International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN: 2313-626X

Frequency: 12

![]()

Volume 7, Issue 12 (December 2020), Pages: 48-55

----------------------------------------------

Original Research Paper

Title: Calendar effects: Empirical evidence from the Vietnam stock markets

Author(s): Bui Huy Nhuong 1, Pham Dan Khanh 2, *, Pham Thanh Dat 3

Affiliation(s):

1Personnel Department, National Economics University, Hanoi, Vietnam

2School of Advanced Education Program, National Economics University, Hanoi, Vietnam

3School of Banking and Finance, National Economics University, Hanoi, Vietnam

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0170-8636

Corresponding author's ORCID profile: https://orcid.org/0000-0003-0170-8636

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2020.12.005

Abstract:

The Efficient Market Hypothesis (EMH) deals with informational efficiency and strongly based on the idea that the stock market prices or returns are unpredictable and do not follows any regular pattern, so it is impossible to “beat the market.” According to the EMH theory, security prices immediately and fully reflect all available relevant information. EMH also establishes a foundation of modern investment theory that essentially advocates the futility of information in the generation of abnormal returns in capital markets over a period. However, the existence of anomalies challenges the notion of efficiency in stock markets. Calendar effects break the weak form of efficiency, highlighting the role of past patterns and seasonality in estimating future prices. The present research aims to study the efficiency in Vietnam stock markets. Using daily and monthly returns of VnIndex data from its inception in March 2002 to December 2018, we employ dummy variable multiple linear regression techniques to assess the existence of calendar effects in Vietnam stock markets. To correct for volatility clustering and ARCH effect present in the daily returns, the results are modeled using the EGARCH estimation methodology. The study reveals the existence of calendar effects in Vietnam in the form of a significant Friday Effect as well as a significant “January effect,” thereby suggesting that the Vietnam stock markets do not show informational efficiency even in the weak form, a trait observable in emerging markets.

© 2020 The Authors. Published by IASE.

This is an

Keywords: Calendar effects, EMH, Dummy variable regression, Day-of-the-week effect, Month-of-the-year effect

Article History: Received 7 May 2020, Received in revised form 21 July 2020, Accepted 29 July 2020

Acknowledgment:

No Acknowledgment.

Compliance with ethical standards

Conflict of interest: The authors declare that they have no conflict of interest.

Citation:

Nhuong BH, Khanh PD, and Dat PT (2020). Calendar effects: Empirical evidence from the Vietnam stock markets. International Journal of Advanced and Applied Sciences, 7(12): 48-55

