International

ADVANCED AND APPLIED SCIENCES

EISSN: 2313-3724, Print ISSN:2313-626X

Frequency: 12

![]()

Volume 6, Issue 3 (March 2019), Pages: 86-95

----------------------------------------------

Original Research Paper

Title: Mapping of mandatory and voluntary disclosures with capital market variables and future research opportunities: Market based accounting research study period 2006-2015

Author(s): Kautsar Riza Salman *

Affiliation(s):

Accounting Department, STIE Perbanas Surabaya, Surabaya, Indonesia

* Corresponding Author.

Corresponding author's ORCID profile: https://orcid.org/0000-0001-9463-6429

Corresponding author's ORCID profile: https://orcid.org/0000-0001-9463-6429

Digital Object Identifier:

https://doi.org/10.21833/ijaas.2019.03.013

Abstract:

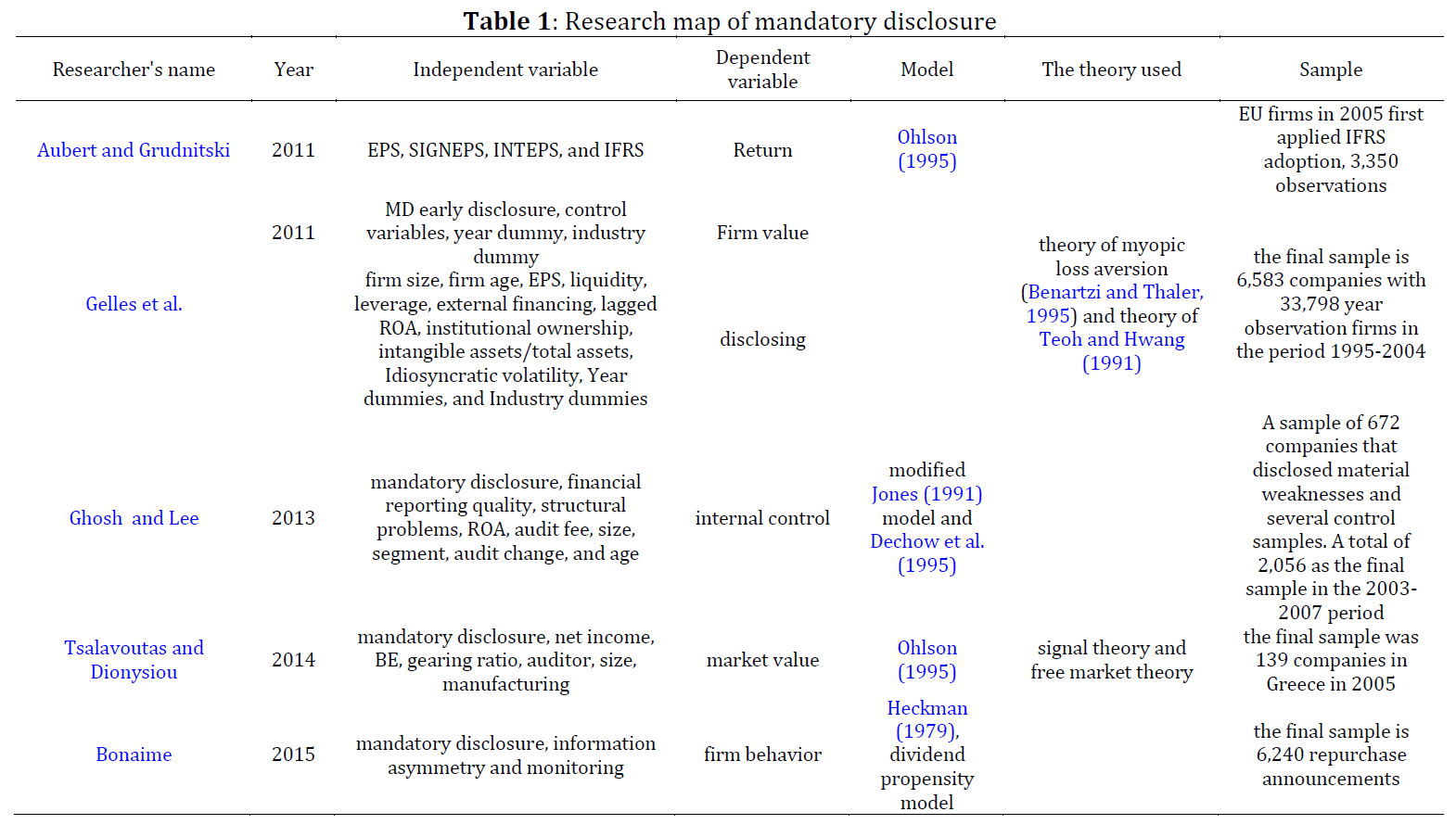

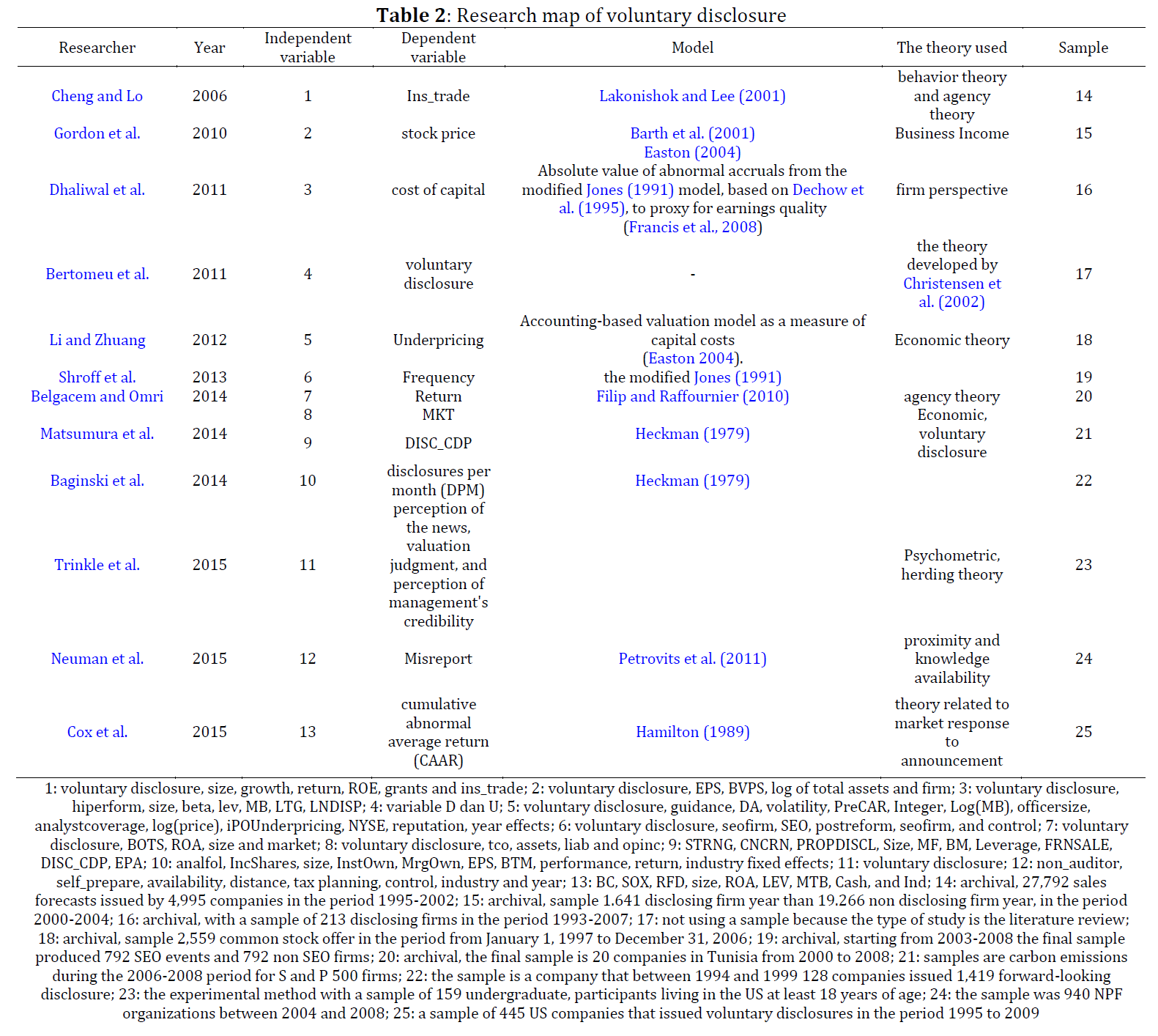

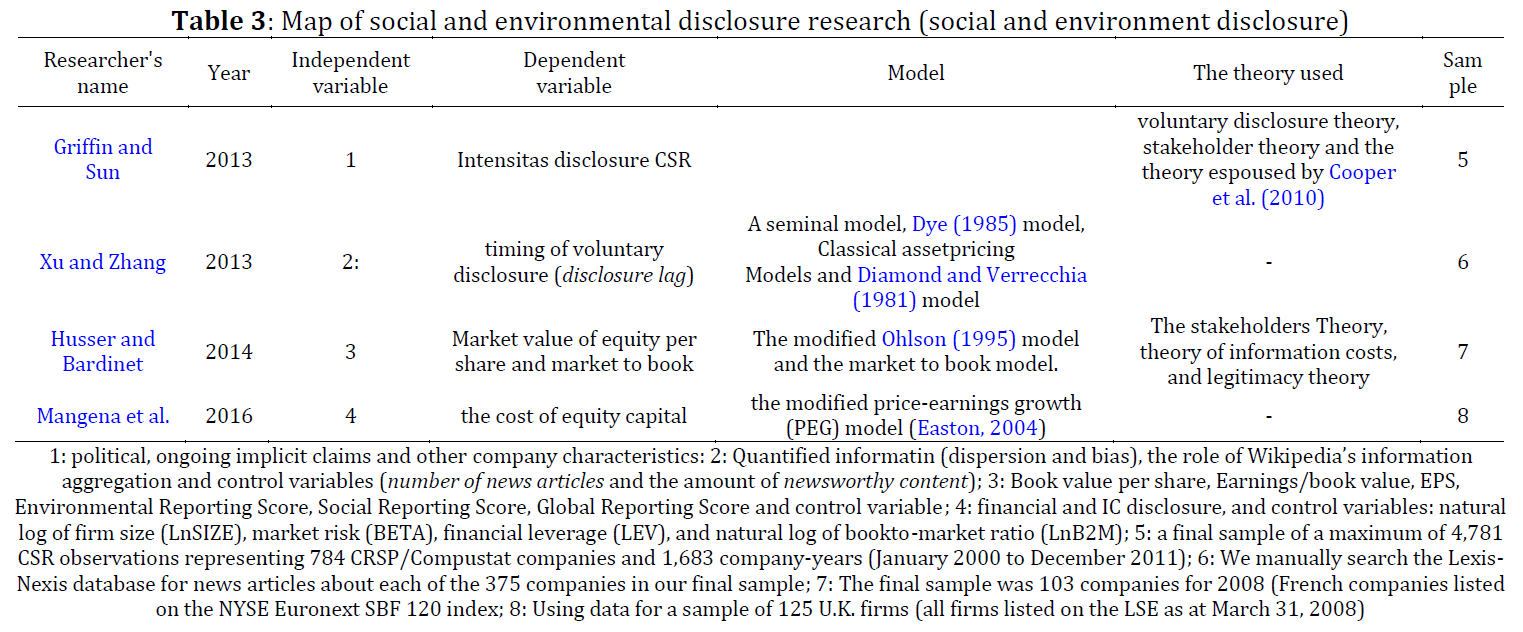

