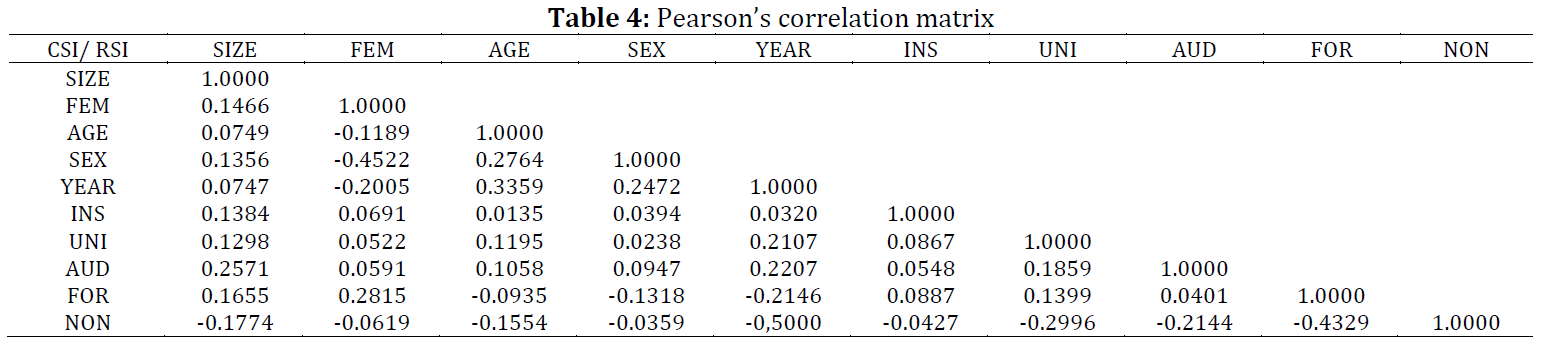

Table 1 Table 2 Table 3 Table 4 Table 5

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (21)

- Allen SB, Goodwin DW, and Herrod JW (1999). Life and health insurance marketing. 2nd Edition. Life Office Management Association, Atlanta, USA. [Google Scholar]

- Allingham MG and Sandmo A (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1: 323-338. https://doi.org/10.1016/0047-2727(72)90010-2 [Google Scholar]

- Castel P and To TT (2012). Informal employment in the formal sector: Wages and social security tax evasion in Vietnam. Journal of the Asia Pacific Economy, 17(4): 616-631. https://doi.org/10.1080/13547860.2012.724551 [Google Scholar]

- Elffers H, Robben HS, and Hessing DJ (1992). On measuring tax evasion. Journal of Economic Psychology, 13(4): 545-567. https://doi.org/10.1016/0167-4870(92)90011-U [Google Scholar]

- Farrar DE and Glauber RR (1967). Multicollinearity in regression analysis: The problem revisited. The Review of Economics and Statistics, 49: 92-107. https://doi.org/10.2307/1937887 [Google Scholar]

- Gao Q and Rickne J (2014). Firm ownership and social insurance inequality in transitional China: Evidence from a large panel of firm-level data. European Journal of Social Security, 16(1): 2-25. https://doi.org/10.1177/138826271401600101 [Google Scholar]

- Han Y, Zheng E, and Xu M (2014). The influence from the past: Organizational imprinting and firms’ compliance with social insurance policies in China. Journal of Business Ethics, 122(1): 65-77. https://doi.org/10.1007/s10551-013-1758-3 [Google Scholar]

- Huynh TN (2021). Impacts of social insurance on firm performance: Evidence from Vietnamese small-and medium-sized enterprises. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-08-2020-0869 [Google Scholar]

- Kirchler E and Maciejovsky B (2001). Tax compliance within the context of gain and loss situations, expected and current asset position, and profession. Journal of Economic Psychology, 22(2): 173-194. https://doi.org/10.1016/S0167-4870(01)00028-9 [Google Scholar]

- Maitra P, Smyth R, Nielsen I, Nyland C, and Zhu C (2007). Firm compliance with social insurance obligations where there is a weak surveillance and enforcement mechanism: Empirical evidence from Shanghai. Pacific Economic Review, 12(5): 577-596. https://doi.org/10.1111/j.1468-0106.2007.00373.x [Google Scholar]

- Mandigma MBS (2016). Determinants of social insurance coverage in the Philippines. International Journal of Social Science and Humanity, 6: 660-666. https://doi.org/10.7763/IJSSH.2016.V6.728 [Google Scholar]

- Mao J, Zhang L, and Zhao J (2013). Social security taxation and compliance: The Chinese evidence. https://doi.org/10.2139/ssrn.2151695 [Google Scholar]

- Mares I (2003). The sources of business interest in social insurance: Sectoral versus national differences. World Politics, 55(2): 229-258. https://doi.org/10.1353/wp.2003.0012 [Google Scholar]

- Nguyen KD, Tran VA, and Nguyen DT (2021). Social insurance reform and absenteeism in Vietnam. International Journal of Social Welfare, 30(2): 193-207. https://doi.org/10.1111/ijsw.12449 [Google Scholar]

- Nielsen I and Smyth R (2008). Who bears the burden of employer compliance with social security contributions? Evidence from Chinese firm level data. China Economic Review, 19(2): 230-244. https://doi.org/10.1016/j.chieco.2007.06.002 [Google Scholar]

- Nyland C, Smyth R, and Zhu CJ (2006). What determines the extent to which employers will comply with their social security obligations? Evidence from Chinese firm‐level data. Social Policy and Administration, 40(2): 196-214. https://doi.org/10.1111/j.1467-9515.2006.00484.x [Google Scholar]

- Nyland C, Thomson SB, and Zhu CJ (2011). Employer attitudes towards social insurance compliance in Shanghai, China. International Social Security Review, 64(4): 73-98. https://doi.org/10.1111/j.1468-246X.2011.01412.x [Google Scholar]

- Pate AM and Hamilton EE (1992). Formal and informal deterrents to domestic violence: The Dade County spouse assault experiment. American Sociological Review, 57: 691-697. https://doi.org/10.2307/2095922 [Google Scholar]

- Rickne J (2013). Labor market conditions and social insurance in China. China Economic Review, 27: 52-68. https://doi.org/10.1016/j.chieco.2013.07.003 [Google Scholar]

- Smyth R, Nielsen I, and Qian X (2009). What determines employer willingness to “top up” social insurance? Evidence from Shanghai's 25 plus X scheme. International Journal of Manpower, 30(6): 512-528. https://doi.org/10.1108/01437720910988957 [Google Scholar]

- Tachibanaki T and Yokoyama Y (2008). The estimation of the incidence of employer contributions to social security in Japan. The Japanese Economic Review, 59(1): 75-83. https://doi.org/10.1111/j.1468-5876.2007.00380.x [Google Scholar]