International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 2 (February 2022), Pages: 72-80

----------------------------------------------

Original Research Paper

Title: Systematic illiquidity, characteristic illiquidity, and stock returns: Timeseries analysis

Author(s): Hela Ben Soltane 1, 2, *, Kamel Naoui 2, Abdulhamid Alshammari 1

Affiliation(s):

1College of Business Administration, University of Ha’il, Ha’il, Saudi Arabia

2Higher School of Business of Tunis, University of Manouba, Tunisia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-0615-4807

Corresponding author's ORCID profile: https://orcid.org/0000-0002-0615-4807

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.02.008

Abstract:

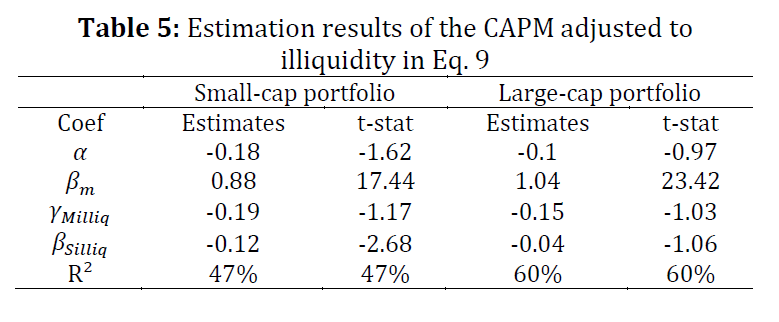

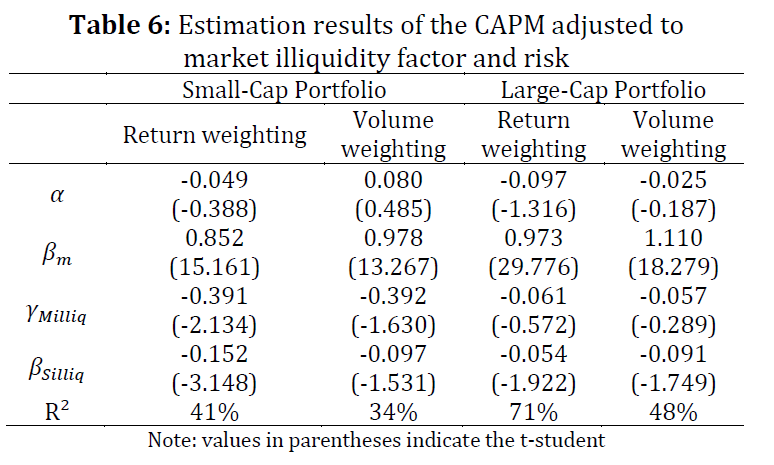

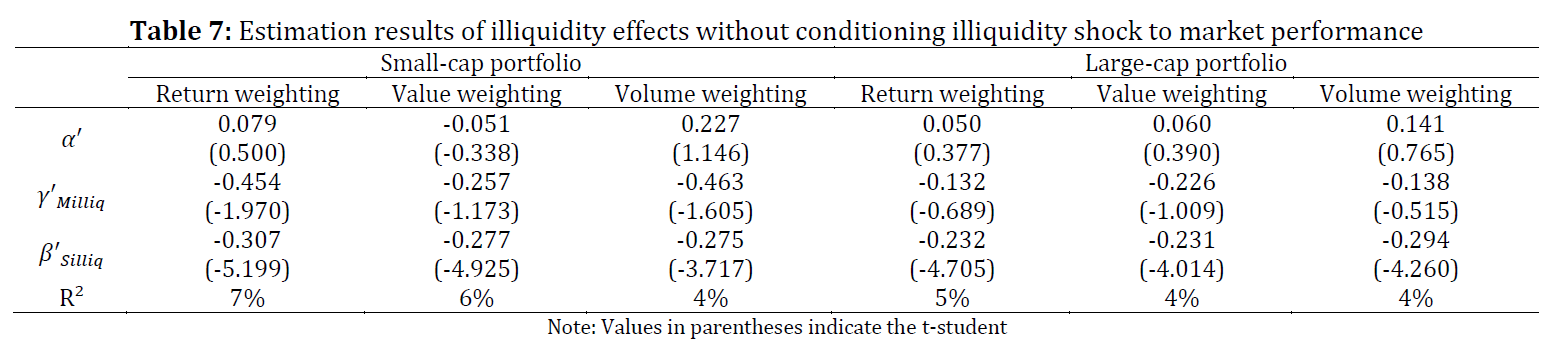

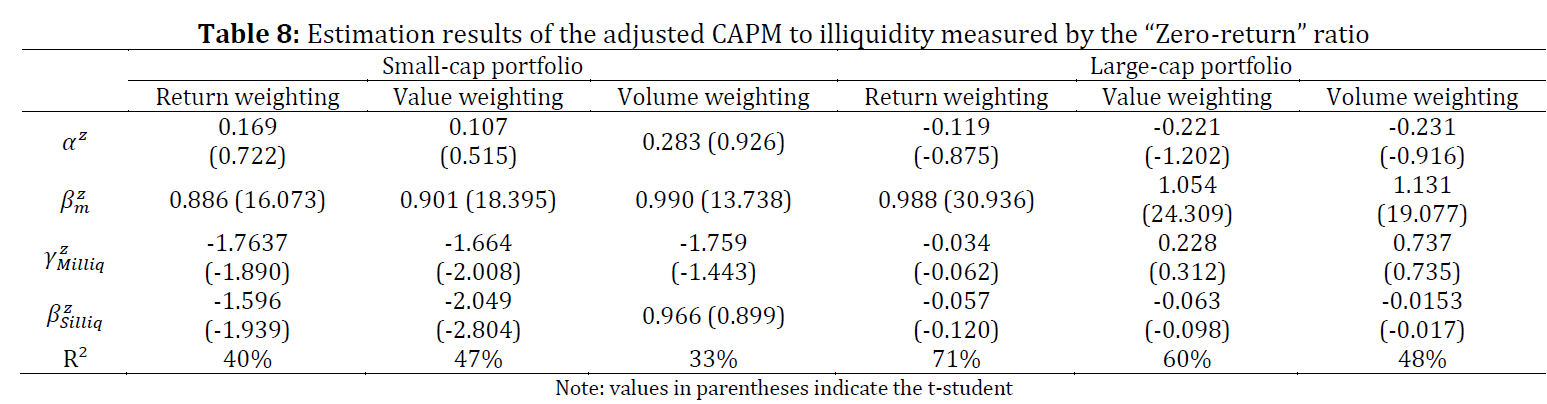

The objective of this research is to investigate the relationship between illiquidity and stock prices on the Tunisian stock exchange. While previous researches tended to focus on one form of illiquidity to examine this relationship, our study unifies three forms of illiquidity at the same time. Indeed, we simultaneously consider illiquidity as systematic risk, as a characteristic of the market, and as a characteristic of the stock. The aggregate illiquidity of the market is the average of individual stock illiquidity. The illiquidity risk is the sensitivity of the stock price to illiquidity shocks. Shocks of market illiquidity are estimated by the innovations in the expected market illiquidity. Results show that investors on the Tunisian stock exchange do not require higher returns when they expect a rise of market illiquidity, whereas investors on U.S markets are compensated for higher expected market illiquidity. In addition, shocks of market illiquidity provoke a fall in stock prices of small caps, while large caps are not sensitive to market illiquidity shocks. This differs slightly from results based on U.S. data where illiquidity shocks reduce all stock prices but most notably those of small caps. Robustness tests validate our findings. Our results are consistent with previous studies which reported that the “zero-return” ratio predicts significantly the return-illiquidity relationship on emerging markets.