International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 5 (May 2022), Pages: 90-95

----------------------------------------------

Original Research Paper

Title: A study on prediction model estimation of financial assets (exchange rate, KOSPI index, interest rate)

Author(s): Chang-Ho An *

Affiliation(s):

Department of Financial Information Engineering, Seokyeong University, Seoul, South Korea

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-6415-2757

Corresponding author's ORCID profile: https://orcid.org/0000-0001-6415-2757

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.05.012

Abstract:

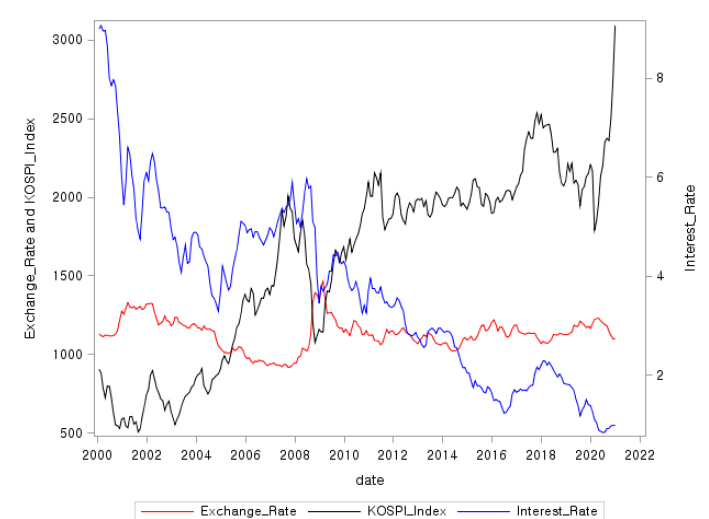

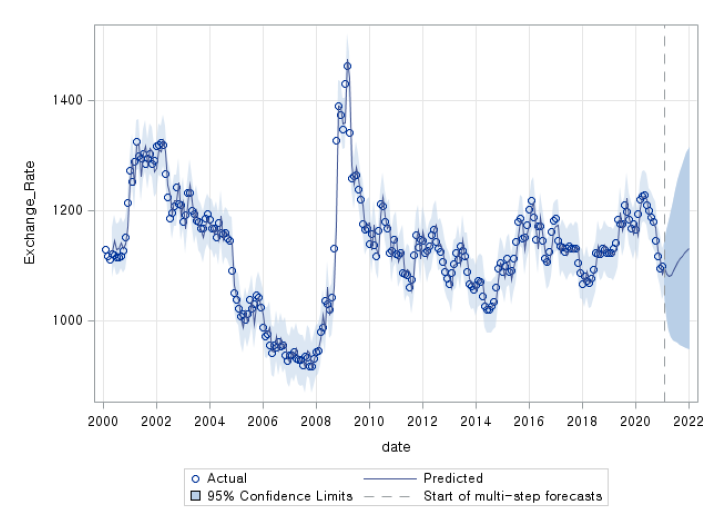

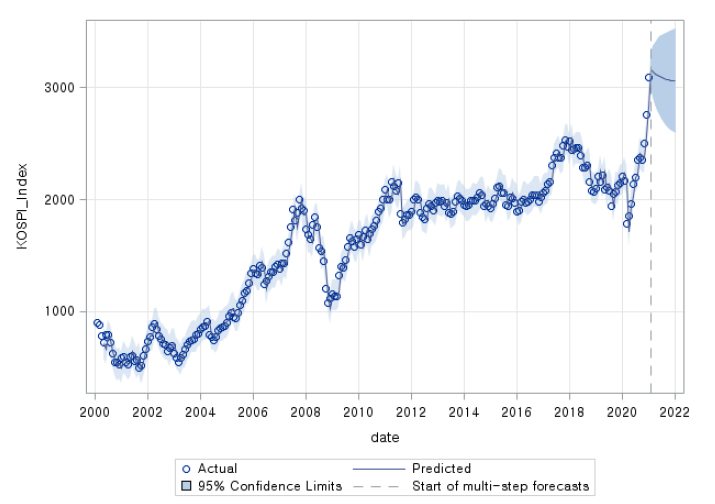

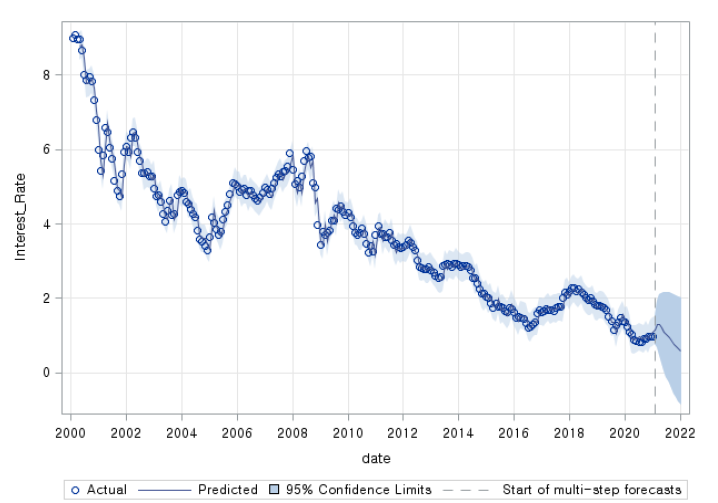

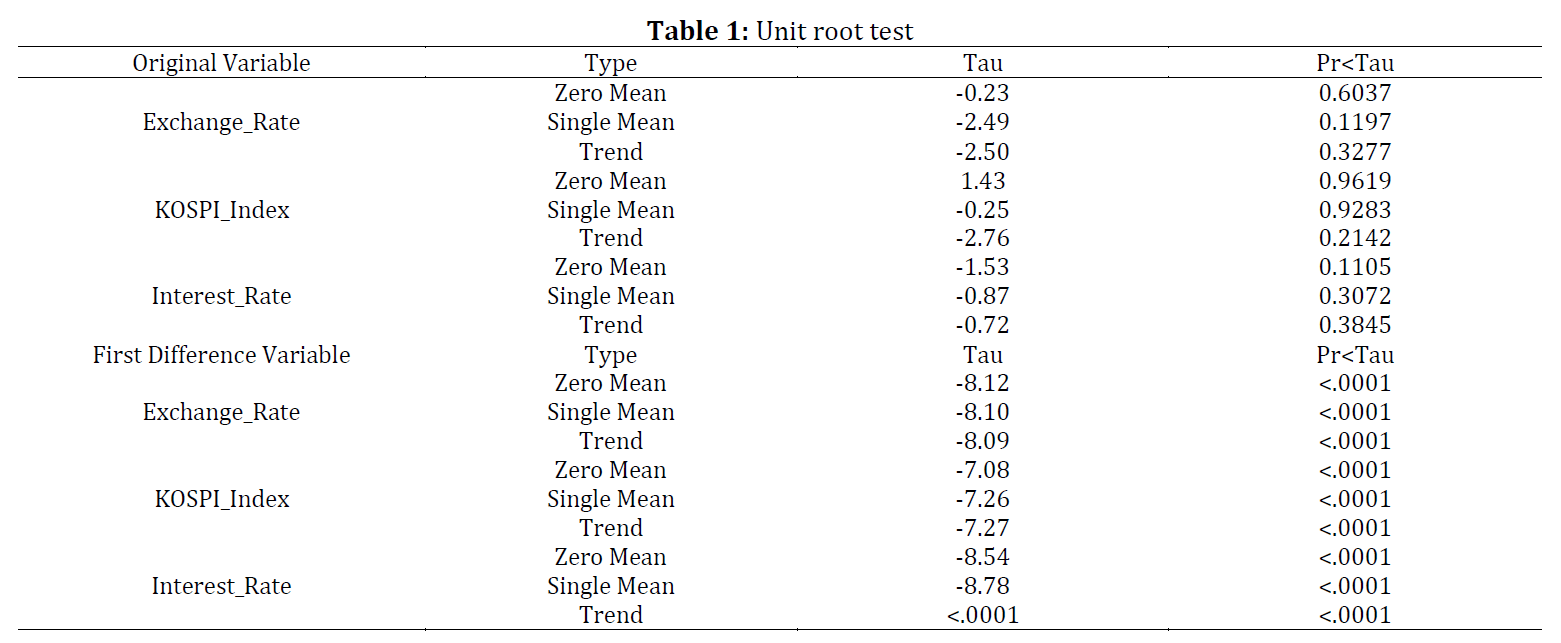

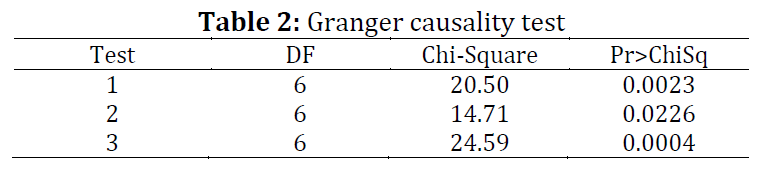

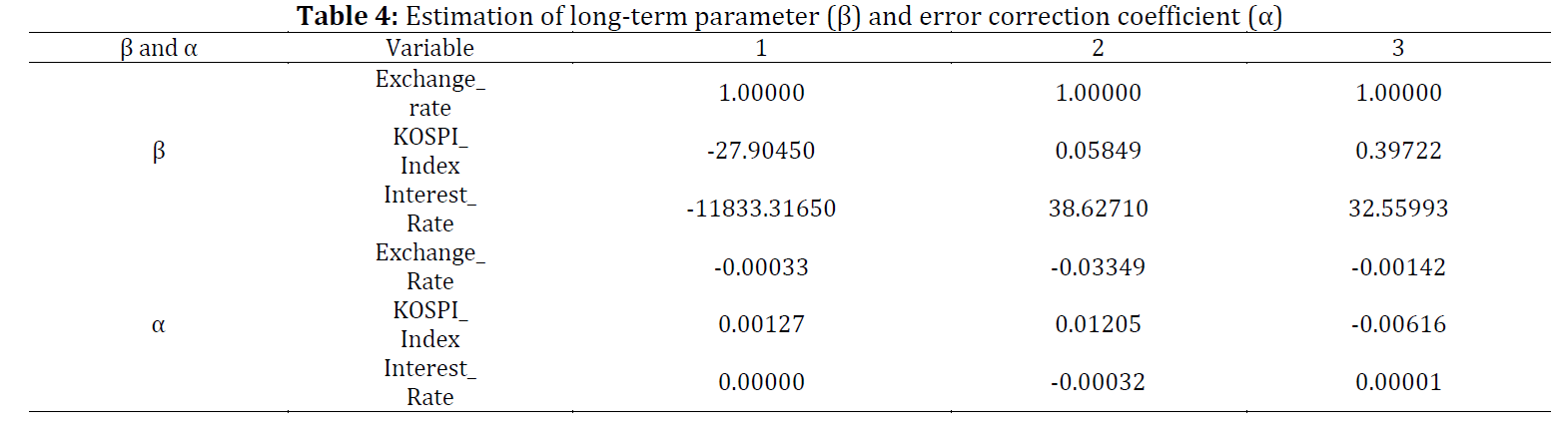

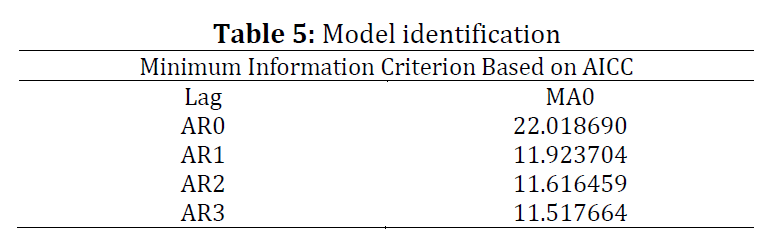

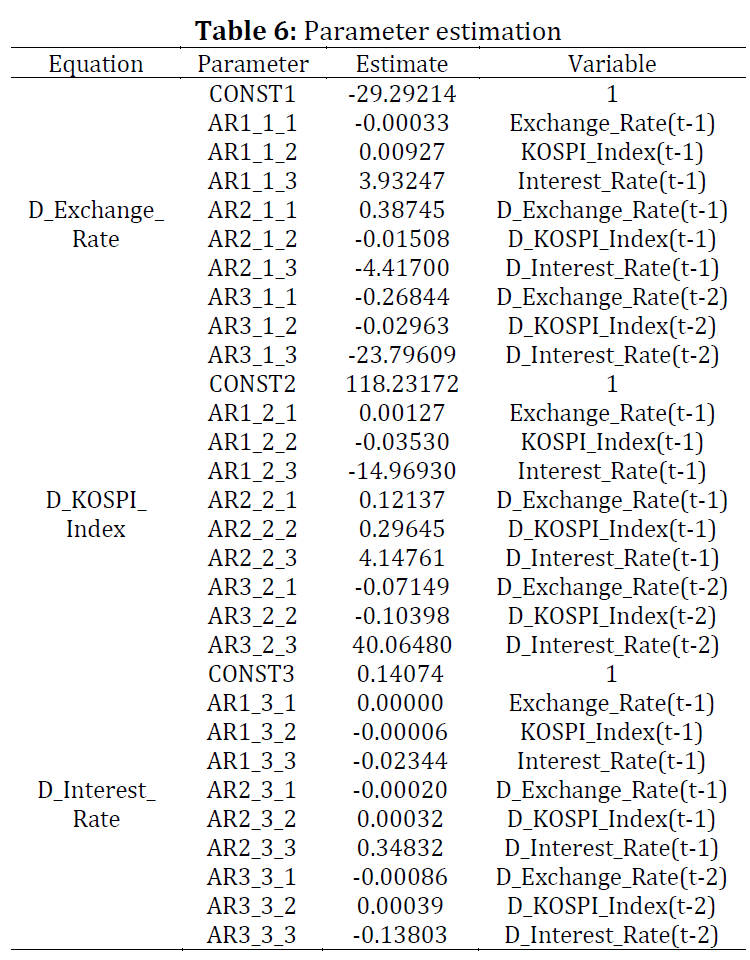

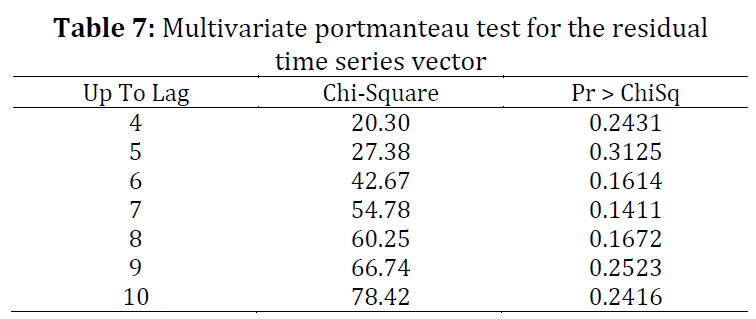