The aim of this paper is to review a number of previous studies that examined the relationship of mandatory and voluntary disclosure variables with capital market variables such as market prices, market returns and the cost of equity capital. The first part of this paper is an explanation of the theories that form the basis of research on this topic. The second part of this paper is a review of some accounting research that examines the relationship between company disclosure and capital market variables. The third part reveals several accounting research opportunities that can be done to continue the results of previous studies. The review process was conducted on twelve international journals related to capital market-based accounting research in the period 2006-2015. Based on the literature review, the results show that the basic theories that are widely used are the efficient market theory, agency theory, behavior theory, economic theory, voluntary disclosure theory, value relevance, and net surplus theory. The most widely conducted research is to examine the effect of mandatory disclosures on capital market variables such as returns, market value, firm value, and others. In addition, the majority of studies examine the impact of voluntary disclosure on capital market variables such as stock prices, equity capital costs, and returns. The archiving method is more widely used by utilizing secondary data, whereas few use experiments. Research opportunities that can be directed to: (1) examine the impact of sharia disclosures on capital market variables (2) using experimental methods, and (3) test the association of social disclosures, environmental disclosures, disclosure of intellectual capital and other types of voluntary disclosures.

© 2019 The Authors. Published by IASE.

This is an

Keywords: Literature review, Mandatory disclosure, Voluntary disclosure, Market price, Market return, Cost of equity capital

Article History: Received 19 October 2018, Received in revised form 25 January 2019, Accepted 27 January 2019

Acknowledgement:

No Acknowledgement

Compliance with ethical standards

Conflict of interest: The authors declare that they have no conflict of interest.

