International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 8, Issue 9 (September 2021), Pages: 15-28

----------------------------------------------

Original Research Paper

Title: Practices and mechanisms to mitigate the negative effects of accounting-based earnings management: An empirical study from the professionals’ perspective

Author(s): Albertina Paula Monteiro 1, *, Orlando Lima Rua 2, José Carlos Figueira 3, Eduardo Leite 4

Affiliation(s):

1Porto Accounting and Business School, Polytechnic of Porto, CEOS.PP, Porto, Portugal

2Porto Accounting and Business School, Polytechnic of Porto, CEOS.PP, UNIAG, APNOR, Porto, Portugal

3Porto Accounting and Business School, Polytechnic of Porto, Porto, Portugal

4Higher School Technology and Management, University of Madeira, CiTUR, Funchal, Portugal

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-2146-9807

Corresponding author's ORCID profile: https://orcid.org/0000-0002-2146-9807

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2021.09.003

Abstract:

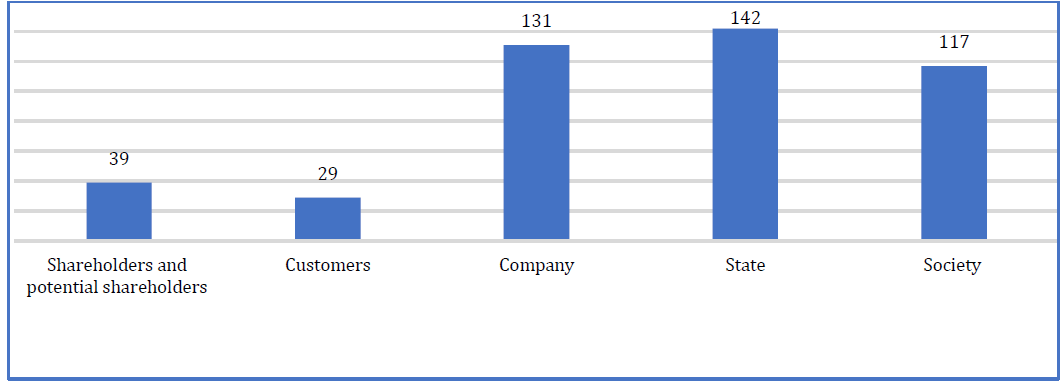

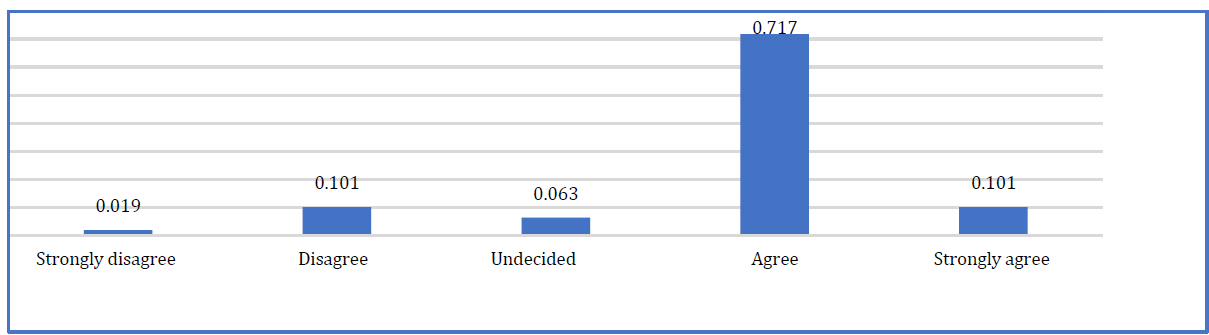

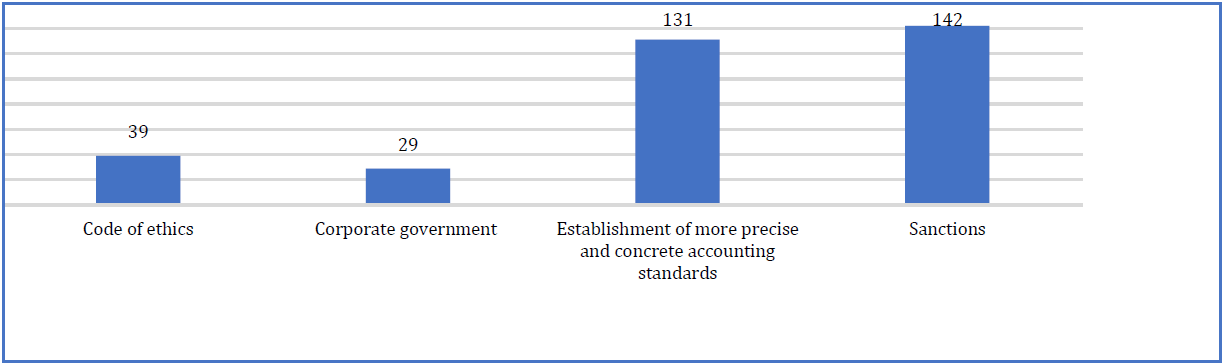

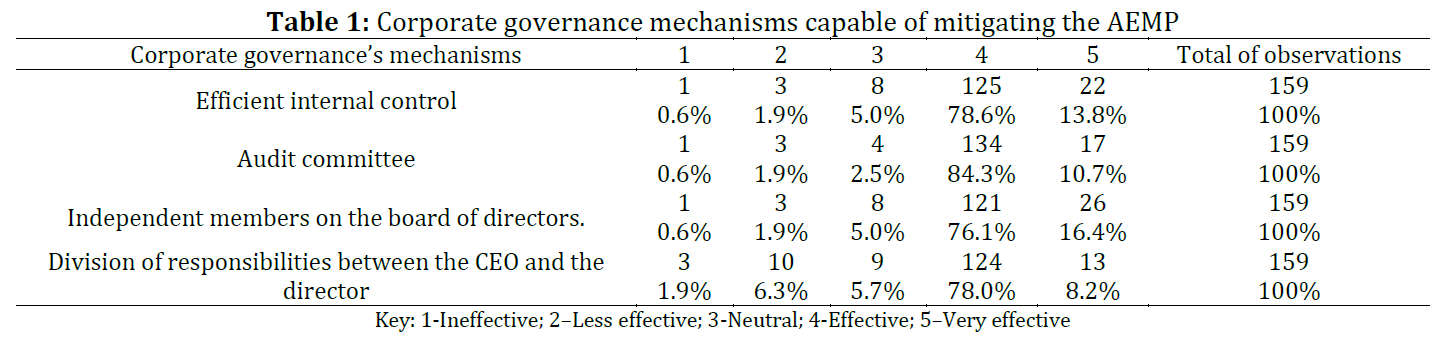

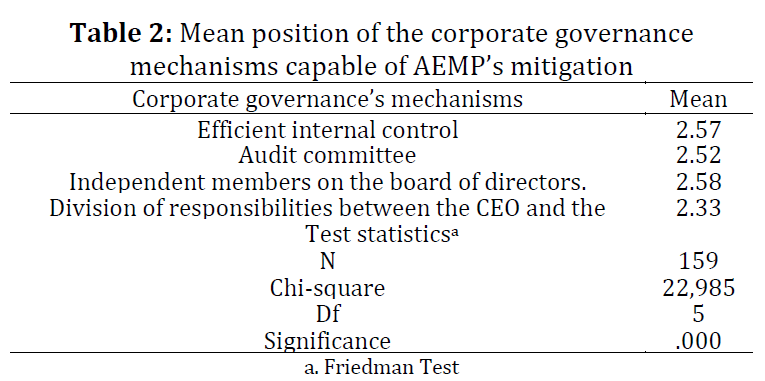

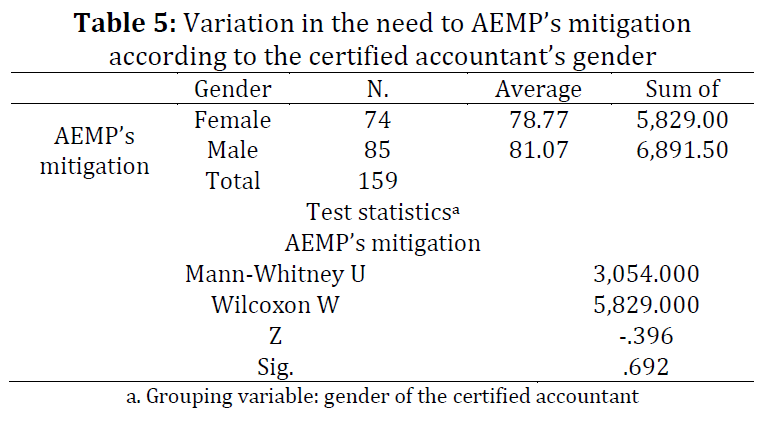

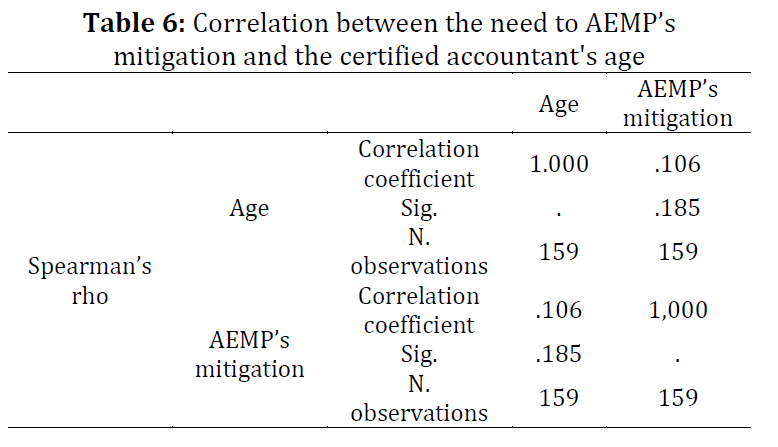

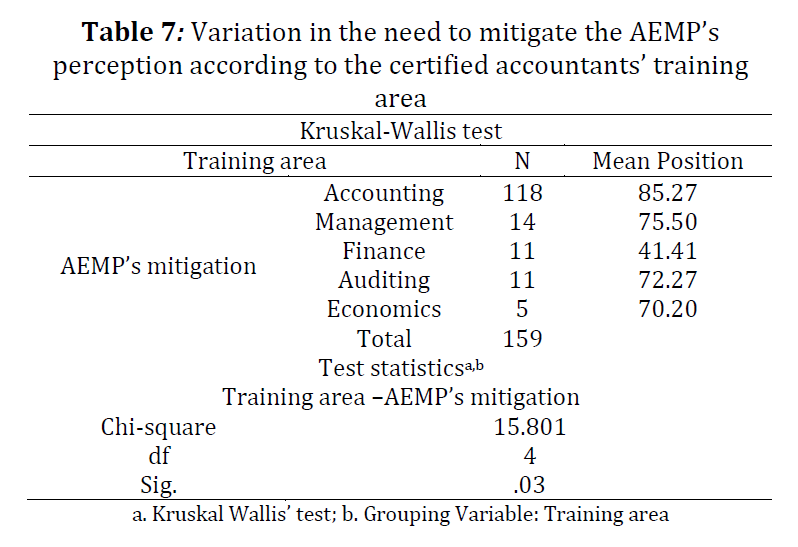

