International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 8, Issue 10 (October 2021), Pages: 151-160

----------------------------------------------

Original Research Paper

Title: Impact of the ownership structure on the diversification strategy

Author(s): Marouan Kouki *

Affiliation(s):

Faculty of Computing and IT, Northern Border University, Arar, Saudi Arabia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-5699-0910

Corresponding author's ORCID profile: https://orcid.org/0000-0001-5699-0910

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2021.10.015

Abstract:

This study examines the ownership characteristics that influence the decision to diversify. The Logit model was used to show that ownership structure influences the probability of diversification. Empirical tests show that the presence of the first large shareholder increases the probability of diversification during the financial crisis period. This behavior is observed for the coalition of second and third shareholders only for periods during and after the crisis. The average level of probability for firms to be diversified is between 20% and 50%. Furthermore, results show that industrial firms and more willing to be diversified than firms in the financial sector.

© 2021 The Authors. Published by IASE.

This is an

Keywords: Ownership structure, Blockholders, Diversification, Logit, Herfindahl, Entropy

Article History: Received 16 June 2020, Received in revised form 4 September 2021, Accepted 20 August 2021

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Kouki M (2021). Impact of the ownership structure on the diversification strategy. International Journal of Advanced and Applied Sciences, 8(10): 151-160

Figures

No Figure

Tables

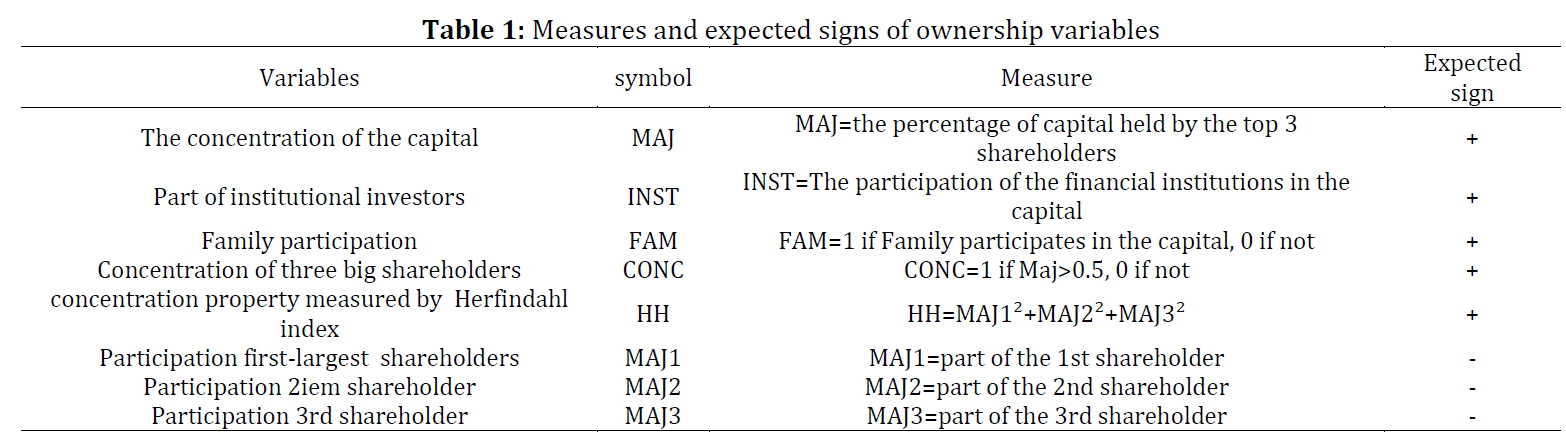

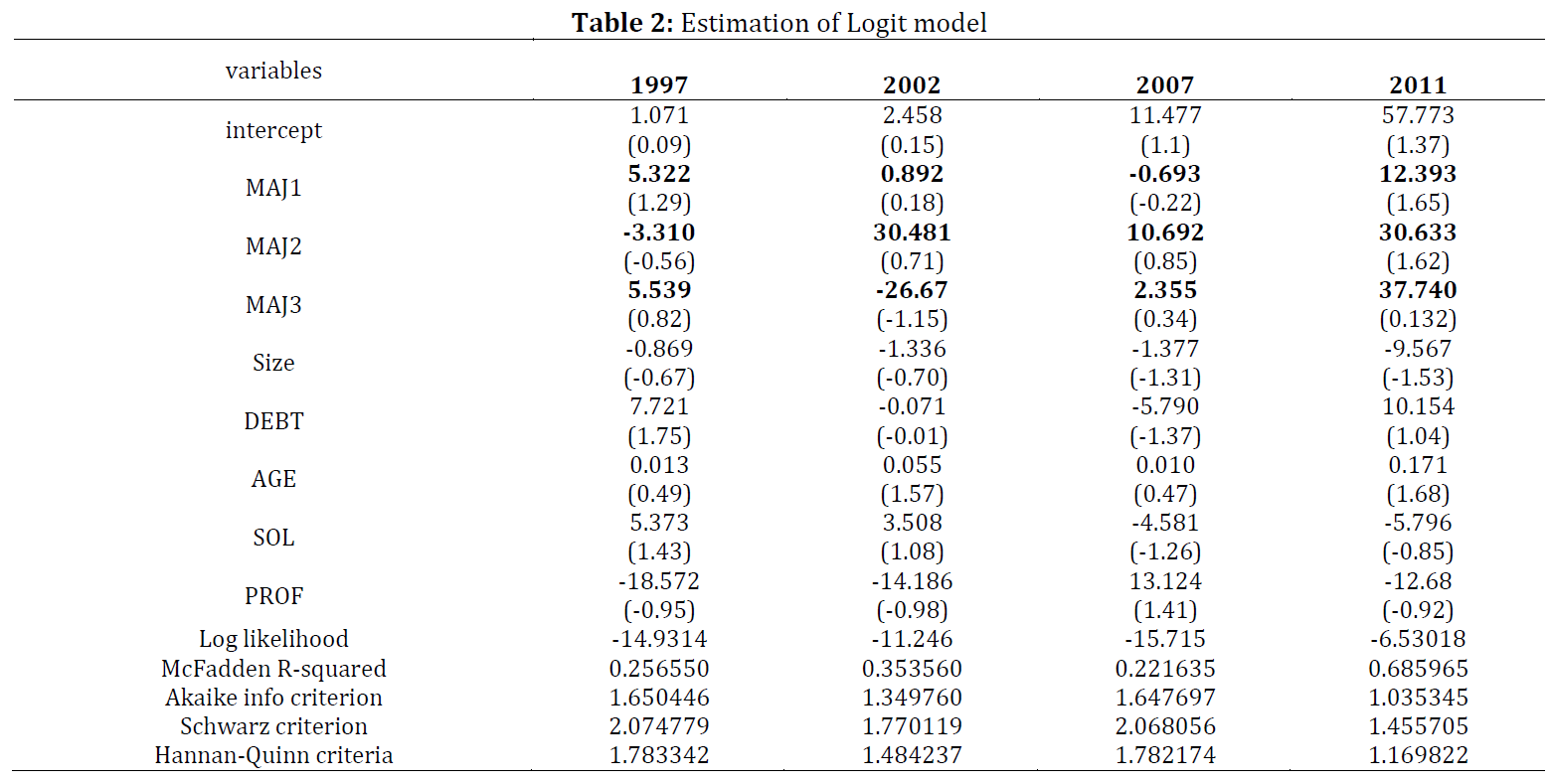

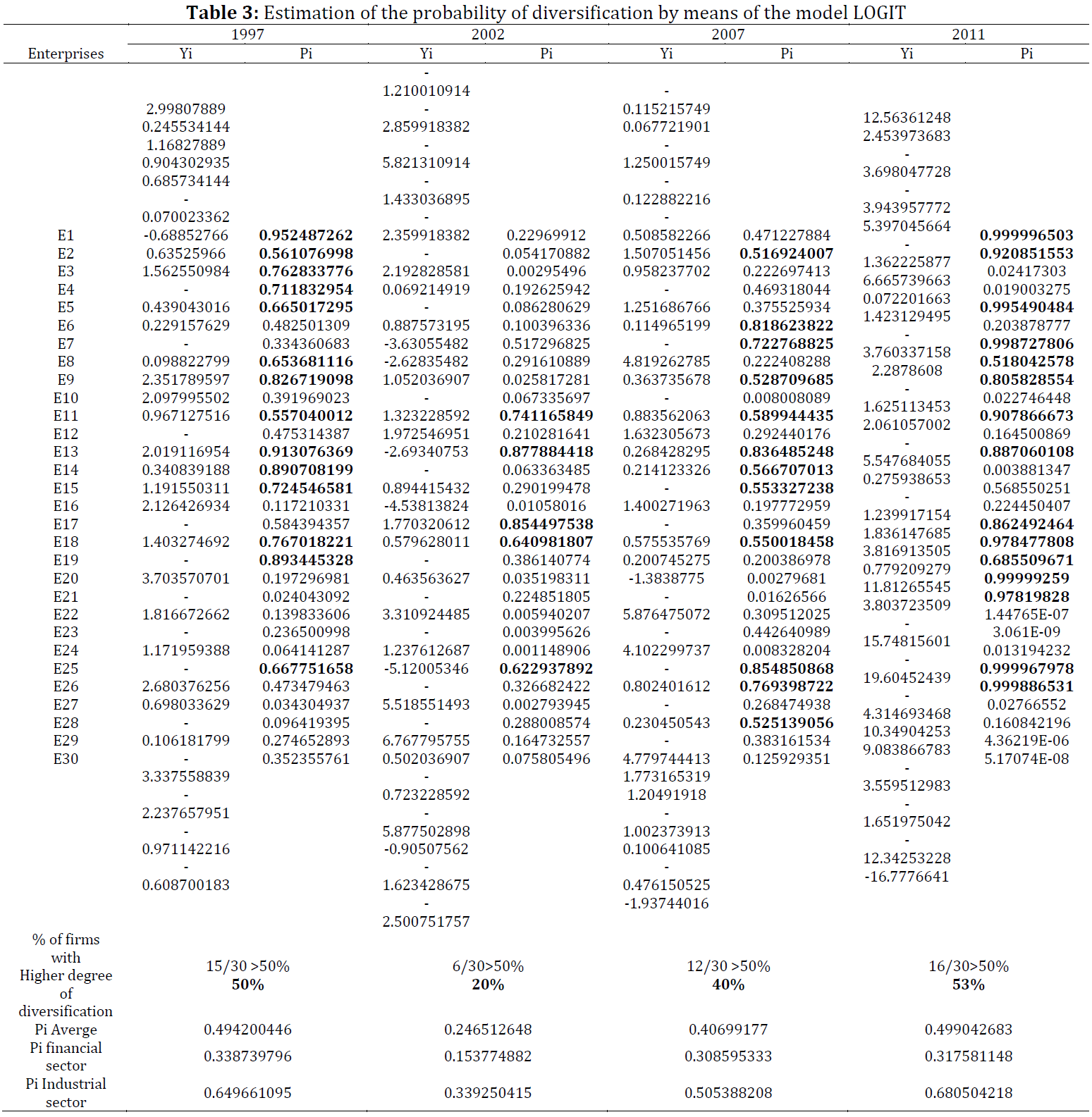

Table 1 Table 2 Table 3 Table 4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (62)

- Aivazian V, Booth L, and Cleary S (2001). Do firms in emerging markets follow different dividend policies from those in the US: Evidence from firms in eight emerging countries. Journal of Financial Research, 26(3): 175-188. https://doi.org/10.1111/1475-6803.00064 [Google Scholar]

- Amihud Y and Lev B (1981). Risk reduction as a managerial motive for conglomerate mergers. The Bell Journal of Economics, 12: 605-617. https://doi.org/10.2307/3003575 [Google Scholar]

- Amihud Y and Lev B (1999). Does corporate ownership structure affect its strategy towards diversification? Strategic Management Journal, 20(11): 1063-1069. https://doi.org/10.1002/(SICI)1097-0266(199911)20:11<1063::AID-SMJ69>3.0.CO;2-S [Google Scholar]

- Anderson RC and Reeb DM (2003). Founding‐family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance, 58(3): 1301-1328. https://doi.org/10.1111/1540-6261.00567 [Google Scholar]

- Barney J (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1): 99-120. https://doi.org/10.1177/014920639101700108 [Google Scholar]

- Batsch L (1993). La diversité des activités des groupes industriels-Une approche empirique du recentrage. Revue d'économie Industrielle, 66(1): 33-50. https://doi.org/10.3406/rei.1993.1495 [Google Scholar]