Citation:

Salman KR (2019). Mapping of mandatory and voluntary disclosures with capital market variables and future research opportunities: Market based accounting research study period 2006-2015. International Journal of Advanced and Applied Sciences, 6(3): 86-95

Figures

No Figure

Tables

{kind=link}

{kind=link}

{kind=link}

----------------------------------------------

References (59)

- Aubert F and Grudnitski G (2011). The impact and importance of mandatory adoption of international financial reporting standards in Europe. Journal of International Financial Management and Accounting, 22(1): 1-26. https://doi.org/10.1111/j.1467-646X.2010.01043.x [Google Scholar]

- Baginski SP, Clinton SB, and Mcguire ST (2014). Forward‐looking voluntary disclosure in proxy contests. Contemporary Accounting Research, 31(4): 1008-1046. https://doi.org/10.1111/1911-3846.12057 [Google Scholar]

- Ball R and Brown P (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6(2): 159-178. https://doi.org/10.2307/2490232 [Google Scholar]

- Barth ME, Beaver WH, and Landsman WR (2001). The relevance of the value relevance literature for financial accounting standard setting: Another view. Journal of Accounting and Economics, 31(1-3): 77-104. https://doi.org/10.1016/S0165-4101(01)00019-2 [Google Scholar]

- Beaver WH (1968). The information content of annual earnings announcements. Journal of Accounting Research, 6: 67-92. https://doi.org/10.2307/2490070 [Google Scholar]

- Beaver WH (1996). Directions in accounting research: NEAR and FAR. Accounting Horizons, 10(2): 113-124. [Google Scholar]

- Belgacem I and Omri A (2014). The value relevance of voluntary disclosure: Evidence from Tunisia stock market. International Journal of Management, Accounting and Economics, 1(5): 353-370. [Google Scholar]

- Benartzi S and Thaler RH (1995). Myopic loss aversion and the equity premium puzzle. The Quarterly Journal of Economics, 110(1): 73-92. https://doi.org/10.2307/2118511 [Google Scholar]

- Bertomeu J, Beyer A, and Dye RA (2011). Capital structure, cost of capital, and voluntary disclosures. The Accounting Review, 86(3): 857-886. https://doi.org/10.2308/accr.00000037 [Google Scholar]

- Bonaime AA (2015). Mandatory disclosure and firm behavior: Evidence from share repurchases. The Accounting Review, 90(4): 1333-1362. https://doi.org/10.2308/accr-51027 [Google Scholar]

- Botosan CA (1997). Disclosure level and the cost of equity capital. The Accounting Review, 72(3): 323-349. [Google Scholar]

- Bushee BJ and Leuz C (2005). Economic consequences of SEC disclosure regulation: Evidence from the OTC bulletin board. Journal of Accounting and Economics, 39(2): 233-264. https://doi.org/10.1016/j.jacceco.2004.04.002 [Google Scholar]

- Cheng Q and Lo K (2006). Insider trading and voluntary disclosures. Journal of Accounting Research, 44(5): 815-848. https://doi.org/10.1111/j.1475-679X.2006.00222.x [Google Scholar]

- Christensen PO, Feltham GA, and Wu MGH (2002). Cost of capital in residual income for performance evaluation. The Accounting Review, 77(1): 1-23. https://doi.org/10.2308/accr.2002.77.1.1 [Google Scholar]

- Cooper MJ, Gulen H, and Ovtchinnikov AV (2010). Corporate political contributions and stock returns. Journal of Finance, 65(2): 687-724. https://doi.org/10.1111/j.1540-6261.2009.01548.x [Google Scholar]

- Cox RAK, Dayanandan A, and Donker H (2015). Relationship between voluntary disclosure and the economic cycle: Empirical research findings. Journal of Financial Management and Analysis, 28(1): 44-60. [Google Scholar]

- Dechow PM, Sloan RG, and Sweeney AP (1995). Detecting earnings management. The Accounting Review, 70(2): 193-225. [Google Scholar]

- Dhaliwal DS, Li OZ, Tsang A, and Yang YG (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review, 86(1): 59-100. https://doi.org/10.2308/accr.00000005 [Google Scholar]

- Diamond DW and Verrecchia RE (1981). Information aggregation in a noisy rational expectations economy. Journal of Financial Economics, 9(3): 221-235. https://doi.org/10.1016/0304-405X(81)90026-X [Google Scholar]