Accounting conservatism and Accounting-based Earnings Management Practices (AEMP) introduce bias in financial information (FI), thereby influencing stakeholder behavior in the decision-making process. This study aims to analyze, from the certified accountants’ perspective, the AEMP in Portugal. Specifically, it analyses (1) the development of the AEMP and its impact on FI reporting, (2) the main hampered on its implementation, and (3) the need for the instruments and corporate governance mechanisms to mitigate the AEMP. Besides this research analyses (4) the relationship between the certified accountant’s characteristics (gender, age, professional experience, educational qualifications, and training area. To achieve the proposed objectives, we have used a quantitative methodological approach with a survey questionnaire, conducting an empirical study based on a sample of certified accountants. Based on a sample of 159 certified accountants, the results found that the majority of respondents indicate that Portuguese companies develop AEMP and that these practices have a negative and significant impact on the quality of financial statements (FS). Moreover, most certified accountants point out that is important to adopt measures that will prevent the abuse of AEMP and the main instruments for this are the establishments of more precise and concrete accounting standards and the application of the sanctions. The results also indicate that the audit committee and efficient internal control are corporate governance mechanisms AEMP able of mitigating the effects of the AEMP. Finally, the individual characteristics of certified accountants, such as professional experience, educational qualifications, and training area, significantly influence their perception of the