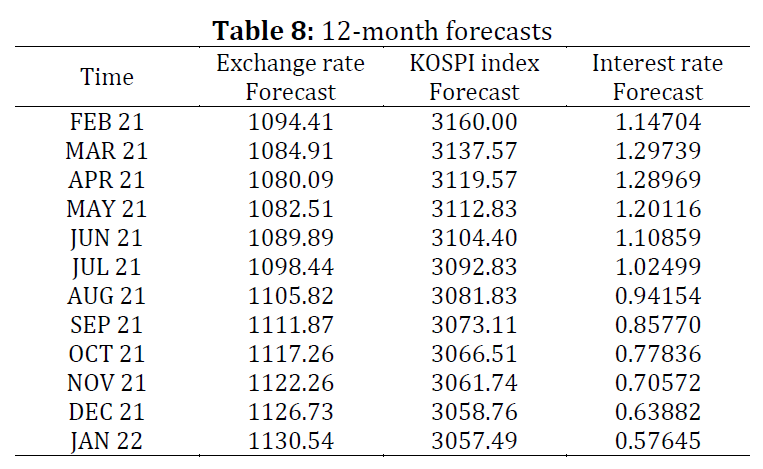

In this study, financial assets such as exchange rate, KOSPI index, and interest rate (3-year government bond) were predicted using the vector error correction model used in various financial markets. For this purpose, time series data from February 2000 to January 2021 provided by the Bank of Korea were used. To estimate the prediction model, the stability of the time series variables was confirmed by the ADF test, the causal relationship between the time series variables by the Granger causality test, and the cointegration relationship between the time series variables by the cointegration test. In addition, the prediction model was estimated by identifying the model based on the minimum information criterion based on AICC statistics, and the validity of the model was confirmed by the significance test of the cross-correlation matrix and the multivariate Portmanteau test. As the result of forecasting with the estimated prediction model, the exchange rate was predicted to rise steadily, the KOSPI index was predicted to fall, but remain in the mid-3,000 range, and the interest rate (3-year government bond) was predicted to decline.