International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 8, Issue 1 (January 2021), Pages: 75-81

----------------------------------------------

Original Research Paper

Title: Effect of risk of using computerized AIS on external auditor's work quality in Yemen

Author(s): Hamood Mohd. Al-Hattami 1, Abdulwahid Ahmed Hashed 2, *, Khaled M. E. Alnuzaili 3, Maged A. Z. Alsoufi 3, Alwan A. Alnakeeb 3, Hussein Rageh 3

Affiliation(s):

1Department of Accounting, Hodeidah University, Al Hudaydah, Yemen

2Department of Accounting, Prince Sattam Bin Abdulaziz University, Al-Kharj, Saudi Arabia

3Department of Commerce, Dr. Babasaheb Ambedkar Marathwada University, Aurangabad, India

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0002-6791-235X

Corresponding author's ORCID profile: https://orcid.org/0000-0002-6791-235X

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2021.01.010

Abstract:

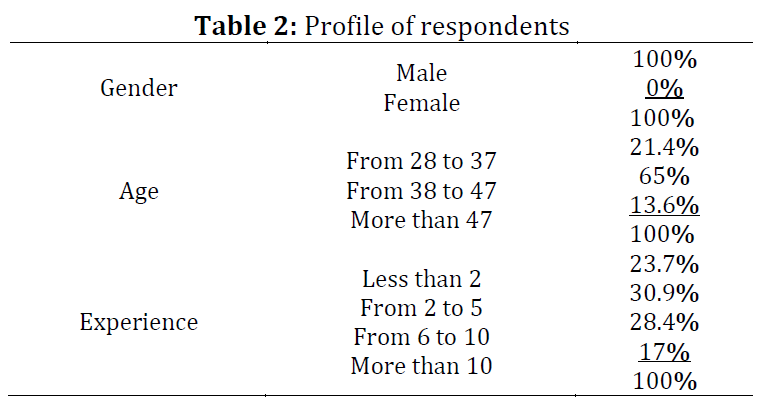

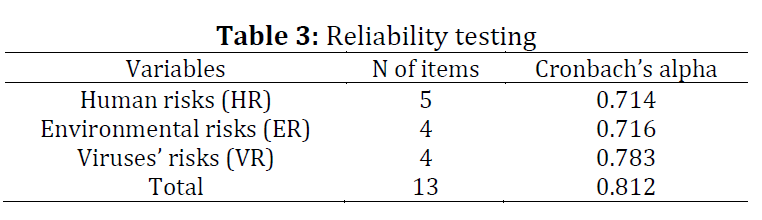

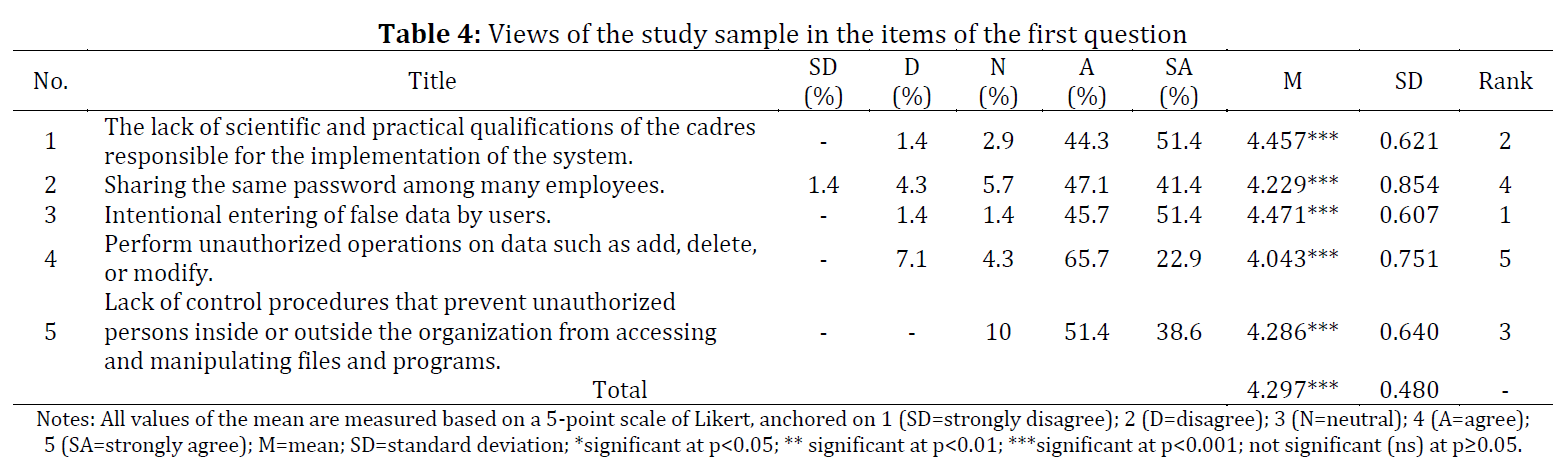

This study aimed to identify the effect of the risks of using computerized AIS in facilities subject to auditing on external auditor's work quality. The study was applied to Yemeni external auditors, with a targeted sample size of 120 people who were randomly selected. Data were collected through questionnaires. The collected data were processed using SPSS version 23. The results of this study revealed a statistically significant effect of risk associated with the use of computerized AIS (human risks, environmental risks, and viruses’ risks) on external auditor's work quality. However, human risks are the most risk to the external auditor in the audited facilities. From a practical standpoint, AIS and IT auditors and facilities subject to auditing all stand to gain from the results of this study.

© 2020 The Authors. Published by IASE.

This is an

Keywords: Risk, Accounting information system (AIS), Computerized AIS, External auditor's work quality, Yemen

Article History: Received 24 June 2020, Received in revised form 1 September 2020, Accepted 1 September 2020

Acknowledgment:

This publication was supported by the Deanship of Scientific Research, Prince Sattam Bin Abdulaziz University, Alkharj, Saudi Arabia.

Compliance with ethical standards

Conflict of interest: The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Citation:

Al-Hattami HM, Hashed AA, and Alnuzaili KME et al. (2021). Effect of risk of using computerized AIS on external auditor's work quality in Yemen. International Journal of Advanced and Applied Sciences, 8(1): 75-81

