International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 8, Issue 10 (October 2021), Pages: 59-76

----------------------------------------------

Original Research Paper

Title: Equity home bias and consumption-real exchange rate puzzles: A joint solution

Author(s): Dao Hoang Tuan *

Affiliation(s):

Academy of Policy and Development (APD), International School of Economics and Finance, Hanoi, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-5785-3843

Corresponding author's ORCID profile: https://orcid.org/0000-0002-5785-3843

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2021.10.008

Abstract:

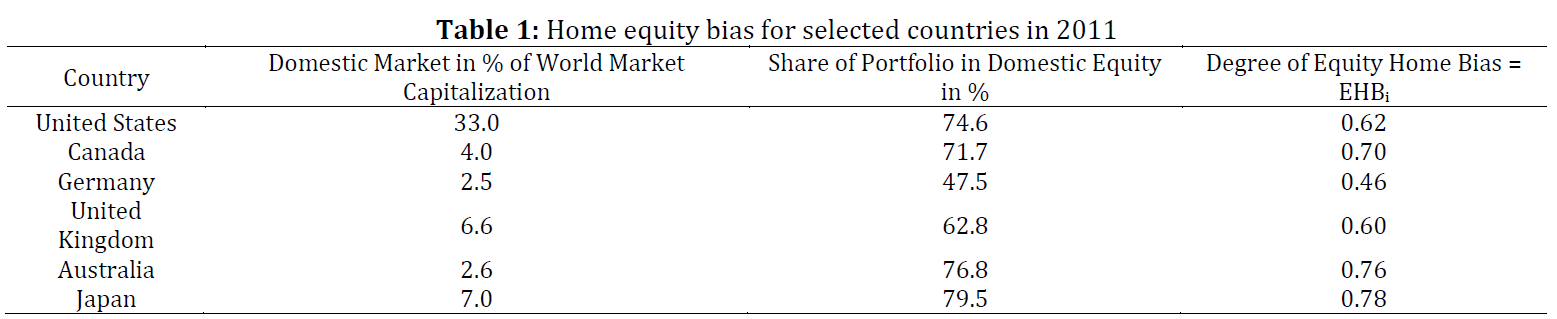

In a standard dynamic stochastic general equilibrium model with a complete asset market, home agents should hold a foreign equity biased portfolio to hedge the non-traded labor income risk, which contradicts home equity biased portfolios observed worldwide. As the labor income share increases, the degree of home bias should decrease because there is more incentive to hold foreign equity. In the data, there is not any evidence that the labor income share and the degree of home bias are negatively correlated. The standard model also predicts that the consumption differential-real exchange rate correlation is positive, while it is negative in the data. I show that a combination of market incompleteness, non-tradable goods, and labor supply can explain the three features above. My model can generate a large equity home bias, despite the strong positive correlation of non-traded human capital return with domestic equity return. The home bias is not sensitive to the labor income share. The consumption differential-real exchange rate unconditional correlation generated by my model simulation is zero.

© 2021 The Authors. Published by IASE.

This is an

Keywords: International equity home-bias, Consumption-real exchange rate puzzle, Home agent

Article History: Received 19 April 2021, Received in revised form 6 July 2021, Accepted 22 July 2021

Acknowledgment

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Tuan DH (2021). Equity home bias and consumption-real exchange rate puzzles: A joint solution. International Journal of Advanced and Applied Sciences, 8(10): 59-76

Figures

Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6 Fig. 7 Fig. 8 Fig. 9 Fig. 10 Fig. 11 Fig. 12 Fig. 13 Fig. 14

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

{kind=link}

{kind=link}

----------------------------------------------

References (42)

- Ahearne AG, Griever WL, and Warnock FE (2004). Information costs and home bias: An analysis of US holdings of foreign equities. Journal of International Economics, 62(2): 313-336. https://doi.org/10.1016/S0022-1996(03)00015-1 [Google Scholar]

- Amano R and Wirjanto T (1996). Intertemporal substitution, imports and the permanent income model. Journal of International Economics, 40(3-4): 439–457. https://doi.org/10.1016/0022-1996(95)01418-7 [Google Scholar]

- Backus D and Smith G (1993). Consumption and real exchange rates in dynamic economies with non-traded goods. Journal of International Economics, 35(3-4): 297–316. https://doi.org/10.1016/0022-1996(93)90021-O [Google Scholar]

