International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 2 (February 2022), Pages: 31-40

----------------------------------------------

Original Research Paper

Title: Determinants of credit risk at Vietnam bank for agriculture and rural developments in Can Tho City

Author(s): Quang Vang Dang 1, Viet Thanh Truc Tran 2, Van Nam Mai 3, Long Hau Le 2, Quoc Duy Vuong 2, *

Affiliation(s):

1Faculty of Economics, University of Technology and Education, Ho Chi Minh City, Vietnam

2Department of Finance and Banking, College of Economics, Can Tho University, Can Tho, Vietnam

3Graduate School, Can Tho University, Can Tho, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-6870-4106

Corresponding author's ORCID profile: https://orcid.org/0000-0002-6870-4106

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.02.004

Abstract:

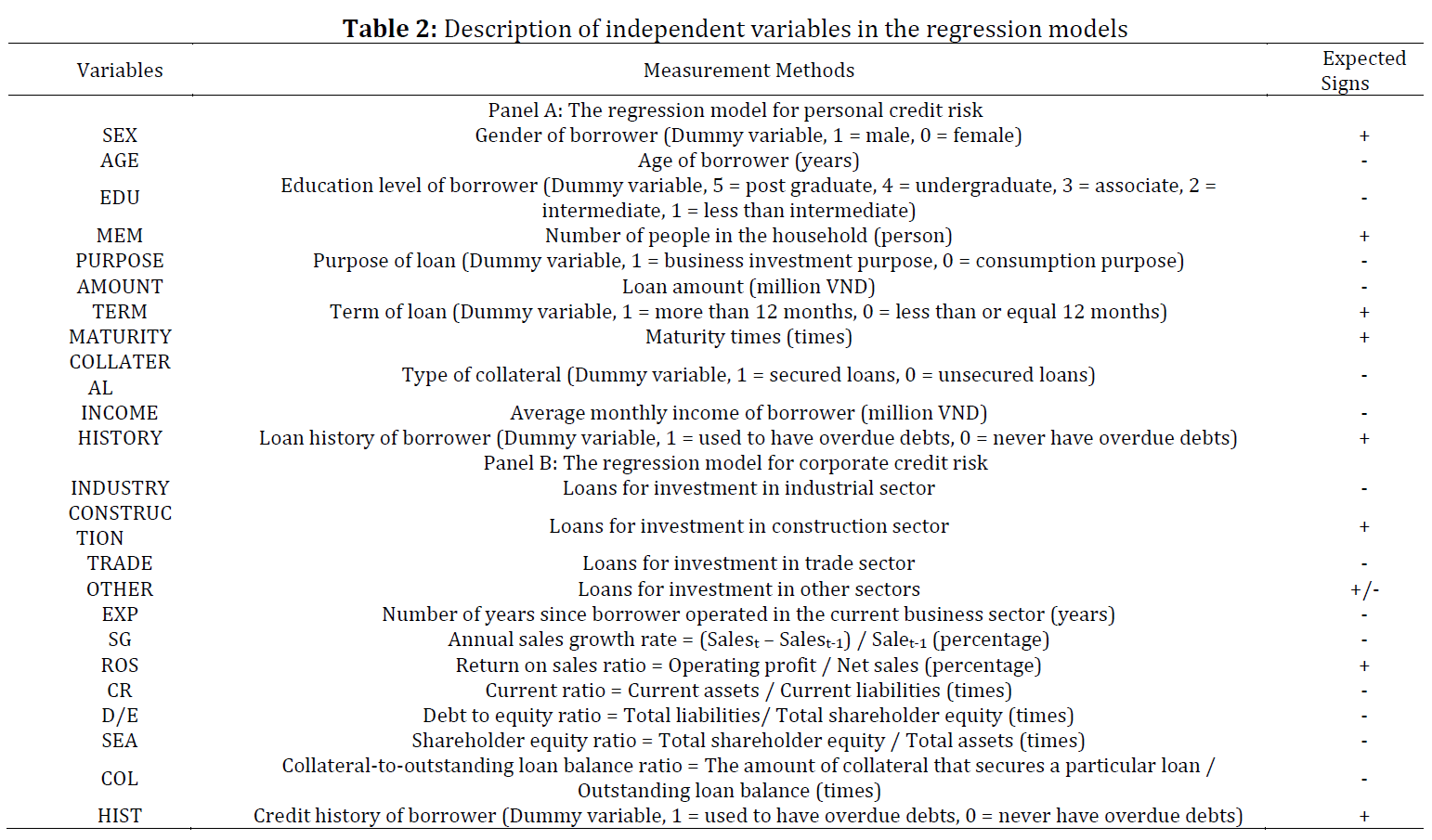

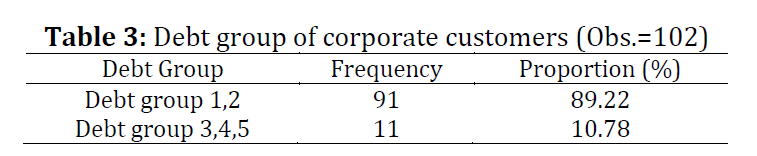

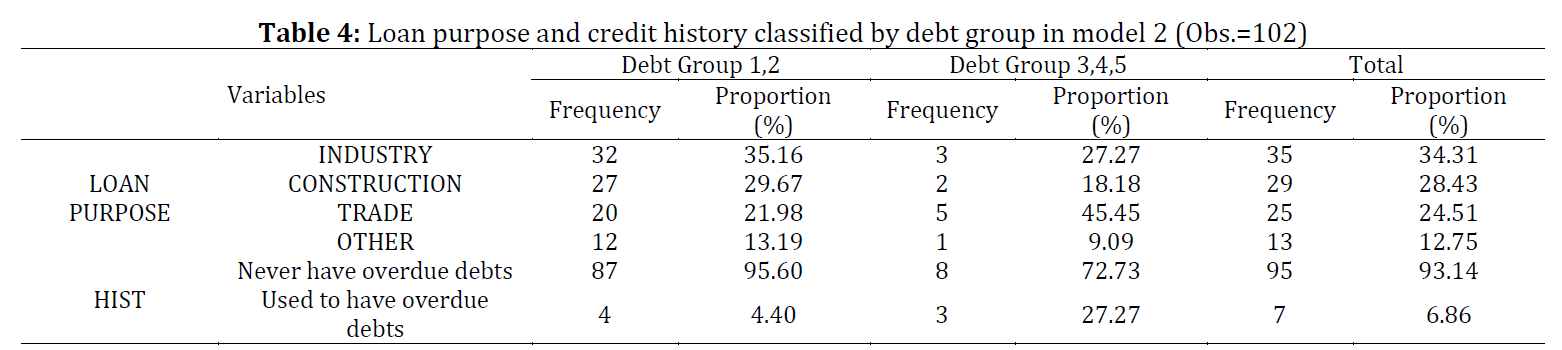

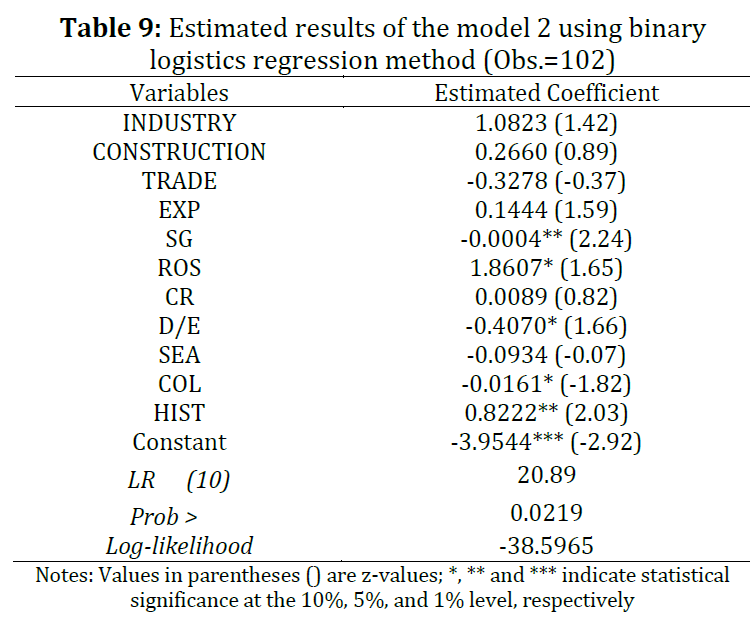