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Illiquidity, Systematic risk, Stock return, Shocks, Robustness testing

Article History: Received 17 July 2021, Received in revised form 23 October 2021, Accepted 3 December 2021

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Soltane HB, Naoui K, and Alshammari A (2022). Systematic illiquidity, characteristic illiquidity, and stock returns: Timeseries analysis. International Journal of Advanced and Applied Sciences, 9(2): 72-80

Figures

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (29)

- Acharya VV and Pedersen LH (2005). Asset pricing with liquidity risk. Journal of Financial Economics, 77(2): 375-410. https://doi.org/10.1016/j.jfineco.2004.06.007 [Google Scholar]

- Acharya VV, Amihud Y, and Bharath ST (2013). Liquidity risk of corporate bond returns: Conditional approach. Journal of Financial Economics, 110(2): 358-386. https://doi.org/10.1016/j.jfineco.2013.08.002 [Google Scholar]

- Amihud Y (2002). Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets, 5(1): 31-56. https://doi.org/10.1016/S1386-4181(01)00024-6 [Google Scholar]

- Amihud Y (2019). Illiquidity and stock returns: A revisit. Critical Finance Review, 8(1-2): 203-221. https://doi.org/10.1561/104.00000073 [Google Scholar]

- Amihud Y and Mendelson H (1986). Asset pricing and the bid-ask spread. Journal of Financial Economics, 17(2): 223-249. https://doi.org/10.1016/0304-405X(86)90065-6 [Google Scholar]

- Amihud Y and Noh J (2021). Illiquidity and stock returns II: Cross-section and time-series effects. The Review of Financial Studies, 34(4): 2101-2123. https://doi.org/10.1093/rfs/hhaa080 [Google Scholar]

- Amihud Y, Hameed A, Kang W, and Zhang H (2015). The illiquidity premium: International evidence. Journal of Financial Economics, 117(2): 350-368. https://doi.org/10.1016/j.jfineco.2015.04.005 [Google Scholar]