Figures

{kind=link}

Tables

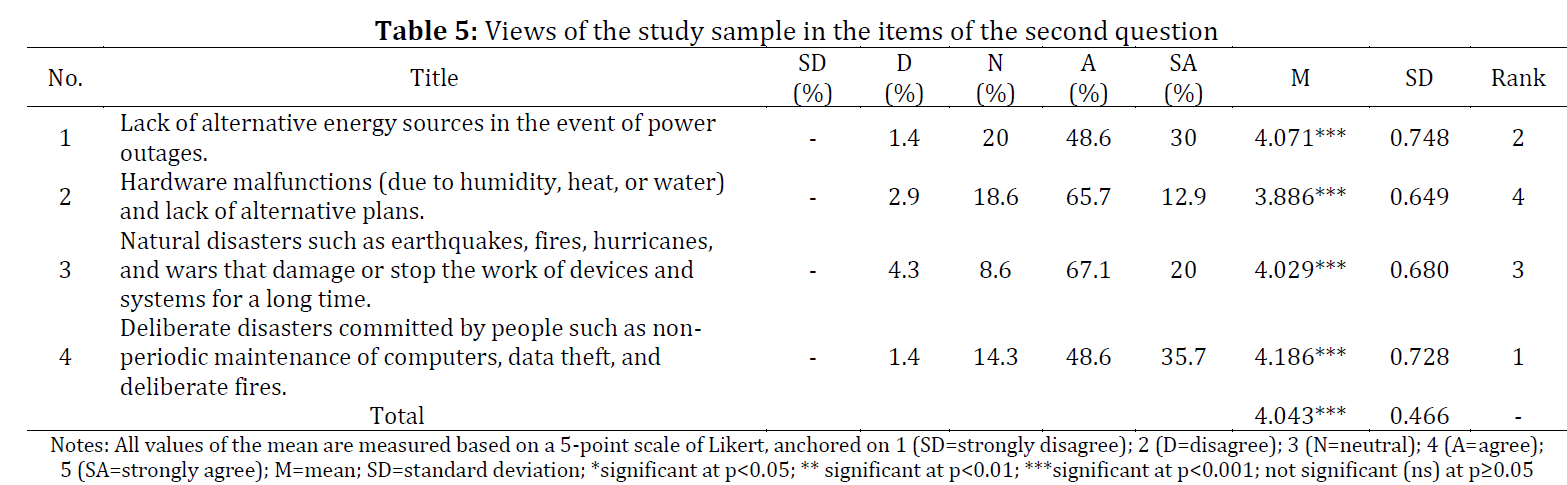

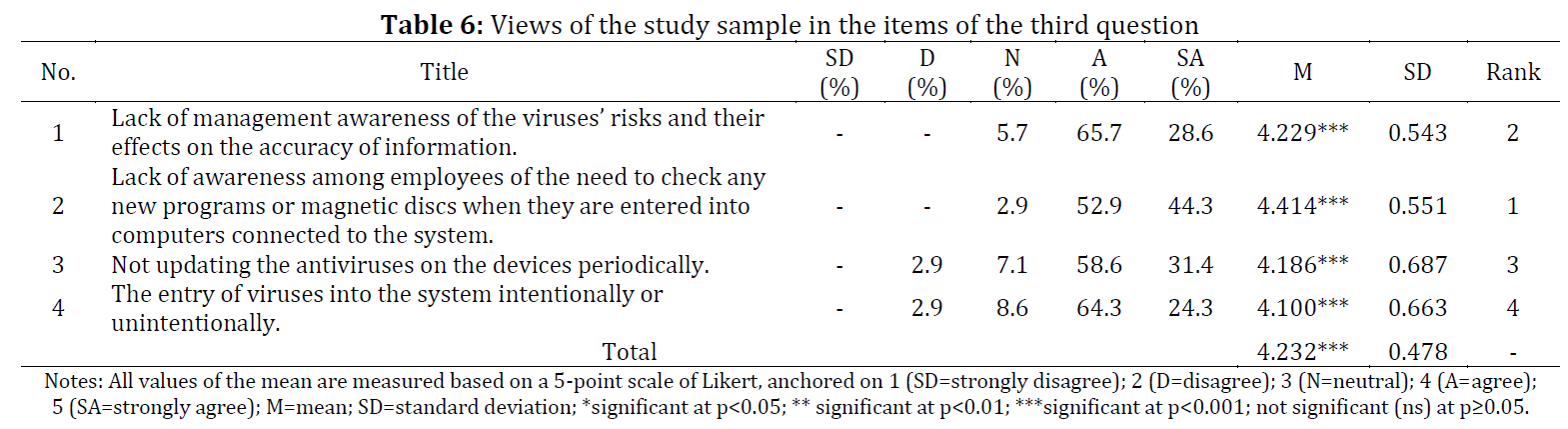

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (42)

- Adow AHE (2020). Contemporary trends in external auditing and its role in reducing audit risks-A field study of external auditing offices in Sudan. International Journal of Advanced and Applied Sciences, 7(7): 119-125. https://doi.org/10.21833/ijaas.2020.07.015 [Google Scholar]

- Al-Ansi AA and Ismail NAB, and Al-Swidi AK (2013). The effect of IT knowledge and IT training on the IT utilisation among external auditors: Evidence from Yemen. Asian Social Science, 9(10): 307-323. https://doi.org/10.5539/ass.v9n10p307 [Google Scholar]

