International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN:2313-626X

Frequency: 12

![]()

Volume 6, Issue 8 (August 2019), Pages: 16-22

----------------------------------------------

Original Research Paper

Title: The transparency of accounting information and its role in making investment decision (Companies listed on the Saudi stock exchange)

Author(s): Khaled Adnan Oweis *, Hichem Dekhili

Affiliation(s):

Accounting Department, Business Administration College, Northern Border University, Arar, Saudi Arabia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-5773-1494

Corresponding author's ORCID profile: https://orcid.org/0000-0001-5773-1494

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2019.08.003

Abstract:

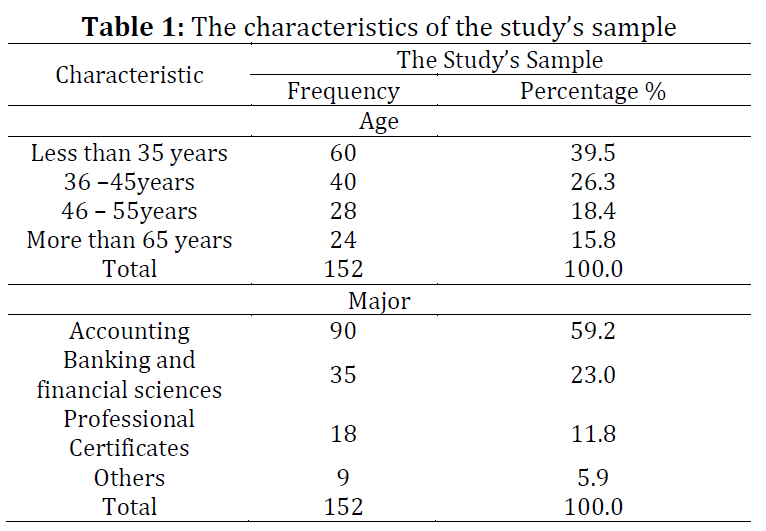

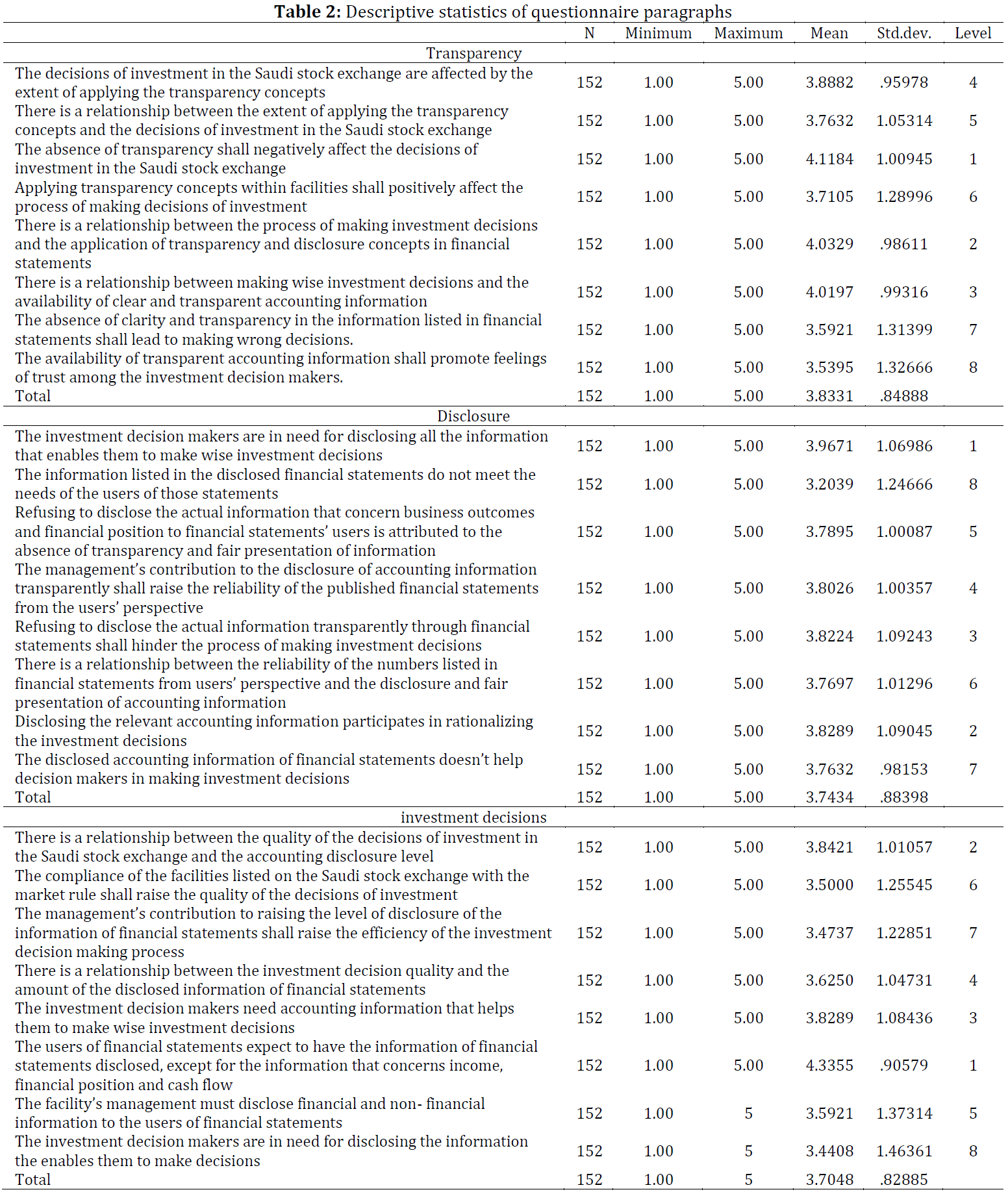

The present study aimed to explore the impact of accounting information transparency on the process of making investment decisions in Saudi companies. It also aimed to explore the role of accounting information transparency in meeting the investors’ needs. It should be noted that the absence of transparency shall negatively affect the growth and development of financial markets. Such absence shall discourage potential investors from investing in the market, whether these investors are inside or outside the country. The present study is considered significant because it sheds a light on a significant issue. The latter issue is represented in the impact of accounting information transparency on the process of making an investment decision in the Saudi Public Shareholding Companies. The researchers of the present study adopted a descriptive analytical approach. In addition, an inductive approach was adopted too. The latter approach was adopted when reviewing the relevant studies and references. The researchers selected a sample. It consists of all the Saudi Public Shareholding Companies that were listed on the Saudi Stock Exchange during 2017. Thus, the sample consists of 172 companies. Questionnaire forms were distributed to several financial managers and managers of internal review department. These managers were selected from the aforementioned companies. 152 questionnaire forms were retrieved. All of the retrieved forms are considered valid for statistical analysis. The response rate is 86.3 % which is a high percentage. It was found that having transparent accounting information shall significantly help managers in making investment decisions. It was also found that transparent accounting information shall reduce the investment-related risks. In light of these results, the researchers suggested several recommendations.

© 2019 The Authors. Published by IASE.

This is an

Keywords: Transparency, Investment, Disclosure, Financial statements

Article History: Received 19 February 2019, Received in revised form 2 June 2019, Accepted 2 June 2019

Acknowledgement:

No Acknowledgement.

Compliance with ethical standards

Conflict of interest: The authors declare that they have no conflict of interest.

Citation:

Arham DI, Rakhmat R, and Arismunandar A et al. (2019). The transparency of accounting information and its role in making investment decision (Companies listed on the Saudi stock exchange). International Journal of Advanced and Applied Sciences, 6(8): 16-22

Figures

No Figure

Tables

Table 1 Table 2 Table 3 Table 4 Table 5 Table 6 Table 7 Table 8 Table 9 Table 10 Table 11

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (13)

- Agbo EI and Udeh SN (2019). Issues in financial markets' development in Sub-Saharan Africa: Lessons from developed economies. In the 5th ICAN Academic conference, Kaduna State University, Kaduna, Nigeria. [Google Scholar]

- Aguinis H and Solarino AM (2019). Transparency and replicability in qualitative research: The case of interviews with elite informants. Strategic Management Journal. https://doi.org/10.1002/smj.3015 [Google Scholar]

- Alam MM, Yasmin S, Rahman M, and Uddin MGS (2011). Effect of policy reforms on market efficiency: Evidence from Dhaka stock exchange (DSE). Economics Research International, 2011: Article ID 864940. https://doi.org/10.1155/2011/864940 [Google Scholar]

- Dhaliwal DS, Radhakrishnan S, Tsang A, and Yang YG (2012). Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. The Accounting Review, 87(3): 723-759. https://doi.org/10.2308/accr-10218 [Google Scholar]

- Fernandez-Feijoo B, Romero S, and Ruiz S (2014). Effect of stakeholders’ pressure on transparency of sustainability reports within the GRI framework. Journal of Business Ethics, 122(1): 53-63. https://doi.org/10.1007/s10551-013-1748-5 [Google Scholar]

- Geiger MA and Rama DV (2006). Audit firm size and going-concern reporting accuracy. Accounting Horizons, 20(1): 1-17. https://doi.org/10.2308/acch.2006.20.1.1 [Google Scholar]

- Hajilee M and Chen CP (2019). The relationship between exchange rate volatility and banking sector development: Time-series evidence from emerging economies. The Journal of Developing Areas, 53(2): 179-191. https://doi.org/10.1353/jda.2019.0029 [Google Scholar]

- Michener G (2019). Gauging the impact of transparency policies. Public Administration Review, 79(1): 136-139. https://doi.org/10.1111/puar.13011 [Google Scholar]

- Saade MR, Gomes V, da Silva MG, Ugaya CM, Lasvaux S, Passer A, and Habert G (2019). Investigating transparency regarding ecoinvent users’ system model choices. The International Journal of Life Cycle Assessment, 24(1): 1-5. https://doi.org/10.1007/s11367-018-1509-x [Google Scholar]

- SOCPA (2017). Saudi organization for certified public accounts. Riyadh, Saudi Arabia. Available online at: https://bit.ly/2WYVTdR

- STATS (2018). General authority for statistics. Available online at: https://www.stats.gov.sa/en

- Tadawul (2018). Capital market authority. Available online at: https://bit.ly/2IWpTgK

- Zhu H, Zhang C, Li H, and Chen S (2015). Information environment, market-wide sentiment and IPO initial returns: Evidence from analyst forecasts before listing. China Journal of Accounting Research, 8(3): 193-211. https://doi.org/10.1016/j.cjar.2015.01.002 [Google Scholar]