need to mitigate the AEMP. This study presents relevant contributions to theory and practice. First, it develops the literature that evaluates AEMP, particularly in Portugal, where studies are scarce. Second, this study is original because it considers the relationship characteristics of accounting and AEMP professionals. Third, it allows entities that operate in accounting standardization and for accountants and FI users to have a more in-depth knowledge of the AEMP’s instruments and mechanisms.

© 2021 The Authors. Published by IASE.

This is an

Keywords: Accounting practices and mechanisms, Accounting standards, Certified accountants, Earnings management

Article History: Received 2 February 2021, Received in revised form 25 May 2021, Accepted 27 May 2021

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Monteiro AP, Rua OL, and Figueira JC et al. (2021). Practices and mechanisms to mitigate the negative effects of accounting-based earnings management: An empirical study from the professionals’ perspective. International Journal of Advanced and Applied Sciences, 8(9): 15-28

Figures

Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (77)

- Ababneh TEAM and Aga M (2019). The impact of sustainable financial data governance, political connections, and creative accounting practices on organizational outcomes. Sustainability, 11(20): 5676. https://doi.org/10.3390/su11205676 [Google Scholar]

- Akpanuko EE and Umoren NJ (2018). The influence of creative accounting on the credibility of accounting reports. Journal of Financial Reporting and Accounting, 16(2): 293-310. https://doi.org/10.1108/JFRA-08-2016-0064 [Google Scholar]