- Al-Hattami HM and Kabra JD (2019). The role of Accounting Information System (AIS) in rationalizing human resource related decisions: A case study of selected commercial banks in Yemen. International Journal of Management Studies, 4(2): 84-91. https://doi.org/10.18843/ijms/v6si2/12 [Google Scholar]

- Al-Hattami HM, Hashed AA, and Kabra JD (2020). Effect of AIS success on performance measures of SMEs: Evidence from Yemen. International Journal of Business Information Systems, 1(1). https://doi.org/10.1504/IJBIS.2020.10025605 [Google Scholar]

- Al-Kharbi A (2010). A study of the impact of ‘IT’ on audit and the role of auditing organizations to cope with the changing environment of the accounting systems with special reference to Republic of Yemen. Ph.D. Dissertation, Bharati Vidyapeeth Deemed University, India. [Google Scholar]

- Appiah KO, Agyemang F, Agyei YFR, Nketiah S, and Mensah BJ (2014). Computerised accounting information systems: lessons in state-owned enterprise in developing economies. Journal of Finance and Management in Public Services, 12(1): 1-23. [Google Scholar]

- Arens A and Loebbecke J (2005). Audit–An integrated approach. Arc Publishing House, Todmorden, Lancashire, UK. [Google Scholar]

- Arens AA, Beasley MS, and Elder R (2006). Auditing and assurance services: An integrated approach. Prentice-Hall, Upper Saddle River, USA. [Google Scholar]

- Azibi J (2018). Joint audit and financial scandal: The case of the French context. International Journal of Advanced and Applied Sciences, 5(7): 1-7. https://doi.org/10.21833/ijaas.2018.07.001 [Google Scholar]

- Azzam M, Alrabba H, AlQudah A, and Mansur H (2020). A study on the relationship between internal and external audits on financial reporting quality. Management Science Letters, 10(4): 937-942. [Google Scholar]

- Bagranoff NA, Simkin MG, and Norman CS (2010). Core concept accounting information systems. John Wiley and Sons, Hoboken, USA. [Google Scholar]

- Bansah EA (2018). The threats of using computerized accounting information systems in the banking industry. Journal of Accounting and Management Information Systems, 18(3): 440-461. https://doi.org/10.24818/jamis.2018.03006 [Google Scholar]

- BPPLM (2016). ACCA P7 advanced audit and assurance (UK): Study text. BPP Learning Media, London, UK.

- Chersan IC (2019). Audit quality and several of its determinants. The Audit Financial Journal, Chamber of Financial Auditors of Romania, 17(153): 1-93. [Google Scholar]

- Das S (1989). An overview of accounting as an information system. In: Flood RL, Jackson MC, and Keys P (Eds.), Systems prospects: 29-34. Springer, Boston, USA. [Google Scholar]

- Elefterie L and Badea G (2016). The impact of information technology on the audit process. Economics, Management and Financial Markets, 11(1): 303-309. [Google Scholar]

- Farouk MA and Hassan SU (2014). Impact of audit quality and financial performance of quoted cement firms in Nigeria. International Journal of Accounting and Taxation, 2(2): 1-22. [Google Scholar]

- Frias SA and Fajardo CL (2008). Textbook in auditing theory. Katha Publishing Co. Inc., Makati City, Philippines.

- Hair JF, Black WC, Babin BJ, and Anderson RE (2010). Multivariate data analysis: A global perspective. 7th Edition, Pearson Education Inc., Upper Saddle River, USA. [Google Scholar]

- Kamil A and Nashat N (2017). The impact of information technology on the auditing profession analytical study. International Review of Management and Business Research, 6(4): 1330-1342. [Google Scholar]

- Kombo B (2013). The effects of computerized accounting system on auditing process: A case study of Mtwara district council (mdc). Ph.D. Dissertation, Mzumbe University, Morogoro, Tanzania. [Google Scholar]