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Vector error correction model, Granger causality test, Cointegration test, AICC statistics, Multivariate portmanteau test

Article History: Received 10 December 2021, Received in revised form 25 February 2022, Accepted 5 March 2022

Acknowledgment

This research was supported by Seokyeong University in 2021.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

An CH (2022). A study on prediction model estimation of financial assets (exchange rate, KOSPI index, interest rate). International Journal of Advanced and Applied Sciences, 9(5): 90-95

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (12)

- Baig MT and Goldfajn MI (1998). Monetary policy in the aftermath of currency crises: The case of Asia. International Monetary Fund, Washington, USA. https://doi.org/10.2139/ssrn.883294 [Google Scholar]

- Darbar MSM and Deb P (1999). Linkages among asset markets in the United States: Tests in a bivariate GARCH framework. International Monetary Fund, Washington, USA. https://doi.org/10.2139/ssrn.880685 [Google Scholar]

- Engle RF and Granger CW (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica: Journal of the Econometric Society, 55: 251-276. https://doi.org/10.2307/1913236 [Google Scholar]

- Fleming J, Kirby C, and Ostdiek B (1998). Information and volatility linkages in the stock, bond, and money markets. Journal of Financial Economics, 49(1): 111-137. https://doi.org/10.1016/S0304-405X(98)00019-1 [Google Scholar]

- Granger CW (1980). Testing for causality: A personal viewpoint. Journal of Economic Dynamics and Control, 2: 329-352. https://doi.org/10.1016/0165-1889(80)90069-X [Google Scholar]

- Harbo I, Johansen S, Nielsen B, and Rahbek A (1998). Asymptotic inference on cointegrating rank in partial systems. Journal of Business and Economic Statistics, 16(4): 388-399. https://doi.org/10.1080/07350015.1998.10524779 [Google Scholar]

- Hosking JR (1980). The multivariate portmanteau statistic. Journal of the American Statistical Association, 75(371): 602-608. https://doi.org/10.1080/01621459.1980.10477520 [Google Scholar]

- Johansen S (1995). A statistical analysis of cointegration for I (2) variables. Econometric Theory, 11(1): 25-59. https://doi.org/10.1017/S0266466600009026 [Google Scholar]

- Kim IS and Park DC (2012). A study on relationship between housing finance and macroeconomic variables using the VAR model. Journal of the Korean Regional Economics, 22: 3-18. [Google Scholar]

- Lee W and Chun H (2016). A deep learning analysis of the Chinese Yuan's volatility in the onshore and offshore markets. Journal of the Korean Data and Information Science Society, 27(2): 327-335. https://doi.org/10.7465/jkdi.2016.27.2.327 [Google Scholar]

- Li Q, Wang T, Li P, Liu L, Gong Q, and Chen Y (2014). The effect of news and public mood on stock movements. Information Sciences, 278: 826-840. https://doi.org/10.1016/j.ins.2014.03.096 [Google Scholar]

- Park HS and An JA (2009). The sources of regional real estate price fluctuations. Korea Real Estate Review, 19: 27-49. [Google Scholar]