- Al Momani MA and Obeidat MI (2013). The effect of auditors' ethics on their detection of creative accounting practices: A field study. International Journal of Business and Management, 8(13): 118-136. https://doi.org/10.5539/ijbm.v8n13p118 [Google Scholar]

- Al-Haddad L and Whittington M (2019). The impact of corporate governance mechanisms on real and accrual earnings management practices: Evidence from Jordan. Corporate Governance, 19(6): 1167-1186. https://doi.org/10.1108/CG-05-2018-0183 [Google Scholar]

- Amat O, Blake J, and Gutiérrez SM (1996). La contabilidad creativa en España y en el Reino Unido: Un estudio comparativo. Management Review Barcelona, 3: 68-75. [Google Scholar]

- Beasley MS (1996). An empirical analysis of the relation between the board of director composition and financial statement fraud. Accounting Review, 71: 443-465. [Google Scholar]

- Bhasin ML (2016). Creative accounting practices: An empirical study of India. European Journal of Accounting, Finance and Business, 4(1): 10–30. [Google Scholar]

- Breton G and Taffler RJ (1995). Creative accounting and investment analyst response. Accounting and Business Research, 25(98): 81-92. https://doi.org/10.1080/00014788.1995.9729931 [Google Scholar]

- Cepêda CLM and Monteiro AP (2020). The accountant’s perception of the usefulness of financial information in decision making-a study in Portugal. Revista Brasileira de Gestão de Negócios, 22(2): 363-380. https://doi.org/10.7819/rbgn.v22i2.4050 [Google Scholar]