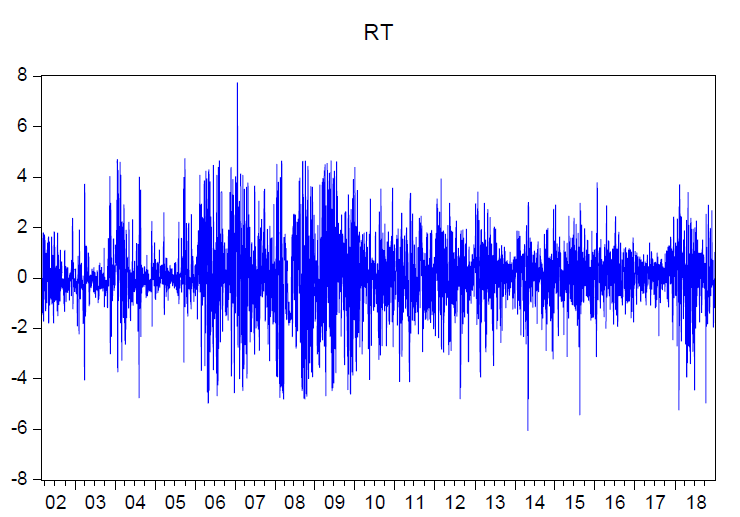

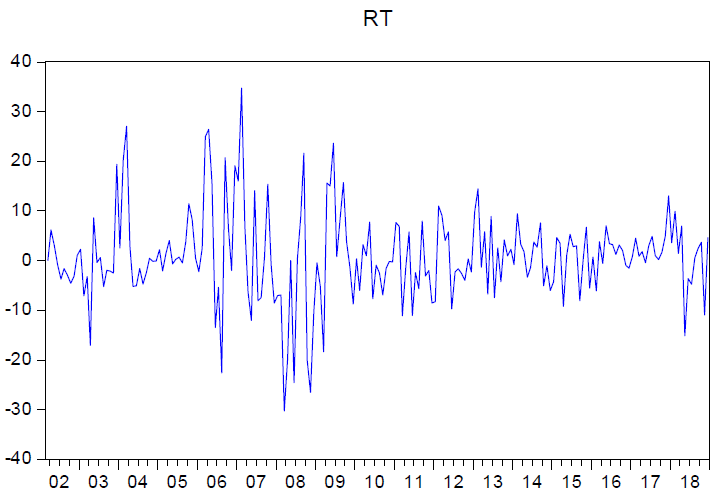

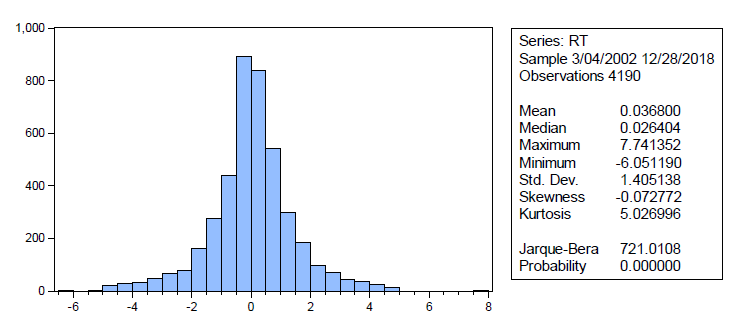

Figures

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (29)

- Bachelier L (1900). Theory of speculation. Gauthier-Villars, Paris, France. https://doi.org/10.24033/asens.476 [Google Scholar]

- Banz RW (1981). The relationship between return and market value of common stocks. Journal of Financial Economics, 9(1): 3-18. https://doi.org/10.1016/0304-405X(81)90018-0 [Google Scholar]

- Beja A (1977). The limits of price information in market processes. Research Program in Finance Working Papers No. 61, University of California at Berkeley, Berkeley, USA. [Google Scholar]

- Bollerslev T, Cai J, and Song FM (2000). Intraday periodicity, long memory volatility, and macroeconomic announcement effects in the US Treasury bond market. Journal of Empirical Finance, 7(1): 37-55. https://doi.org/10.1016/S0927-5398(00)00002-5 [Google Scholar]

- Borges MR (2009). Calendar effects in stock markets: Critique of previous methodologies and recent evidence in European countries. Working Papers nº37-2009/DE/SOCIUS, Instituto Superior de Economia e Gestão, Lisbon, Portugal. [Google Scholar]

- Brown P, Keim DB, Kleidon AW, and Marsh TA (1983). Stock return seasonalities and the tax-loss selling hypothesis: Analysis of the arguments and Australian evidence. Journal of Financial Economics, 12(1): 105-127. https://doi.org/10.1016/0304-405X(83)90030-2 [Google Scholar]

- Choudhry T (2001). Month of the year effect and January effect in pre‐WWI stock returns: Evidence from a non‐linear GARCH model. International Journal of Finance and Economics, 6(1): 1-11. https://doi.org/10.1002/ijfe.142 [Google Scholar]

- Connolly RA (1989). An examination of the robustness of the weekend effect. Journal of Financial and Quantitative Analysis, 24(2): 133-169. https://doi.org/10.2307/2330769 [Google Scholar]

- Ding Z, Granger CW, and Engle RF (1993). A long memory property of stock market returns and a new model. Journal of Empirical Finance, 1(1): 83-106. https://doi.org/10.1016/0927-5398(93)90006-D [Google Scholar]