- Bennedsen M and Wolfenzon D (2000). The balance of power in closely held corporations. Journal of Financial Economics, 58(1-2): 113-139. https://doi.org/10.1016/S0304-405X(00)00068-4 [Google Scholar]

- Berger PG and Ofek E (1995). Diversification's effect on firm value. Journal of Financial Economics, 37(1): 39-65. https://doi.org/10.1016/0304-405X(94)00798-6 [Google Scholar]

- Berger PG and Ofek E (1996). Bustup takeovers of value‐destroying diversified firms. The Journal of Finance, 51(4): 1175-1200. https://doi.org/10.1111/j.1540-6261.1996.tb04066.x [Google Scholar]

- Berry CH (1975). Corporate growth and diversification. Princeton University Press, Princeton, USA. https://doi.org/10.1515/9781400872961 [Google Scholar]

- Bettis RA (1981). Performance differences in related and unrelated diversified firms. Strategic Management Journal, 2(4): 379-393. https://doi.org/10.1002/smj.4250020406 [Google Scholar]

- Burkart M, Gromb D, and Panunzi F (1998). Why higher takeover premia protect minority shareholders. Journal of Political Economy, 106(1): 172-204. https://doi.org/10.1086/250006 [Google Scholar]

- Campa JM and Kedia S (2002). Explaining the diversification discount. The Journal of Finance, 57(4): 1731-1762. https://doi.org/10.1111/1540-6261.00476 [Google Scholar]

- Chen HL and Hsu WT (2009). Family ownership, board independence, and R&D investment. Family Business Review, 22(4): 347-362. https://doi.org/10.1177/0894486509341062 [Google Scholar]

- Chen SS and Ho KW (2000). Corporate diversification, ownership structure, and firm value: The Singapore evidence. International Review of Financial Analysis, 9(3): 315-326. https://doi.org/10.1016/S1057-5219(00)00032-6 [Google Scholar]

- Cho MH (1998). Ownership structure, investment, and the corporate value: An empirical analysis. Journal of Financial Economics, 47(1): 103-121. https://doi.org/10.1016/S0304-405X(97)00039-1 [Google Scholar]

- Claessens S, Djankov S, and Lang LH (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58(1-2): 81-112. https://doi.org/10.1596/0-8213-4631-8 [Google Scholar]

- Collin SO and Bengtsson L (2000). Corporate governance and strategy: A test of the association between governance structures and diversification on Swedish data. Corporate Governance: An International Review, 8(2): 154-165. https://doi.org/10.1111/1467-8683.00192 [Google Scholar]

- Comment R and Jarrell GA (1995). Corporate focus and stock returns. Journal of Financial Economics, 37(1): 67-87. https://doi.org/10.1016/0304-405X(94)00777-X [Google Scholar]

- Davis JA, Hampton MM, and Lansberg I (1997). Generation to generation: Life cycles of the family business. Harvard Business Press, Boston, USA. [Google Scholar]

- Delios A and Beamish PW (1999). Geographic scope, product diversification, and the corporate performance of Japanese firms. Strategic Management Journal, 20(8): 711-727. https://doi.org/10.1002/(SICI)1097-0266(199908)20:8<711::AID-SMJ41>3.0.CO;2-8 [Google Scholar]

- Delios A and Wu ZJ (2005). Legal person ownership, diversification strategy and firm profitability in China. Journal of Management and Governance, 9(2): 151-169. https://doi.org/10.1007/s10997-005-4034-9 [Google Scholar]

- Delios A, Xu D, and Beamish PW (2008a). Within-country product diversification and foreign subsidiary performance. Journal of International Business Studies, 39(4): 706-724. https://doi.org/10.1057/palgrave.jibs.8400378 [Google Scholar]

- Delios A, Zhou N, and Xu WW (2008b). Ownership structure and the diversification and performance of publicly-listed companies in China. Business Horizons, 51(6): 473-483. https://doi.org/10.1016/j.bushor.2008.06.004 [Google Scholar]

- Demsetz H and Villalonga B (2001). Ownership structure and corporate performance. Journal of Corporate Finance, 7(3): 209-233. https://doi.org/10.1016/S0929-1199(01)00020-7 [Google Scholar]