- Asparouhova E, Bessembinder H, and Kalcheva I (2013). Noisy prices and inference regarding returns. The Journal of Finance, 68(2): 665-714. https://doi.org/10.1111/jofi.12010 [Google Scholar]

- Bekaert G, Harvey CR, and Lundblad C (2007). Liquidity and expected returns: Lessons from emerging markets. The Review of Financial Studies, 20(6): 1783-1831. https://doi.org/10.1093/rfs/hhm030 [Google Scholar]

- Blume ME and Stambaugh RF (1983). Biases in computed returns: An application to the size effect. Journal of Financial Economics, 12(3): 387-404. https://doi.org/10.1016/0304-405X(83)90056-9 [Google Scholar]

- Bongaerts D, De Jong F, and Driessen J (2012). An asset pricing approach to liquidity effects in corporate bond markets. https://doi.org/10.2139/ssrn.1762564 [Google Scholar]

- Brennan MJ and Subrahmanyam A (1996). Market microstructure and asset pricing: On the compensation for illiquidity in stock returns. Journal of Financial Economics, 41(3): 441-464. https://doi.org/10.1016/0304-405X(95)00870-K [Google Scholar]

- Brockman P, Chung DY, and Pérignon C (2009). Commonality in liquidity: A global perspective. Journal of Financial and Quantitative Analysis, 44(4): 851-882. https://doi.org/10.1017/S0022109009990123 [Google Scholar]

- Carhart MM (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1): 57-82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x [Google Scholar]

- Chordia T, Huh SW, and Subrahmanyam A (2009). Theory-based illiquidity and asset pricing. The Review of Financial Studies, 22(9): 3629-3668. https://doi.org/10.1093/rfs/hhn121 [Google Scholar]

- Chordia T, Roll R, and Subrahmanyam A (2000). Commonality in liquidity. Journal of Financial Economics, 56(1): 3-28. https://doi.org/10.1016/S0304-405X(99)00057-4 [Google Scholar]

- Datar VT, Naik NY, and Radcliffe R (1998). Liquidity and stock returns: An alternative test. Journal of Financial Markets, 1(2): 203-219. https://doi.org/10.1016/S1386-4181(97)00004-9 [Google Scholar]

- Farna EF and French KR (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1): 3-56. https://doi.org/10.1016/0304-405X(93)90023-5 [Google Scholar]

- Hasbrouck J and Seppi DJ (2001). Common factors in prices, order flows, and liquidity. Journal of Financial Economics, 59(3): 383-411. https://doi.org/10.1016/S0304-405X(00)00091-X [Google Scholar]

- Huberman G and Halka D (2001). Systematic liquidity. Journal of Financial Research, 24(2): 161-178. https://doi.org/10.1111/j.1475-6803.2001.tb00763.x [Google Scholar]

- Lee KH (2011). The world price of liquidity risk. Journal of Financial Economics, 99(1): 136-161. https://doi.org/10.1016/j.jfineco.2010.08.003 [Google Scholar]

- Lesmond DA (2005). The costs of equity trading in emerging markets. Journal of Financial Economics, 77(2): 411-452. https://doi.org/10.1016/j.jfineco.2004.01.005 [Google Scholar]

- Lesmond DA, Ogden JP, and Trzcinka CA (1999). A new estimate of transaction costs. The Review of Financial Studies, 12(5): 1113-1141. https://doi.org/10.1093/rfs/12.5.1113 [Google Scholar]

- Liu W (2006). A liquidity-augmented capital asset pricing model. Journal of Financial Economics, 82(3): 631-671. https://doi.org/10.1016/j.jfineco.2005.10.001 [Google Scholar]

- Lou X and Shu T (2017). Price impact or trading volume: Why is the Amihud (2002) measure priced? The Review of Financial Studies, 30(12): 4481-4520. https://doi.org/10.1093/rfs/hhx072 [Google Scholar]

- Loukil N, Zayani MB, and Omri A (2010). Impact of liquidity on stock returns: An empirical investigation of the Tunisian stock market. Macroeconomics and Finance in Emerging Market Economies, 3(2): 261-283. https://doi.org/10.1080/17520843.2010.498137 [Google Scholar]

- Pastor L and Stambaugh RF (2003). Liquidity risk and expected stock returns. Journal of Political Economy, 111(3): 642-685. https://doi.org/10.1086/374184 [Google Scholar]

- Tissaoui K, Ftiti Z, and Aloui C (2015). Commonality in liquidity: Lessons from an emerging stock market. Journal of Applied Business Research (JABR), 31(5): 1927-1952. https://doi.org/10.19030/jabr.v31i5.9410 [Google Scholar]

- Watanabe A and Watanabe M (2008). Time-varying liquidity risk and the cross section of stock returns. The Review of Financial Studies, 21(6): 2449-2486. https://doi.org/10.1093/rfs/hhm054 [Google Scholar]