- Doyle JR and Chen CH (2009). The wandering weekday effect in major stock markets. Journal of Banking and Finance, 33(8): 1388-1399. https://doi.org/10.1016/j.jbankfin.2009.02.002 [Google Scholar]

- Engle RF (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society, 50: 987-1007. https://doi.org/10.2307/1912773 [Google Scholar]

- Fama EF (1965). The behavior of stock-market prices. The Journal of Business, 38(1): 34-105. https://doi.org/10.1086/294743 [Google Scholar]

- Friday HS and Hoang N (2015). Seasonality in the Vietnam stock index. The International Journal of Business and Finance Research, 9(1): 103-112. https://doi.org/10.21102/gefj.2015.03.81.08 [Google Scholar]

- Grossman SJ and Stiglitz JE (1980). On the impossibility of informationally efficient markets. The American Economic Review, 70(3): 393-408. [Google Scholar]

- Gultekin MN and Gultekin NB (1983). Stock market seasonality: International evidence. Journal of Financial Economics, 12(4): 469-481. https://doi.org/10.1016/0304-405X(83)90044-2 [Google Scholar]

- Kruskal WH and Wallis WA (1952). Use of ranks in one-criterion variance analysis. Journal of the American Statistical Association, 47(260): 583-621. https://doi.org/10.1080/01621459.1952.10483441 [Google Scholar]

- Lehmann BN (1990). Fads, martingales, and market efficiency. The Quarterly Journal of Economics, 105(1): 1-28. https://doi.org/10.2307/2937816 [Google Scholar]

- Malkiel BG (1973). A random walk down Wall Street. Norton, New York, USA. [Google Scholar]

- Malkiel BG and Fama EF (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2): 383-417. https://doi.org/10.1111/j.1540-6261.1970.tb00518.x [Google Scholar]

- Mills TC, Siriopoulos C, Markellos RN, and Harizanis D (2000). Seasonality in the Athens stock exchange. Applied Financial Economics, 10(2): 137-142. https://doi.org/10.1080/096031000331761 [Google Scholar]

- Nelson DB (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society, 59: 347-370. https://doi.org/10.2307/2938260 [Google Scholar]

- Nghiem LT, Hau LL, Tri HM, Duy VQ, and Dalina A (2012). Day-of-the-week in different stock markets: New evidence on model-dependency in testing seasonalities in stock return. CAS Discussion Paper No. 85, Centre for ASEAN Studies, Jakarta, Indonesia. [Google Scholar]

- Reinganum MR (1983). The anomalous stock market behavior of small firms in January: Empirical tests for tax-loss selling effects. Journal of Financial Economics, 12(1): 89-104. https://doi.org/10.1016/0304-405X(83)90029-6 [Google Scholar]

- Roberts H (1967). Statistical versus clinical prediction of the stock market. Unpublished Manuscript, IEPR Working Paper 05.41, University of Southern California, Los Angeles, USA. [Google Scholar]

- Rozeff MS and Kinney WR (1976). Capital market seasonality: The case of stock returns. Journal of Financial Economics, 3(4): 379-402. https://doi.org/10.1016/0304-405X(76)90028-3 [Google Scholar]

- Tram TXH, Vo XV, Nguyen PC (2014). Monday effect on the Vietnamese stock exchange pre-crisis, and post-crisis. Journal of Development and Integration, 20(30): 55-60. [Google Scholar]

- Wachtel SB (1942). Certain observations on seasonal movements in stock prices. The Journal of Business of the University of Chicago, 15(2): 184-193. https://doi.org/10.1086/232617 [Google Scholar]

- Yavrumyan E (2015). Efficient market hypothesis and calendar effects: Evidence from the Oslo stock exchange. M.Sc. Thesis, University of Oslo, Oslo, Norway. [Google Scholar]

- Zhang J, Lai Y, and Lin J (2017). The day-of-the-week effects of stock markets in different countries. Finance Research Letters, 20: 47-62. https://doi.org/10.1016/j.frl.2016.09.006 [Google Scholar]