- Kumar R and Sharma V (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd., New Delhi, India. [Google Scholar]

- Lanier S (1992). Computerized accounting. Prentice-Hall International Limited, London, UK. [Google Scholar]

- Mathur N, Mathur H, and Pandya T (2015). Risk management in information system of organisation: A conceptual framework. International Journal of Novel Research in Computer Science and Software Engineering, 2(1): 82-88. [Google Scholar]

- Mitchell F, Reid GC, and Smith JA (2000). Information system development in the small firm: The use of management accounting. CIMA Publisher, London, UK. [Google Scholar]

- Moscove SA and Simkin MG (1984). Accounting information systems: Concepts and practice for effective decision making. John Wiley and Sons, Inc., Hoboken, USA. [Google Scholar]

- Nicolaou AI (2000). A contingency model of perceived effectiveness in accounting information systems: Organizational coordination and control effects. International Journal of Accounting Information Systems, 1(2): 91-105. [Google Scholar]

- Pedrosa I, Costa CJ, and Laureano RM (2015). Motivations and limitations on the use of information technology on statutory auditors' work: An exploratory study. In the 10th Iberian Conference on Information Systems and Technologies, IEEE, Aveiro, Portugal: 1-6. [Google Scholar]

- Pierre AK, Khalil G, Marwan K, Nivine G, and Tarek A (2013). The tendency for using Accounting Information Systems in Lebanese firms. International Journal of Computer Theory and Engineering, 5(6): 895-899. https://doi.org/10.7763/IJCTE.2013.V5.818 [Google Scholar]

- Řeháček P (2017). Risk management standards for project management. International Journal of Advanced and Applied Sciences, 4(6): 1-13. https://doi.org/10.21833/ijaas.2017.06.001 [Google Scholar]

- Sayana SA and CISA C (2003). Using CAATs to support IS audit. Information Systems Control Journal, 1: 21-23. [Google Scholar]

- Sharp JM (2010). Yemen: Background and US relations. DIANE Publishing, Darby, USA. [Google Scholar]

- Stoneburner G, Goguen A, and Feringa A (2002). Risk management guide for information technology systems. Nist Special Publication, 800(30): 800-830. https://doi.org/10.6028/NIST.SP.800-30 [Google Scholar] PMid:12516822

- Sugut OC (2014). The effect of computerized accounting systems on the quality of financial reports of non-governmental organizations in Nairobi county, Kenya. Ph.D. Dissertation, University of Nairobi, Nairobi, Kenya. [Google Scholar]

- Tarek M, Mohamed EK, Hussain MM, and Basuony MA (2017). The implication of information technology on the audit profession in developing country. International Journal of Accounting and Information Management, 25(2): 237-255. https://doi.org/10.1108/IJAIM-03-2016-0022 [Google Scholar]

- UNCTAD (2017). The least developed countries report 2017. United Nations Conference on Trade and Development, United Nations Publication, USA. [Google Scholar]

- UNY (2011). United Nations development assistance framework (UNDAF) 2012-2015. United Nations in Yemen, Sana'a, Yemen. [Google Scholar]

- WBG (2007). Assessing the financial needs of small and micro institutions in Yemen. World Bank Group Final Report No.44471-YE., World Bank Group, Washington, USA. [Google Scholar]

- Whittington OR and Pany K (2016). Principles of auditing and other assurance services. 20th Edition, McGraw-Hill Education, New York, USA. [Google Scholar]

- Wongsim M and Gao J (2011). Exploring information quality in accounting information systems adoption. IBIMA Publishing, Pennsylvania, USA. https://doi.org/10.5171/2011.683574 [Google Scholar]

- YACPA (2011). Yemeni Association of Certified Public Accountants. Available online at: http://www.yacpa.org/ar/

- Yasser S and Soliman M (2018). The effect of audit quality on earnings management in developing countries: The case of Egypt. International Research Journal of Applied Finance, 9(4): 216-231. [Google Scholar]