International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 9, Issue 12 (December 2022), Pages: 1-10

----------------------------------------------

Original Research Paper

Measuring stock performance using stochastic frontier analysis model with dependent error approach

Author(s): Roslah Arsad 1, *, Zaidi Isa 2, Nurul Hafizah Zainal Abidin 1, Norbaizura Kamarudin 3

Affiliation(s):

1Faculty of Computer and Mathematical Sciences, Universiti Teknologi MARA, Perak Branch, Tapah Campus, 35400 Tapah Road, Perak, Malaysia

2Faculty Sciences and Technology, School of Mathematical Sciences, Universiti Kebangsaan Malaysia, 43600 UKM Bangi, Selangor, Malaysia

3Faculty of Computer and Mathematical Sciences, Centre of Statistics and Decision Sciences Studies, Universiti Teknologi MARA, 40450 Shah Alam, Selangor, Malaysia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-1080-3600

Corresponding author's ORCID profile: https://orcid.org/0000-0003-1080-3600

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2022.12.001

Abstract:

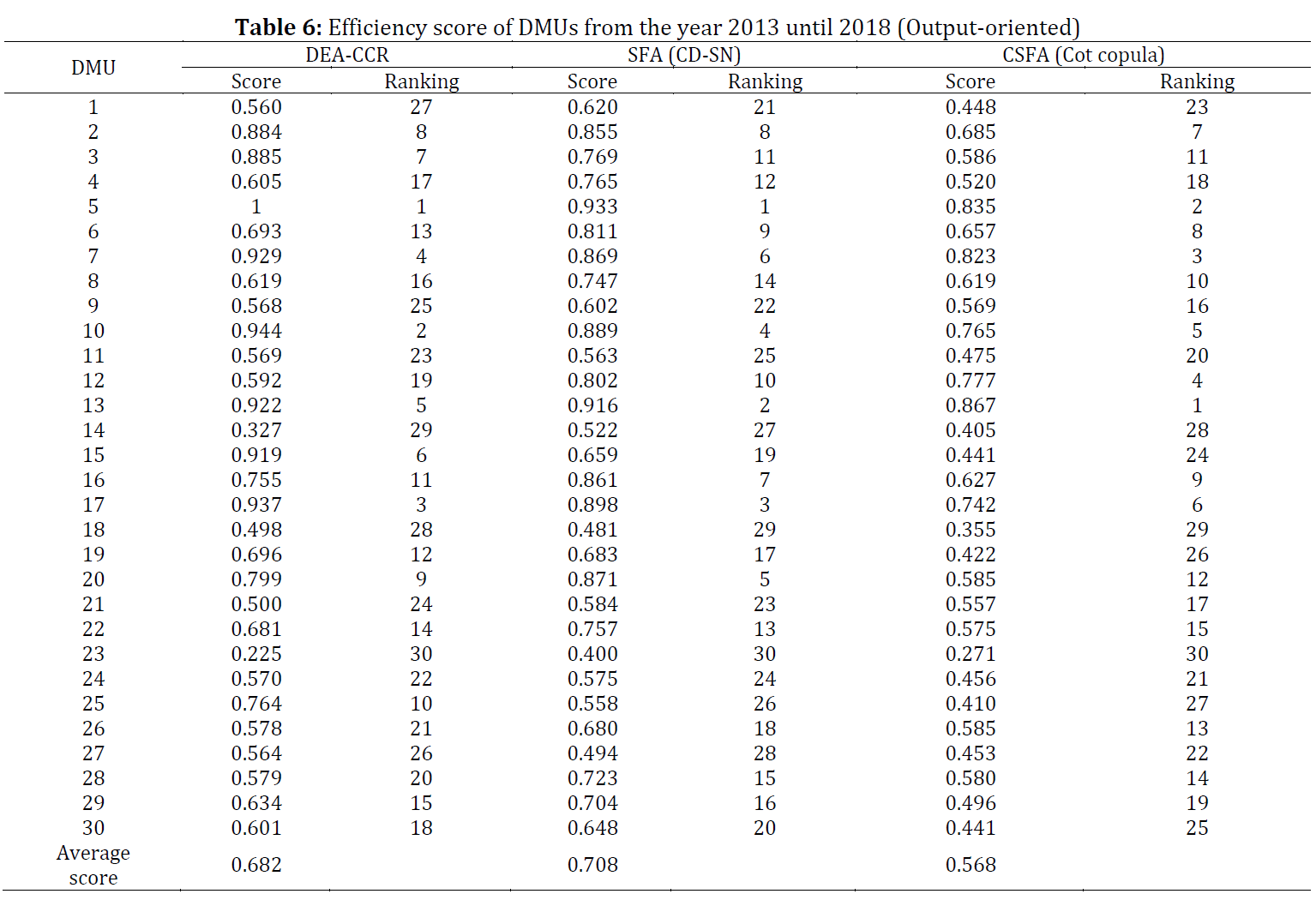

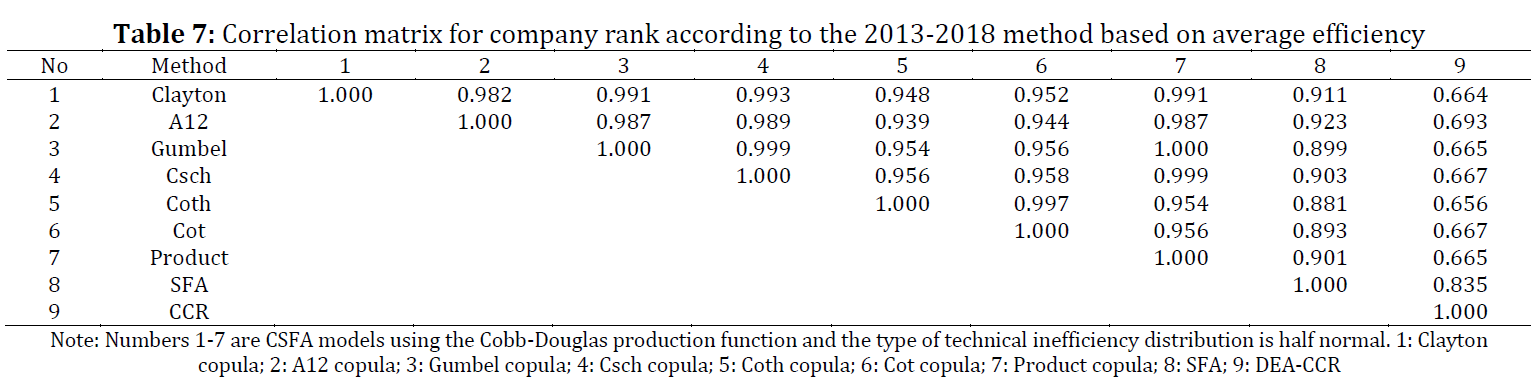

This paper focuses on analyzing the technical efficiency of Malaysian stock performance over the period of 2013 to 2018. By utilizing the stochastic frontier analysis (SFA) production function Cobb-Douglas, the inefficiency effect of time-invariant is allowed and predicted to estimate the technical efficiency score as well as provide a ranking efficiency based on the model estimation performance. In SFA, the two main errors, random error and inefficiency error are assumed to be independent, and this assumption is not practical in a real-life situation. The assumption for random error is normally distributed and the inefficiency error is half-normal distributed. Therefore, in this paper, when the assumption of SFA is dependent on both errors, the copula is applied to capture the joint distribution of these two error components. These main findings revealed that stock efficiency estimates using copula SFA (CSFA) are appropriate because it uses more practical assumptions and among the seven models, through the AIC method, the Cot copula was selected as the best model. This paper provides new evidence on comparison ranking of technical efficiency based on the three models, yielded by copulas with SFA (CSFA-Cot copula), SFA, and DEA-CCR models. Spearman’s rank order was implemented and revealed that there was a high degree of correlation found among the rank efficiency estimates derived from the models of CSFA and SFA applied. However, the scores produced by both models are different. Accurate scores are necessary in order to make correct decisions and predictions. Therefore, the dependence error between random error and inefficiency error cannot be ignored, and the Cot copula in SFA models can be considered as an alternative suitable tool for measuring efficiency performance.