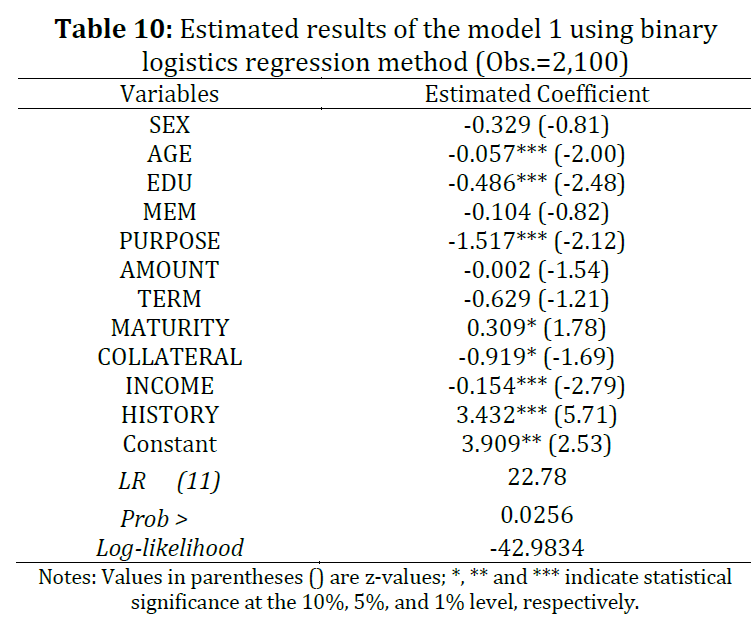

The aim of this study is to investigate factors affecting credit risks of the borrowers (both corporate and individual customers) of Vietnam bank for agriculture and rural development's branch at Can Tho city (lender), thereby proposing several solutions to improve the bank’s operational efficiency in the upcoming years. Simultaneous qualitative and quantitative research methods are applied and secondary data from 102 corporate customers and 2100 individual clients are collected directly from the financial report of the Can Tho branch of Vietnam bank for agriculture and rural development (Agribank) until the end of 2018. A binary logistics model is employed to identify the determinant factors of the credit risk of bank customers. Estimation results reveal that the credit risk of corporate customers is affected by the factors of sales growth, return on sales ratio, Debt to equity ratio, collateral-to-outstanding loan balance ratio, and customer's loan history which are consistent with those of previous studies, whereas the credit risk of individual customers is influenced by the factors of age, educational level, loan purpose, loan maturity, type of collateral, customer income, and customer loan history, which are confirmed by previous studies. The empirical findings of the article imply that the Can Tho branch of Agribank should take precautions in order to limit the credit risk of bank customers. In addition, several governance recommendations are given for bank’s manager to improve the operational efficiency of bank.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Credit risk, Binary logistics model, Commercial bank, Vietnam

Article History: Received 3 August 2021, Received in revised form 23 October 2021, Accepted 27 November 2021

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Dang QV, Tran VTT, and Mai VN et al. (2022). Determinants of credit risk at Vietnam bank for agriculture and rural developments in Can Tho City. International Journal of Advanced and Applied Sciences, 9(2): 31-40