- Christie AA and Zimmerman JL (1994). Efficient and opportunistic choices of accounting procedures: Corporate control contests. Accounting Review, 69: 539-566. [Google Scholar]

- Dahya J, Lonie AA, and Power DM (1996). The case for separating the roles of chairman and CEO: An analysis of stock market and accounting data. Corporate Governance: An International Review, 4(2): 71-77. https://doi.org/10.1111/j.1467-8683.1996.tb00136.x [Google Scholar]

- Dai L and Ngo P (2021). Political uncertainty and accounting conservatism. European Accounting Review, 30(2): 277-307. https://doi.org/10.1080/09638180.2020.1760117 [Google Scholar]

- Davidson R, Goodwin‐Stewart J, and Kent P (2005). Internal governance structures and earnings management. Accounting and Finance, 45(2): 241-267. https://doi.org/10.1111/j.1467-629x.2004.00132.x [Google Scholar]

- Dechow PM, Sloan RG, and Sweeney AP (1996). Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research, 13(1): 1-36. https://doi.org/10.1111/j.1911-3846.1996.tb00489.x [Google Scholar]

- Desai H, Hogan CE, and Wilkins MS (2006). The reputational penalty for aggressive accounting: Earnings restatements and management turnover. The Accounting Review, 81(1): 83-112. https://doi.org/10.2308/accr.2006.81.1.83 [Google Scholar]

- Duréndez A and Madrid-Guijarro A (2018). The impact of family influence on financial reporting quality in small and medium family firms. Journal of Family Business Strategy, 9(3): 205-218. https://doi.org/10.1016/j.jfbs.2018.08.002 [Google Scholar]

- Ewert R and Wagenhofer A (2012). Earnings management, conservatism, and earnings quality. Foundations and Trends® in Accounting, 6(2): 65-186. https://doi.org/10.1561/1400000025 [Google Scholar]

- Figueira JC, Monteiro AP, and Rua OL (2021). Earnings management practices: The certified accountant’s perspective. Portuguese Journal of Finance, Management and Accounting, 7(13): 3-26. [Google Scholar]

- Ge R, Seybert N, and Zhang F (2019). Investor sentiment and accounting conservatism. Accounting Horizons, 33(1): 83-102. https://doi.org/10.2308/acch-52250 [Google Scholar]

- Gowthorpe C and Amat O (2005). Creative accounting: Some ethical issues of macro-and micro-manipulation. Journal of Business Ethics, 57(1): 55-64. https://doi.org/10.1007/s10551-004-3822-5 [Google Scholar]

- Gutiérrez AL and Rodríguez MC (2019). A review on the multidimensional analysis of earnings quality. Revista de Contabilidad-Spanish Accounting Review, 22(1): 41-60. https://doi.org/10.6018/rc-sar.22.1.354301 [Google Scholar]

- Halabi H, Alshehabi A, and Zakaria I (2019). Informal institutions and managers’ earnings management choices: Evidence from IFRS-adopting countries. Journal of Contemporary Accounting and Economics, 15(3): 100162. https://doi.org/10.1016/j.jcae.2019.100162 [Google Scholar]

- Haw IM, Ho SS, and Li AY (2011). Corporate governance and earnings management by classification shifting. Contemporary Accounting Research, 28(2): 517-553. https://doi.org/10.1111/j.1911-3846.2010.01059.x [Google Scholar]

- Healy PM (1985). The effect of bonus schemes on accounting decisions. Journal of Accounting and Economics, 7(1-3): 85-107. https://doi.org/10.1016/0165-4101(85)90029-1 [Google Scholar]

- Hill A and Hill MM (2008). Investigação por questionário. 2nd Edition. Edições Silabo, Lisbon, Portugal. [Google Scholar]

- Jackson K (2010). The scandal beneath the crisis: Getting a view from a cultural-moral mental model. Harvard Journal of Law and Public Policy, 33(2): 735–778. [Google Scholar]