- Denis DJ, Denis DK, and Sarin A (1997). Agency problems, equity ownership, and corporate diversification. The Journal of Finance, 52(1): 135-160. https://doi.org/10.1111/j.1540-6261.1997.tb03811.x [Google Scholar]

- Denis DJ, Denis DK, and Sarin A (1999). Agency theory and the influence of equity ownership structure on corporate diversification strategies. Strategic Management Journal, 20(11): 1071-1076. https://doi.org/10.1002/(SICI)1097-0266(199911)20:11<1071::AID-SMJ70>3.0.CO;2-G [Google Scholar]

- Denis DJ, Denis DK, and Yost K (2002). Global diversification, industrial diversification, and firm value. The journal of Finance, 57(5): 1951-1979. https://doi.org/10.1111/0022-1082.00485 [Google Scholar]

- Fauver L, Houston J, and Naranjo A (2003). Capital market development, international integration, legal systems, and the value of corporate diversification: A cross-country analysis. Journal of Financial and Quantitative Analysis, 38: 135-157. https://doi.org/10.2307/4126767 [Google Scholar]

- Gomes FJ (2005). Portfolio choice and trading volume with loss‐averse investors. The Journal of Business, 78(2): 675-706. https://doi.org/10.1086/427643 [Google Scholar]

- Gomez‐Mejia LR, Makri M, and Kintana ML (2010). Diversification decisions in family‐controlled firms. Journal of Management Studies, 47(2): 223-252. https://doi.org/10.1111/j.1467-6486.2009.00889.x [Google Scholar]

- Goranova M, Alessandri TM, Brandes P, and Dharwadkar R (2007). Managerial ownership and corporate diversification: A longitudinal view. Strategic Management Journal, 28(3): 211-225. https://doi.org/10.1002/smj.570 [Google Scholar]

- Grant RM, Jammine AP, and Thomas H (1988). Diversity, diversification, and profitability among British manufacturing companies, 1972–1984. Academy of Management Journal, 31(4): 771-801. https://doi.org/10.5465/256338 [Google Scholar]

- Grossman SJ and Hart OD (1986). The costs and benefits of ownership: A theory of vertical and lateral integration. Journal of Political Economy, 94(4): 691-719. https://doi.org/10.1086/261404 [Google Scholar]

- Harris M, Kriebel CH, and Raviv A (1982). Asymmetric information, incentives and intrafirm resource allocation. Management Science, 28(6): 604-620. https://doi.org/10.1287/mnsc.28.6.604 [Google Scholar]

- Kang JK and Stulz RM (1996). How different is Japanese corporate finance? An investigation of the information content of new security issues. The Review of Financial Studies, 9(1): 109-139. https://doi.org/10.1093/rfs/9.1.109 [Google Scholar]

- Kaserer C and Moldenhauer B (2008). Insider ownership and corporate performance: Evidence from Germany. Review of Managerial Science, 2(1): 1-35. https://doi.org/10.1007/s11846-007-0009-3 [Google Scholar]

- Khanna T and Palepu K (1999). Emerging market business groups, foreign investors, and corporate governance. National Bureau of Economic Research Working Paper #6955. https://doi.org/10.3386/w6955 [Google Scholar]

- Khanna T and Palepu K (2000). Is group affiliation profitable in emerging markets? An analysis of diversified Indian business groups. The Journal of Finance, 55(2): 867-891. https://doi.org/10.1111/0022-1082.00229 [Google Scholar]

- Kochhar R and Hitt MA (1998). Linking corporate strategy to capital structure: Diversification strategy, type and source of financing. Strategic Management Journal, 19(6): 601-610. https://doi.org/10.1002/(SICI)1097-0266(199806)19:6<601::AID-SMJ961>3.0.CO;2-M [Google Scholar]

- Lane PJ, Cannella AA, and Lubatkin MH (1998). Agency problems as antecedents to unrelated mergers and diversification: Amihud and Lev reconsidered. Strategic Management Journal, 19(6): 555-578. https://doi.org/10.1002/(SICI)1097-0266(199806)19:6<555::AID-SMJ955>3.0.CO;2-Y [Google Scholar]

- Lane PJ, Cannella AA, and Lubatkin MH (1999). Ownership structure and corporate strategy: One question viewed from two different worlds. Strategic Management Journal, 20(11): 1077-1086. https://doi.org/10.1002/(SICI)1097-0266(199911)20:11<1077::AID-SMJ68>3.0.CO;2-O [Google Scholar]