Figures

No Figure

Tables

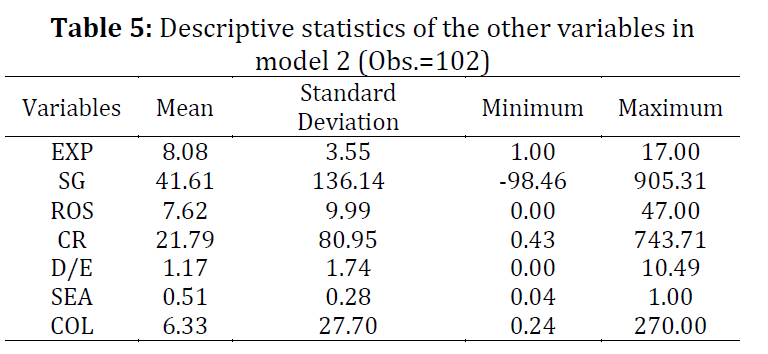

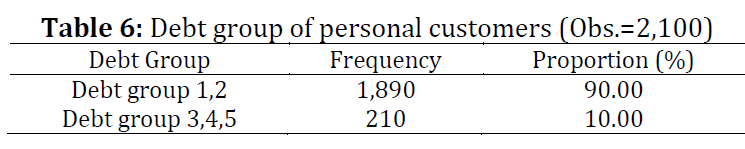

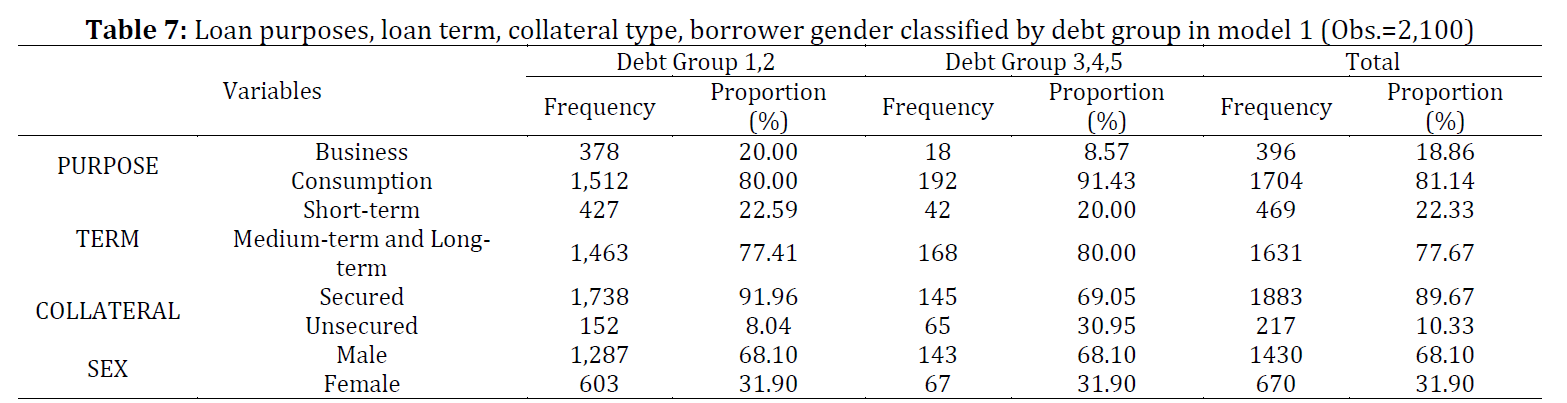

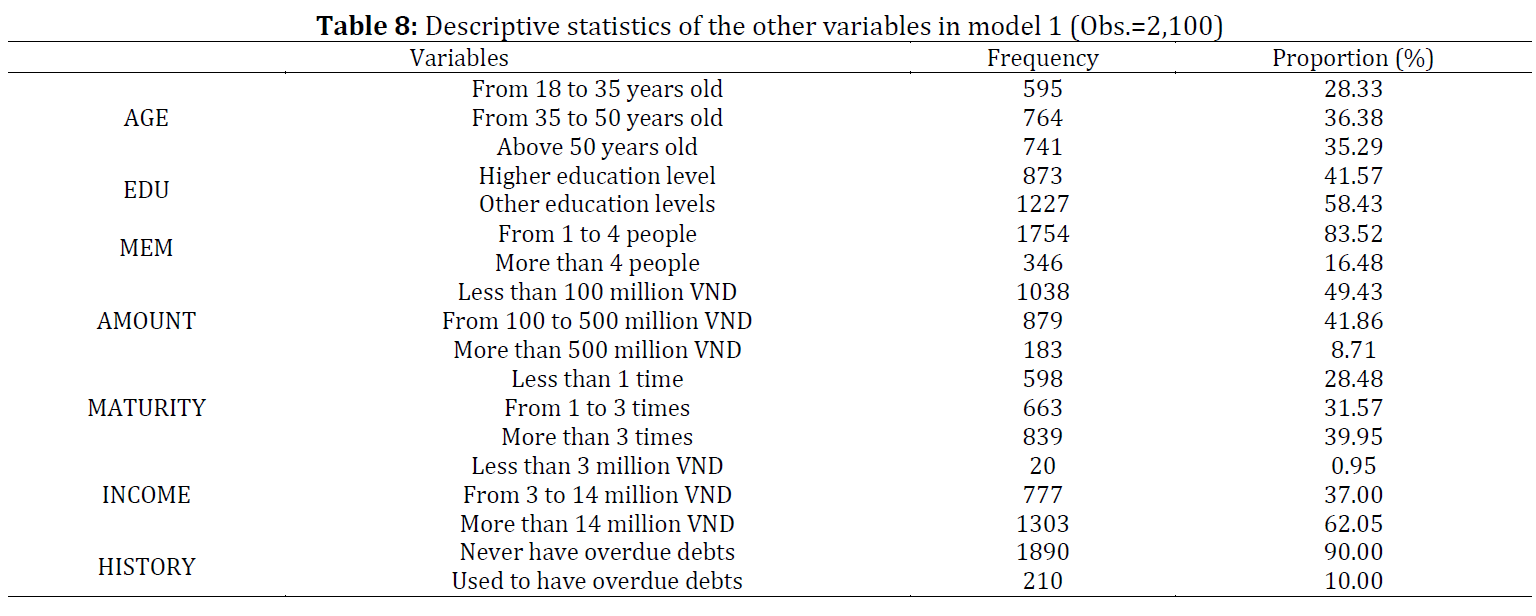

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9 Table 10

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (19)