- Jaggi B and Leung S (2007). Impact of family dominance on monitoring of earnings management by audit committees: Evidence from Hong Kong. Journal of International Accounting, Auditing and Taxation, 16(1): 27-50. https://doi.org/10.1016/j.intaccaudtax.2007.01.003 [Google Scholar]

- Jawad FA and Xia X (2015). International financial reporting standards and moral hazard of creative accounting on hedging. International Journal of Finance and Accounting, 4(1): 60-70. [Google Scholar]

- Jensen MC (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2): 323-329. [Google Scholar]

- Jensen MC and Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4): 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [Google Scholar]

- Jiang W, Lee P, and Anandarajan A (2008). The association between corporate governance and earnings quality: Further evidence using the GOV-Score. Advances in Accounting, 24(2): 191-201. https://doi.org/10.1016/j.adiac.2008.08.011 [Google Scholar]

- Jones M (2011). Creative accounting, fraud and international accounting scandals. John Wiley and Sons, London, UK. https://doi.org/10.1002/9781119208907 [Google Scholar]

- Knežević G, Mizdraković V, and Arežina N (2012). Management as cause and instrument of creative accounting suppression. Management-časopis Za Teoriju I Praksu Menadžmenta, 17(62): 89-95. https://doi.org/10.7595/management.fon.2012.0001 [Google Scholar]

- Kontesa M, Lako A, and Wendy W (2020). Board capital and earnings quality with different controlling shareholders. Accounting Research Journal, 33(4/5): 593-613. https://doi.org/10.1108/ARJ-01-2020-0017 [Google Scholar]

- Kousenidis DV, Ladas AC, and Negakis CI (2013). The effects of the European debt crisis on earnings quality. International Review of Financial Analysis, 30: 351-362. https://doi.org/10.1016/j.irfa.2013.03.004 [Google Scholar]

- Lafond R and Roychowdhury S (2008). Managerial ownership and accounting conservatism. Journal of accounting research, 46(1): 101-135. https://doi.org/10.1111/j.1475-679X.2008.00268.x [Google Scholar]

- Lai L and Tam H (2007). Independent directors and the propensity to smooth earnings: A study of corporate governance in China. The Business Review, 7(1): 328-335. [Google Scholar]

- Li CW and Chao YY (2020). The effect of auditing assurance levels on accounting conservatism: Evidence from Taiwan. International Journal of System Assurance Engineering and Management, 11(1): 64-76. https://doi.org/10.1007/s13198-019-00925-3 [Google Scholar]

- Li K, Niskanen J, and Niskanen M (2019). Capital structure and firm performance in European SMEs: Does credit risk make a difference? Managerial Finance, 45(5): 582-601. https://doi.org/10.1108/MF-01-2017-0018 [Google Scholar]

- Lourenço IC, Branco MC, and Curto JD (2018). Timely reporting and family ownership: The Portuguese case. Meditari Accountancy Research, 26 (1): 170-192. https://doi.org/10.1108/MEDAR-05-2016-0058 [Google Scholar]

- Malikov K, Manson S, and Coakley J (2018). Earnings management using classification shifting of revenues. The British Accounting Review, 50(3): 291-305. https://doi.org/10.1016/j.bar.2017.10.004 [Google Scholar]

- Marconi M and Lakatos E (2011). Fundamentos de metodologia científica. Editora Atlas, São Paulo, Brazil. [Google Scholar]

- Martins C (2011). Manual de análise de dados quantitativos com recurso ao IBM SPSS: Saber decidir, fazer, interpretar e redigir. Psiquilíbrios Edições, Braga, Portugal. [Google Scholar]

- McVay SE (2006). Earnings management using classification shifting: An examination of core earnings and special items. The Accounting Review, 81(3): 501-531. https://doi.org/10.2308/accr.2006.81.3.501 [Google Scholar]