- Dye RA (1985). Disclosure of nonproprietary information. Journal of Accounting Research, 23(1): 123-145. https://doi.org/10.2307/2490910 [Google Scholar]

- Dye RA (1986). Proprietary and nonproprietary disclosures. Journal of Business, 59(2): 331-366. https://doi.org/10.1086/296331 [Google Scholar]

- Easton PD (1999). Security returns and the value relevance of accounting data. Accounting Horizons, 13(4): 399-412. https://doi.org/10.2308/acch.1999.13.4.399 [Google Scholar]

- Easton PD (2004). PE ratios, PEG ratios, and estimating the implied expected rate of return on equity capital. The Accounting Review, 79(1): 73-95. https://doi.org/10.2308/accr.2004.79.1.73 [Google Scholar]

- Feltham GA and Ohlson JA (1995). Valuation and clean surplus accounting for operating and financial activities. Contemporary Accounting Research, 11(2): 689-731. https://doi.org/10.1111/j.1911-3846.1995.tb00462.x [Google Scholar]

- Filip A and Raffournier B (2010). The value relevance of earnings in a transition economy: The case of Romania. The International Journal of Accounting, 45(1): 77-103. https://doi.org/10.1016/j.intacc.2010.01.004 [Google Scholar]

- Francis J and Schipper K (1999). Have financial statements lost their relevance?. Journal of Accounting Research, 37(2): 319-352. https://doi.org/10.2307/2491412 [Google Scholar]

- Francis J, Nanda D, and Olsson P (2008). Voluntary disclosure, earnings quality, and cost of capital. Journal of Accounting Research, 46(1): 53-99. https://doi.org/10.1111/j.1475-679X.2008.00267.x [Google Scholar]

- Gelles G, Howe JS, and Xing X (2011). Does it pay to disclose managerial earnings information early?. Journal of Financial Research, 34(2): 365-386. https://doi.org/10.1111/j.1475-6803.2011.01294.x [Google Scholar]

- Ghosh A and Lee YG (2013). Financial reporting quality, structural problems and the informativeness of mandated disclosures on internal controls. Journal of Business Finance and Accounting, 40(3-4): 318-349. https://doi.org/10.1111/jbfa.12015 [Google Scholar]

- Gordon LA, Loeb MP, and Sohail T (2010). Market value of voluntary disclosures concerning information security. MIS Quarterly, 34(30): 567-594. https://doi.org/10.2307/25750692 [Google Scholar]

- Griffin PA and Sun Y (2013). Strange bedfellows? Voluntary corporate social responsibility disclosure and politics. Accounting and Finance, 53(4): 867-903. https://doi.org/10.1111/acfi.12033 [Google Scholar]

- Hamilton JD (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57(2): 357-384. https://doi.org/10.2307/1912559 [Google Scholar]

- Hassan OA, Romilly P, Giorgioni G, and Power D (2009). The value relevance of disclosure: Evidence from the emerging capital market of Egypt. The International Journal of Accounting, 44(1): 79-102. https://doi.org/10.1016/j.intacc.2008.12.005 [Google Scholar]

- Healy PM and Palepu KG (1993). The effect of firms' financial disclosure strategies on stock prices. Accounting Horizons, 7(1): 1-11. [Google Scholar]

- Heckman J (1979). Sample selection bias as a specification error. Econometricia, 47(1): 153-161. https://doi.org/10.2307/1912352 [Google Scholar]

- Hussainey K and Mouselli S (2010). Disclosure quality and stock returns in the UK. Journal of Applied Accounting Research, 11(2): 154-174. https://doi.org/10.1108/09675421011069513 [Google Scholar]

- Hussainey K and Walker M (2009). The effects of voluntary disclosure and dividend propensity on prices leading earnings. Accounting and Business Research, 39(1): 37-55. https://doi.org/10.1080/00014788.2009.9663348 [Google Scholar]

- Husser J and Bardinet EF (2014). The effect of social and environmental disclosure on companies’ market value. Management International, 19(1): 61-84. https://doi.org/10.7202/1028490ar [Google Scholar]

- Jones JJ (1991). Earnings management during import relief investigations. Journal of Accounting Research, 29(2): 193-228. https://doi.org/10.2307/2491047 [Google Scholar]

- Kang T and Pang HY (2005). Economic development and the value-relevance of accounting information a disclosure transparency perspective. Review of Accounting and Finance, 4(1): 5-31. https://doi.org/10.1108/eb043416 [Google Scholar]