© 2022 The Authors. Published by IASE.

This is an

Keywords: Efficiency, Performance, Copula, Stochastic frontier analysis, Dependent error

Article History: Received 12 September 2021, Received in revised form 7 August 2022, Accepted 11 August 2022

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Arsad R, Isa Z, Abidin NHZ, and Kamarudin N (2022). Measuring stock performance using stochastic frontier analysis model with dependent error approach. International Journal of Advanced and Applied Sciences, 9(12): 1-10

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (40)

- Aigner D, Lovell CK, and Schmidt P (1977). Formulation and estimation of stochastic frontier production function models. Journal of Econometrics, 6(1): 21-37. https://doi.org/10.1016/0304-4076(77)90052-5 [Google Scholar]

- Banker RD, Charnes A, and Cooper WW (1984). Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science, 30(9): 1078-1092. https://doi.org/10.1287/mnsc.30.9.1078 [Google Scholar]

- Baten MA, Maznah MK, Razamin R, and Jastini MJ (2014). Evaluating Kuala Lumpur stock exchange oriented bank performance with stochastic frontiers. In AIP Conference Proceedings, American Institute of Physics, 1635(1): 294-300. https://doi.org/10.1063/1.4903598 [Google Scholar]

- Bhandari LC (1988). Debt/equity ratio and expected common stock returns: Empirical evidence. The Journal of Finance, 43(2): 507-528. https://doi.org/10.1111/j.1540-6261.1988.tb03952.x [Google Scholar]

- Charnes A, Cooper WW, and Rhodes E (1978). Measuring the efficiency of decision making units. European Journal of Operational Research, 2(6): 429-444. https://doi.org/10.1016/0377-2217(78)90138-8 [Google Scholar]

- Delen D, Kuzey C, and Uyar A (2013). Measuring firm performance using financial ratios: A decision tree approach. Expert Systems with Applications, 40(10): 3970-3983. https://doi.org/10.1016/j.eswa.2013.01.012 [Google Scholar]

- Dias A (2013). Market capitalization and value-at-risk. Journal of Banking and Finance, 37(12): 5248-5260. https://doi.org/10.1016/j.jbankfin.2013.04.015 [Google Scholar]

- El Mehdi R and Hafner CM (2014). Inference in stochastic frontier analysis with dependent error terms. Mathematics and Computers in Simulation, 102: 104-116. https://doi.org/10.1016/j.matcom.2013.09.008 [Google Scholar]

- Fairfield PM and Yohn TL (2001). Using asset turnover and profit margin to forecast changes in profitability. Review of Accounting Studies, 6(4): 371-385. https://doi.org/10.1023/A:1012430513430 [Google Scholar]

- Gardijan M and Kojić V (2012). DEA-based investment strategy and its application in the Croatian stock market. Croatian Operational Research Review, 3(1): 203-212. [Google Scholar]

- Greene WH (1990). A gamma-distributed stochastic frontier model. Journal of Econometrics, 46(1-2): 141-163. https://doi.org/10.1016/0304-4076(90)90052-U [Google Scholar]

- Hamidi S (2016). Measuring efficiency of governmental hospitals in Palestine using stochastic frontier analysis. Cost Effectiveness and Resource Allocation, 14(1): 1-12. https://doi.org/10.1186/s12962-016-0052-5 [Google Scholar] PMid:26848283 PMCid:PMC4741008

- Hasan BAL and Najjari V (2013). Archimedean copulas family via hyperbolic generator. Gazi University Journal of Science, 26(2): 195-200. [Google Scholar]