- Montenegro TM and Rodrigues LL (2020). Determinants of the attitudes of Portuguese accounting students and professionals towards earnings management. Journal of Academic Ethics, 18(3): 301-332. https://doi.org/10.1007/s10805-020-09376-z [Google Scholar]

- Mulford CW and Comiskey EE (2005). The financial numbers game: Detecting creative accounting practices. John Wiley and Sons, Hoboken, USA. [Google Scholar]

- Muttakin MB, Khan A, and Mihret DG (2018). The effect of board capital and CEO power on corporate social responsibility disclosures. Journal of Business Ethics, 150(1): 41-56. https://doi.org/10.1007/s10551-016-3105-y [Google Scholar]

- Nogueira V and Fari MA (2007). Perfil do profissional contábil: Relações entre formação e atuação no mercado de Trabalho. Perspectivas Contemporâneas, 2(1): 117-131. [Google Scholar]

- Omurgonulsen M and Omurgonulsen U (2009). Critical thinking about creative accounting in the face of a recent scandal in the Turkish banking sector. Critical Perspectives on Accounting, 20(5): 651-673. https://doi.org/10.1016/j.cpa.2007.12.006 [Google Scholar]

- Parada FM and Sanhueza RH (2009). Contabilidad creativa en Chile. Una percepción de estudiantes y profesionistas. Contaduría y Administración, 229: 85-103. [Google Scholar]

- Paseková M, Kramná E, Svitáková B, and Dolejšová M (2019). Relationship between legislation and accounting errors from the point of view of business representatives in the Czech Republic. Oeconomia Copernicana, 10(1): 193–210. https://doi.org/10.24136/oc.2019.010 [Google Scholar]

- Paterson S (2016). The paradox of alignment: Agency problems and debt restructuring. European Business Organization Law Review, 17(4): 497-521. https://doi.org/10.1007/s40804-016-0056-9 [Google Scholar]

- Pinto I and Picoto WN (2018). Earnings and capital management in European banks–Combining a multivariate regression with a qualitative comparative analysis. Journal of Business Research, 89: 258-264. https://doi.org/10.1016/j.jbusres.2017.12.034 [Google Scholar]

- Popescu LM and Ashrafzadeh I (2013). Detecting creative accounting practices and their impact on the quality of information presented in financial statements. Journal of Knowledge Management, Economics and Information Technology, 3(6): 1-13. [Google Scholar]

- Reeb DM and Zhao W (2013). Director capital and corporate disclosure quality. Journal of Accounting and Public Policy, 32(4): 191-212. https://doi.org/10.1016/j.jaccpubpol.2012.11.003 [Google Scholar]

- Remenarić B, Kenfelja I, and Mijoč I (2018). Creative accounting-Motives, techniques and possibilities of prevention. Ekonomski Vjesnik, 31(1): 193-199. [Google Scholar]

- Rhoades DL, Rechner PL, and Sundaramurthy C (2001). A meta‐analysis of board leadership structure and financial performance: Are “two heads better than one”? Corporate Governance: An International Review, 9(4): 311-319. https://doi.org/10.1111/1467-8683.00258 [Google Scholar]

- Salome EN, Ifeanyi OM, Ezemoyih CM, and Echezonachi OE (2012). The effect of creative accounting on the job performance of accountants (Auditors) in reporting financial statement in Nigeria. Kuwait Chapter of the Arabian Journal of Business and Management Review, 1(9): 1-30. [Google Scholar]

- Santos A and Grateron I (2003). Contabilidade criativa e responsabilidade dos auditores. Revista Contabilidade and Finanças, 14(32): 7-22. https://doi.org/10.1590/S1519-70772003000200001 [Google Scholar]

- Saona P, Muro L, San Martín P, and Baier-Fuentes H (2019). Board of director’s gender diversity and its impact on earnings management: An empirical analysis for selected European firms. Technological and Economic Development of Economy, 25 (4): 634-663. https://doi.org/10.3846/tede.2019.9381 [Google Scholar]