- Backus D, Kehoe P, and Kydland F (1994). Dynamics of the trade balance and the terms of trade: The j-curve? American Economic Review, 84(1): 84–103. [Google Scholar]

- Baxter M and Jermann U (1997). The international diversification puzzle is worse than you think. American Economic Review, 87(1): 170–80. [Google Scholar]

- Baxter M, Jermann U, and King R (1998). Nontraded goods, nontraded factors, and international non-diversification. Journal of International Economics, 44(2): 211–229. https://doi.org/10.1016/S0022-1996(97)00018-4 [Google Scholar]

- Benigno G and Thoenissen C (2008). Consumption and real exchange rates with incomplete markets and non-traded goods. Journal of International Money and Finance, 27(6): 926–948. https://doi.org/10.1016/j.jimonfin.2008.04.008 [Google Scholar]

- Campbell JY and Viceira LM (2002). Strategic asset allocation: Portfolio choice for long-term investors. Oxford University Press, Oxford, UK. https://doi.org/10.1093/0198296940.001.0001 [Google Scholar]

- Campbell JY, Chan YL, and Viceira L (2003). A multivariate model of strategic asset allocation. Journal of Financial Economics, 67(1): 41–80. https://doi.org/10.1016/S0304-405X(02)00231-3 [Google Scholar]

- Coeurdacier N and Rey H (2013). Home bias in open economy financial macroeconomics. Journal of Economic Literature, 51(1): 63-115. https://doi.org/10.1257/jel.51.1.63 [Google Scholar]

- Coeurdacier N, Kollmann R, and Martin P (2010). International portfolios, capital accumulation and foreign assets dynamics. Journal of International Economics, 80(1): 100-112. https://doi.org/10.1016/j.jinteco.2009.05.006 [Google Scholar]

- Coeurdacier N, Kollmann R, Martin P, Ghironi F, and Gürkaynak RS (2007). International portfolios with supply, demand, and redistributive shocks. In the NBER International Seminar on Macroeconomics, The University of Chicago Press Chicago, USA, 2007: 231-263. https://doi.org/10.3386/w13424 [Google Scholar]

- Cole HL and Obstfeld M (1991). Commodity trade and international risk sharing: How much do financial markets matter? Journal of Monetary Economics, 28(1): 3-24. https://doi.org/10.1016/0304-3932(91)90023-H [Google Scholar]

- Collard F, Dellas H, Diba B, and Stockman A (2007). Goods trade and international equity portfolios. Working Paper Series No. w13612, National Bureau of Economic Research, Cambridge, USA. https://doi.org/10.3386/w13612 [Google Scholar]

- Corsetti G, Dedola L and Leduc S (2008). International risk sharing and the transmission of productivity shocks. Review of Economic Studies, 75(2): 443–473. https://doi.org/10.1111/j.1467-937X.2008.00475.x [Google Scholar]

- Denis C and Huizinga H (2004). Are foreign ownership and good institutions substitutes? The case of non-traded equity. The Case of Non-Traded Equity (April 2004). Available online at: https://ssrn.com/abstract=541043 [Google Scholar]

- Devereux M and Sutherland A (2010). Valuation effects and the dynamics of net external assets. Journal of International Economics, 80(1): 129–143. https://doi.org/10.1016/j.jinteco.2009.06.001 [Google Scholar]

- Devereux M and Sutherland A (2011). Country portfolios in open economy macro models. Journal of the European Economic Association, 9(2): 337–369. https://doi.org/10.1111/j.1542-4774.2010.01010.x [Google Scholar]

- Engel C and Matsumoto A (2009). The international diversification puzzle when goods prices are sticky: It’s really about exchange-rate hedging, not equity portfolios. American Economic Journal: Macroeconomics, 1(2): 155–88. https://doi.org/10.1257/mac.1.2.155 [Google Scholar]

- Evans M and Hnatkovska V (2012). A method for solving general equilibrium models with incomplete markets and many financial assets. Journal of Economic Dynamics and Control, 36(12): 1909–1930. https://doi.org/10.1016/j.jedc.2012.05.010 [Google Scholar]

- Feng L (2013). Taste shocks, endogenous labor supply, and equity home bias. Macroeconomic Dynamics, 25(5): 1-22. [Google Scholar]

- Fitzgerald D (2012). Trade costs, asset market frictions, and risk sharing. American Economic Review, 102(6): 2700–2733. https://doi.org/10.1257/aer.102.6.2700 [Google Scholar]