- Lakonishok J and Lee I (2001). Are insider trader informative?. Review of Financial Studies, 14(1): 79-111. https://doi.org/10.1093/rfs/14.1.79 [Google Scholar]

- Leuz C and Wysocki PD (2008). Economic consequences of financial reporting and disclosure regulation: A review and suggestions for future research. Working Paper, University of Chicago and Massachusetts Institute of Technology, USA. https://doi.org/10.2139/ssrn.1105398 [Google Scholar]

- Lev B and Zarowin P (1999). The boundaries of financial reporting and how to extend them. Journal of Accounting Research, 37(2): 353-385. https://doi.org/10.2307/2491413 [Google Scholar]

- Li OZ and Zhuang Z (2012). Management guidance and the underpricing of seasoned equity offerings. Contemporary Accounting Research, 29(3): 710-737. https://doi.org/10.1111/j.1911-3846.2011.01120.x [Google Scholar]

- Mangena M, Li J, and Tauringana V (2016). Disentangling the effects of corporate disclosure on the cost of equity capital: A study of the role of intellectual capital disclosure. Journal of Accounting, Auditing and Finance, 31(1): 3-27. https://doi.org/10.1177/0148558X14541443 [Google Scholar]

- Matsumura EM, Prakash R, and Vera-Muñoz SC (2014). Firm-value effects of carbon emissions and carbon disclosures. The Accounting Review, 89(2): 695-724. https://doi.org/10.2308/accr-50629 [Google Scholar]

- Neuman SS, Omer TC, and Thompson AM (2015). Determinants and consequences of tax service provider choice in the not‐for‐profit sector. Contemporary Accounting Research, 32(2): 703-735. https://doi.org/10.1111/1911-3846.12080 [Google Scholar]

- Ohlson JA (1995). Earnings, book values, and dividends in equity valuation. Contemporary Accounting Research, 11(2): 661-687. https://doi.org/10.1111/j.1911-3846.1995.tb00461.x [Google Scholar]

- Petrovits C, Shakespeare C, and Shih A (2011). The Causes and consequences of internal control problems in nonprofit organizations. The Accounting Review, 86(1): 325-357. https://doi.org/10.2308/accr.00000012 [Google Scholar]

- Richardson AJ and Welker M (2001). Social disclosure, financial disclosure and the cost of equity capital. Accounting, Organizations and Society, 26(7-8): 597-616. https://doi.org/10.1016/S0361-3682(01)00025-3 [Google Scholar]

- Scott WR (2012). Financial accounting theory. 6th Edition, Pearson Prentice Hall, Toronto, Canada. [Google Scholar]

- Shroff N, Sun AX, White HD, and Zhang W (2013). Voluntary disclosure and information asymmetry: Evidence from the 2005 securities offering reform. Journal of Accounting Research, 51(5): 1299-1345. https://doi.org/10.1111/1475-679X.12022 [Google Scholar]

- Slack R and Shrives P (2010). Voluntary disclosure narratives: More research or time to reflect?. Journal of Applied Accounting Research, 11(2): 84-89. https://doi.org/10.1108/09675421011069478 [Google Scholar]

- Teoh SH and Hwang CY (1991). Nondisclosure and adverse disclosure as signals of firm value. The Review of Financial Studies, 4(2): 283-313. https://doi.org/10.1093/rfs/4.2.283 [Google Scholar]

- Trinkle BS, Crossler RE, and Bélanger F (2015). Voluntary disclosures via social media and the role of comments. Journal of Information Systems, 29(3): 101-121. https://doi.org/10.2308/isys-51133 [Google Scholar]

- Trueman B (1986). Why do managers voluntarily release earnings forecasts?. Journal of Accounting and Economics, 8(1): 53-71. https://doi.org/10.1016/0165-4101(86)90010-8 [Google Scholar]

- Tsalavoutas I and Dionysiou D (2014). Value relevance of IFRS mandatory disclosure requirements. Journal of Applied Accounting Research, 15(1): 22-42. https://doi.org/10.1108/JAAR-03-2013-0021 [Google Scholar]

- Verrecchia RE (1983). Discretionary disclosure. Journal of Accounting and Economics, 5: 179-194. https://doi.org/10.1016/0165-4101(83)90011-3 [Google Scholar]

- Xu SX and Zhang X (2013). Impact of Wikipedia on market information environment: Evidence on management disclosure and investor reaction. MIS Quarterly, 37(4): 1043-1068. https://doi.org/10.25300/MISQ/2013/37.4.03 [Google Scholar]