- Sen DK and Inanga EL (2005). Creative accounting in Bangladesh and global perspectives. In the Proceedings of the Partners' Conference 2005 of the Maastricht School of Management, Maastricht, The Netherlands: 75-87. [Google Scholar]

- Serrano-Cinca C, Gutiérrez-Nieto B, and Bernate-Valbuena M (2019). The use of accounting anomalies indicators to predict business failure. European Management Journal, 37(3): 353-375. https://doi.org/10.1016/j.emj.2018.10.006 [Google Scholar]

- Shah AK (1998). Exploring the influences and constraints on creative accounting in the United Kingdom. European Accounting Review, 7(1): 83-104. https://doi.org/10.1080/096381898336592 [Google Scholar]

- Shahid M (2016). Influence of creative accounting on reliability and objectivity of financial reporting (factors responsible for adoption of creative accounting practices in Pakistan). Journal of Accounting and Finance in Emerging Economies, 2(2): 75-82. https://doi.org/10.26710/jafee.v2i2.41 [Google Scholar]

- Silva RM and Santos GC (2016). Window dressing: Breach outcomes under rules and principles accounting standards or accounting fraud? An analysis of the biggest fraud worldwide. Revista de Auditoria, Governança e Contabilidade, 4(13): 144–161. [Google Scholar]

- Simsek Z, Jansen JJ, Minichilli A, and Escriba‐Esteve A (2015). Strategic leadership and leaders in entrepreneurial contexts: A nexus for innovation and impact missed? Journal of Management Studies, 52(4): 463-478. https://doi.org/10.1111/joms.12134 [Google Scholar]

- Smith T (1992). Accounting for growth: Stripping the camouflage from company accounts. Century Business, London, UK. [Google Scholar]

- Stewart R (1991). Chairmen and chief executives: An exploration of their relationship. Journal of Management Studies, 28(5): 511-528. https://doi.org/10.1111/j.1467-6486.1991.tb00766.x [Google Scholar]

- Stolowy H and Breton G (2004). Accounts manipulation: A literature review and proposed conceptual framework. Review of Accounting and Finance, 3(1): 5-92. https://doi.org/10.1108/eb043395 [Google Scholar]

- Tassadaq F and Malik QA (2015). Creative accounting and financial reporting: Model development and empirical testing. International Journal of Economics and Financial Issues, 5(2): 544-551. [Google Scholar]

- Triki A, Cook GL, and Bay D (2017). Machiavellianism, moral orientation, social desirability response bias, and anti-intellectualism: A profile of Canadian accountants. Journal of Business Ethics, 144(3): 623-635. https://doi.org/10.1007/s10551-015-2826-7 [Google Scholar]

- Vladu AB and Matis D (2010). Corporate governance and creative accounting: two concepts strongly connected? Some interesting insights highlighted by constructing the internal history of a literature. Annales Universitatis Apulensis: Series Oeconomica, 12(1): 332-346. https://doi.org/10.29302/oeconomica.2010.12.1.33 [Google Scholar]

- Watts RL (2003). Conservatism in accounting part I: Explanations and implications. Accounting Horizons, 17(3): 207-221. https://doi.org/10.2308/acch.2003.17.3.207 [Google Scholar]

- Waymire GB (2014). Neuroscience and ultimate causation in accounting research. The Accounting Review, 89(6): 2011-2019. https://doi.org/10.2308/accr-50881 [Google Scholar]

- Weisbach MS (1988). Outside directors and CEO turnover. Journal of Financial Economics, 20: 431-460. https://doi.org/10.1016/0304-405X(88)90053-0 [Google Scholar]

- Xie B, Davidson III WN, and DaDalt PJ (2003). Earnings management and corporate governance: The role of the board and the audit committee. Journal of Corporate Finance, 9(3): 295-316. https://doi.org/10.1016/S0929-1199(02)00006-8 [Google Scholar]

- Yadav B (2014). Creative accounting: An empirical study from professional prospective. International Journal of Management and Social Sciences Research, 3(1): 38-53. [Google Scholar]