- Lins K and Servaes H (1999). International evidence on the value of corporate diversification. The Journal of Finance, 54(6): 2215-2239. https://doi.org/10.1111/0022-1082.00186 [Google Scholar]

- May DO (1995). Do managerial motives influence firm risk reduction strategies? The Journal of Finance, 50(4): 1291-1308. https://doi.org/10.1111/j.1540-6261.1995.tb04059.x [Google Scholar]

- Michel A and Shaked I (1984). Does business diversification affect performance? Financial Management, 13: 18-25. https://doi.org/10.2307/3665297 [Google Scholar]

- Minguez-Vera A and Martin-Ugedo JF (2007). Does ownership structure affect value? A panel data analysis for the Spanish market. International Review of Financial Analysis, 16(1): 81-98. https://doi.org/10.1016/j.irfa.2005.10.004 [Google Scholar]

- Montgomery CA (1985). Product-market diversification and market power. Academy of Management Journal, 28(4): 789-798. https://doi.org/10.2307/256237 [Google Scholar]

- Montgomery CA (1994). Corporate diversificaton. Journal of Economic Perspectives, 8(3): 163-178. https://doi.org/10.1257/jep.8.3.163 [Google Scholar]

- Mtanios R and Paquerot M (1999). Structure de propriété et sous-performance des firmes: Une étude empirique sur le marché au comptant, le règlement mensuel et le second marché. Finance Contrôle Stratégie, 2(4): 157-179. [Google Scholar]

- Ohlson JA (1980). Financial ratios and the probabilistic prediction of bankruptcy. Journal of Accounting Research, 18(1): 109-131. https://doi.org/10.2307/2490395 [Google Scholar]

- Perrow C (1986). Complex organizations: A critical essay. McGraw-Hill, New York, USA. [Google Scholar]

- Pound J (1988). Proxy contests and the efficiency of shareholder oversight. Journal of Financial Economics, 20: 237-265. https://doi.org/10.1016/0304-405X(88)90046-3 [Google Scholar]

- Prahalad CH and Hamel G (1990). The core competence of the corporation. Harvard Business Review, 68(3): 295-336. [Google Scholar]

- Ramanujam V and Varadarajan P (1989). Research on corporate diversification: A synthesis. Strategic Management Journal, 10(6): 523-551. https://doi.org/10.1002/smj.4250100603 [Google Scholar]

- Ramaswamy K, Li M, and Veliyath R (2002). Variations in ownership behavior and propensity to diversify: A study of the Indian corporate context. Strategic Management Journal, 23(4): 345-358. https://doi.org/10.1002/smj.227 [Google Scholar]

- Rumelt R (1974). Strategy, structure and economic performance. Harvard University Press, Cambridge, USA. [Google Scholar]

- Seetharaman A, Swanson ZL, and Srinidhi B (2001). Analytical and empirical evidence of the impact of tax rates on the trade-off between debt and managerial ownership. Journal of Accounting, Auditing & Finance, 16(3): 249-272. https://doi.org/10.1177/0148558X0101600306 [Google Scholar]

- Shleifer A and Vishny RW (1986). Large shareholders and corporate control. Journal of Political Economy, 94(3, Part 1): 461-488. https://doi.org/10.1086/261385 [Google Scholar]

- Shleifer A and Vishny RW (1989). Management entrenchment: The case of manager-specific investments. Journal of Financial Economics, 25(1): 123-139. https://doi.org/10.1016/0304-405X(89)90099-8 [Google Scholar]

- Shleifer A and Vishny RW (1997). A survey of corporate governance. The Journal of Finance, 52(2): 737-783. https://doi.org/10.1111/j.1540-6261.1997.tb04820.x [Google Scholar]

- Shumway T (2001). Forecasting bankruptcy more accurately: A simple hazard model. The Journal of Business, 74(1): 101-124. https://doi.org/10.1086/209665 [Google Scholar]

- Thomsen S and Pedersen T (2000). Effects of international diversity and product diversity on the performance of multinational firms. Strategic Management Journal, 21(6): 689-705. https://doi.org/10.1002/(SICI)1097-0266(200006)21:6<689::AID-SMJ115>3.0.CO;2-Y [Google Scholar]