- Hasan M and Kamil AA (2014). Contribution of co-skewness and co-kurtosis of the higher moment CAPM for finding the technical efficiency. Economics Research International, 2014: 253527. https://doi.org/10.1155/2014/253527 [Google Scholar]

- Hasan MZ, Kamil AA, Mustafa A, and Baten MA (2012a). Estimating stock market technical efficiency for truncated normal distribution: Evidence from Dhaka stock exchange. Trends in Applied Sciences Research, 7(7): 532-540. https://doi.org/10.3923/tasr.2012.532.540 [Google Scholar]

- Hasan MZ, Kamil AA, Mustafa A, and Baten MA (2012b). Stochastic frontier model approach for measuring stock market efficiency with different distributions. PLOS ONE, 7(5): e37047. https://doi.org/10.1371/journal.pone.0037047 [Google Scholar] PMid:22629352 PMCid:PMC3355172

- Iliyasu A, Mohamed ZA, Ismail MM, Amin AM, and Mazuki H (2016). Technical efficiency of cage fish farming in Peninsular Malaysia: A stochastic frontier production approach. Aquaculture Research, 47(1): 101-113. https://doi.org/10.1111/are.12474 [Google Scholar]

- Ismail MKA, Abd Rahman NMN, Salamudin N, and Kamaruddin BH (2012). DEA portfolio selection in Malaysian stock market. In the 2012 International Conference on Innovation Management and Technology Research, IEEE, Malacca, Malaysia: 739-743. https://doi.org/10.1109/ICIMTR.2012.6236492 [Google Scholar]

- Janang JT, Tinggi M, and Kun A (2018). Technical inefficiency effects of corporate governance on government linked companies in Malaysia. International Journal of Business and Society, 19(3): 918-936. [Google Scholar]

- Jondrow J, Lovell CK, Materov IS, and Schmidt P (1982). On the estimation of technical inefficiency in the stochastic frontier production function model. Journal of Econometrics, 19(2-3): 233-238. https://doi.org/10.1016/0304-4076(82)90004-5 [Google Scholar]

- Leurcharusmee S, Sirisrisakulchai J, and Pruekruedee S (2016). Firm efficiency in Thailand’s telecommunication industry: Application of the stochastic frontier model with dependence in time and error components. In: Huynh VN, Kreinovich V, and Sriboonchitta S (Eds.), Causal inference in econometrics: studies in computational intelligence: 495-505. Volume 622, Springer, Cham, Switzerland. https://doi.org/10.1007/978-3-319-27284-9_32 [Google Scholar]

- Md ZH, Anton AK, and Azizul B (2011). Measuring Dhaka stock exchange market efficiency: A stochastic frontier analysis. African Journal of Business Management, 5(22): 8891-8901. https://doi.org/10.5897/AJBM11.313 [Google Scholar]

- Meeusen W and van Den Broeck J (1977). Efficiency estimation from Cobb-Douglas production functions with composed error. International Economic Review, 18(2): 435-444. https://doi.org/10.2307/2525757 [Google Scholar]

- Mokhtar K, Ruslan SMM, Ahmad WMAW, Abdullah Z, Mokhlis S, May KS, and Abdullah MA (2020). Measuring terminal efficiency: Case of fishing ports in Malaysia. International Journal of Advanced and Applied Sciences, 7(3): 89-103. https://doi.org/10.21833/ijaas.2020.03.010 [Google Scholar]

- Mokhtar M, Shuib A, and Mohamad D (2014). Identifying the critical financial ratios for stocks evaluation: A fuzzy Delphi approach. In AIP Conference Proceedings, American Institute of Physics, 1635(1): 348-354. https://doi.org/10.1063/1.4903606 [Google Scholar]

- Murillo‐Zamorano LR (2004). Economic efficiency and frontier techniques. Journal of Economic Surveys, 18(1): 33-77. https://doi.org/10.1111/j.1467-6419.2004.00215.x [Google Scholar]