- Ghironi F, Lee J, and Rebucci A (2009). The valuation channel of external adjustment. Boston College, Boston, USA. https://doi.org/10.2139/ssrn.1559369 [Google Scholar]

- Heathcote J and Perri F (2013). The international diversification puzzle is not as bad as you think. Journal of Political Economy, 121(6): 1108-1159. https://doi.org/10.1086/674143 [Google Scholar]

- Hnatkovska V (2010). Home bias and high turnover: Dynamic portfolio choice with incomplete markets. Journal of International Economics, 80(1): 113–128. https://doi.org/10.1016/j.jinteco.2009.06.006 [Google Scholar]

- Ireland PN (2001). Sticky-price models of the business cycle: Specification and stability. Journal of Monetary Economics, 47(1): 3-18. https://doi.org/10.1016/S0304-3932(00)00047-7 [Google Scholar]

- Kang J and Stulz R (1997). Why is there a home bias? An analysis of foreign portfolio equity ownership in Japan. Journal of Financial Economics, 46(1): 3–28. https://doi.org/10.1016/S0304-405X(97)00023-8 [Google Scholar]

- King R and Rebelo S (1999). Resuscitating real business cycles. In: Taylor JB, Woodford M, and Uhlig H (Eds.), Handbook of macroeconomics: 927–1007. Volume 1, Elsevier, Amsterdam, Netherlands. https://doi.org/10.1016/S1574-0048(99)10022-3 [Google Scholar]

- Lai H and Trefler D (2002). The gains from trade with monopolistic competition: Specification, estimation, and misspecification. Working Paper No. w9169, National Bureau of Economic Research, Cambridge, USA. https://doi.org/10.3386/w9169 [Google Scholar]

- Mankiw N, Rotemberg J, and Summers L (1985). Intertemporal substitution in macroeconomics. The Quarterly Journal of Economics, 100(1): 225–251. https://doi.org/10.2307/1885743 [Google Scholar]

- Matsumoto A (2007). The role of non-separable utility and non-tradeables in international business cycle and portfolio choice. IMF Working Papers 07/163, International Monetary Fund. https://doi.org/10.5089/9781451867275.001 [Google Scholar]

- Obstfeld M (2007). International risk sharing and the costs of trade. Ohlin Lectures, Stockholm School of Economics, Stockholm, Sweden. [Google Scholar]

- Obstfeld M and Rogoff K (1998). Risk and exchange rates. NBER Working Paper 6694, Bureau of Economic Research Inc., Cambridge, USA. https://doi.org/10.3386/w6694 [Google Scholar]

- Obstfeld M, Rogoff KS, and Rogoff K (1996). Foundations of international macroeconomics. MIT Press, Cambridge, USA. [Google Scholar]

- Pesenti P and Wincoop EV (2002). Can non-tradables generate substantial home bias? Journal of Money, Credit and Banking, 34: 25–50. https://doi.org/10.1353/mcb.2002.0034 [Google Scholar]

- Ravn M and Uhlig H (2002). On adjusting the Hodrick-Prescott filter for the frequency of observations. Review of Economics and Statistics, 84(2): 371–376. https://doi.org/10.1162/003465302317411604 [Google Scholar]

- Schmitt-Grohe S and Uribe M (2003). Closing small open economy models. Journal of International Economics, 61(1): 163–185. https://doi.org/10.1016/S0022-1996(02)00056-9 [Google Scholar]

- Sercu P and VanpÈe R (2007). Home bias in international equity portfolios: A review. Working Paper, Leuven School of Business and Economics. https://doi.org/10.2139/ssrn.1025806 [Google Scholar]

- Stockman A and Tesar L (1995). Tastes and technology in a two-country model of the business cycle: Explaining international comovements. American Economic Association, 85(1): 168–185. [Google Scholar]

- Tesar L (1993). International risk-sharing and non-traded goods. Journal of International Economics, 35(1-2): 69–89. https://doi.org/10.1016/0022-1996(93)90005-I [Google Scholar]

- Tille C and Wincoop EV (2010). International capital flows. Journal of International Economics, 80(2): 157–175. https://doi.org/10.1016/j.jinteco.2009.11.003 [Google Scholar]

- Viceira L (2001). Optimal portfolio choice for long-horizon investors with non-tradable labor income. Journal of Finance, 56(2): 433–470. https://doi.org/10.1111/0022-1082.00333 [Google Scholar]