- Ahmed F and Hassan A (2018). Determinants of credit risk: A study of Pakistan's Banking Sector. Muslim Perspectives, 3(4): 37-68. [Google Scholar]

- Bonfim D (2009). Credit risk drivers: Evaluating the contribution of firm level information and of macroeconomic dynamics. Journal of Banking and Finance, 33(2): 281-299. https://doi.org/10.1016/j.jbankfin.2008.08.006 [Google Scholar]

- Campa ADLA (2011). Increasing access to credit through reforming secured transactions in the MENA region. World Bank Policy Research Working Paper 5613, World Bank, Washington, USA. [Google Scholar]

- Chelagat KN (2012). Determinants of loan defaults by small and medium enterprises among commercial banks in Kenya. M.Sc. Thesis, University of Nairobi, Nairobi, Kenya. [Google Scholar]

- Habibi A and Hosseini SS (2016). Ranking bank customers using Neuro-Fuzzy network and optimization algorithms. International Journal of Advanced and Applied Sciences, 3(2): 40-44. [Google Scholar]

- Hamerle A, Liebig T, and Scheule H (2004). Forecasting credit portfolio risk. Deutsche Bundesbank, Frankfurt, Germany. https://doi.org/10.2139/ssrn.2793953 [Google Scholar]

- Himali LP (2020). Determinants of personal loan default and performance of the proportional hazards model with that of a random survival forest models. International Journal of Applied Science and Research, 3(4): 84-93. [Google Scholar]

- Kano M, Uchida H, Udell GF, and Watanabe W (2011). Information verifiability, bank organization, bank competition and bank–borrower relationships. Journal of Banking and Finance, 35(4): 935-954. https://doi.org/10.1016/j.jbankfin.2010.09.010 [Google Scholar]

- Menkhoff L, Neuberger D, and Suwanaporn C (2006). Collateral-based lending in emerging markets: Evidence from Thailand. Journal of Banking and Finance, 30(1): 1-21. https://doi.org/10.1016/j.jbankfin.2004.12.004 [Google Scholar]

- Nguyen TPT, Nghiem SH, and Roca E (2016). Management behaviour in Vietnamese commercial banks. Australian Economic Papers, 55(4): 345-367. https://doi.org/10.1111/1467-8454.12085 [Google Scholar]

- Oreski S, Oreski D, and Oreski G (2012). Hybrid system with genetic algorithm and artificial neural networks and its application to retail credit risk assessment. Expert Systems with Applications, 39(16): 12605-12617. https://doi.org/10.1016/j.eswa.2012.05.023 [Google Scholar]

- Perlin M, Righi M, and Filomena T (2019). A consumer credit risk structural model based on affordability: Balance at risk. Journal of Credit Risk, 15(2): 1-19. https://doi.org/10.21314/JCR.2018.244 [Google Scholar]

- Pham TT and Lensink R (2007). Lending policies of informal, formal and semiformal lenders. Economics of Transition, 15(2): 181-209. https://doi.org/10.1111/j.1468-0351.2007.00283.x [Google Scholar]

- Pindyck RS and Rubinfeld DL (1981). Econometric models and economic forecasts. McGraw-Hill, New York, USA. [Google Scholar]

- Rosch D (2003). Correlations and business cycles of credit risk: Evidence from bankruptcies in Germany. Financial Markets and Portfolio Management, 17(3): 309-331. https://doi.org/10.1007/s11408-003-0303-2 [Google Scholar]

- SBV (2013). Circular 02/2013/TT-NHNN on classification of assets, levels and method of setting up of risk provisions, and use of provisions against credit risks in the banking activity of credit institutions, foreign banks’ branches. State Bank of Vietnam, Hanoi, Vietnam. [Google Scholar]

- Tang TT (2009). Information asymmetry and firms’ credit market access: Evidence from Moody's credit rating format refinement. Journal of Financial Economics, 93(2): 325-351. https://doi.org/10.1016/j.jfineco.2008.07.007 [Google Scholar]

- Van Hon C (2020). Impact of credit rationing on capital allocated to inputs used by rice farmers in the Mekong River Delta, Vietnam. Journal of Economics and Development, 22(1). https://doi.org/10.1108/JED-11-2019-0067 [Google Scholar]

- Youn H and Gu Z (2010). Predicting Korean lodging firm failures: An artificial neural network model along with a logistic regression model. International Journal of Hospitality Management, 29(1): 120-127. https://doi.org/10.1016/j.ijhm.2009.06.007 [Google Scholar]