- Najjari V, Bacigál T, and Bal H (2014). An Archimedean copula family with hyperbolic cotangent generator. International Journal of Uncertainty, Fuzziness and Knowledge-Based Systems, 22(5): 761-768. https://doi.org/10.1142/S0218488514500391 [Google Scholar]

- Najjari V, Bal H, Özturk F, and Alp I (2016). Stochastic frontier models by copulas and an application. Scientific Bulletin, 78(1): 31-41. [Google Scholar]

- Pirmoradian A and Hamzah A (2011). Simulation of tail dependence in cot-copula. In the Proceedings of the 58th WSC of the ISI. Dublin, Ireland: 4277– 4282. [Google Scholar]

- Reinganum MR (1983). Portfolio strategies based on market capitalization. The Journal of Portfolio Management, 9(2): 29-36. https://doi.org/10.3905/jpm.1983.408902 [Google Scholar]

- Riedl EJ and Srinivasan S (2010). Signaling firm performance through financial statement presentation: An analysis using special items. Contemporary Accounting Research, 27(1): 289-332. https://doi.org/10.1111/j.1911-3846.2010.01009.x [Google Scholar]

- Ritter C and Simar L (1997). Pitfalls of normal-gamma stochastic frontier models. Journal of Productivity Analysis, 8(2): 167-182. https://doi.org/10.1023/A:1007751524050 [Google Scholar]

- Smith MD (2008). Stochastic frontier models with dependent error components. The Econometrics Journal, 11(1): 172-192. https://doi.org/10.1111/j.1368-423X.2007.00228.x [Google Scholar]

- Tibprasorn P, Autchariyapanitkul K, and Sriboonchitta S (2017). Stochastic frontier model in financial econometrics: A copula-based approach. In: Kreinovich V, Sriboonchitta S, and Huynh VN (Eds.), Robustness in econometrics: 575-586. Springer, Cham, Switzerland. https://doi.org/10.1007/978-3-319-50742-2_35 [Google Scholar]

- Tibprasorn P, Autchariyapanitkul K, Chaniam S, and Sriboonchitta S (2015). A copula-based stochastic frontier model for financial pricing. In: Huynh VN, Inuiguchi M, Demoeux T (Eds.), International symposium on integrated uncertainty in knowledge modelling and decision making: 151-162. Springer, Cham, Switzerland. https://doi.org/10.1007/978-3-319-25135-6_15 [Google Scholar]

- Tibprasorn P, Chanaim S, and Sriboonchitta S (2016). A copula-based stochastic frontier model and efficiency analysis: Evidence from stock exchange of Thailand. In: Huynh VN, Inuiguchi M, Demoeux T (Eds.), International symposium on integrated uncertainty in knowledge modelling and decision making: 637-648. Springer, Cham, Switzerland. https://doi.org/10.1007/978-3-319-49046-5_54 [Google Scholar]

- Wan Ahmad WMA, Mamat M, and Isa Z (2010). Analisis kecekapan relatif bagi industri saham amanah menggunakan pendekatan ekonometrik. International Journal of Management Studies, 17(1): 189-202. [Google Scholar]

- Wiboonpongse A, Liu J, Sriboonchitta S, and Denoeux T (2015). Modeling dependence between error components of the stochastic frontier model using copula: Application to intercrop coffee production in Northern Thailand. International Journal of Approximate Reasoning, 65: 34-44. https://doi.org/10.1016/j.ijar.2015.04.001 [Google Scholar]

- Yang HH (2010). Measuring the efficiencies of Asia–Pacific international airports–Parametric and non-parametric evidence. Computers and Industrial Engineering, 59(4): 697-702. https://doi.org/10.1016/j.cie.2010.07.023 [Google Scholar]

- Zohdi M, Marjani AB, Najafabadi AM, Alvani J, and Dalv MR (2012). Data envelopment analysis (DEA) based performance evaluation system for investment companies: Case study of Tehran Stock Exchange. African Journal of Business Management, 6(16): 5573–5577. https://doi.org/10.5897/AJBM11.3036 [Google Scholar]